“For every action, there is an equal and opposite reaction.” — Newton’s third law of motion

When central banks enacted their asset purchase (QE) programs and started to create the most preposterous asset market bubble in history, it was obvious that there would be a point when they would need to start selling assets from their balance sheet. This operation is called quantitative tightening, or QT.

How did the previous balance sheet runoff go?

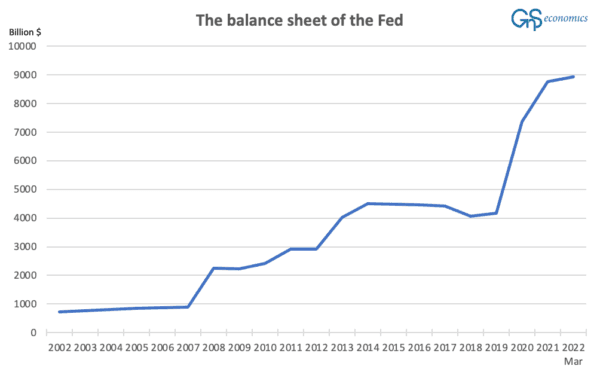

The Fed started to shrink its balance sheet in October 2017. First, the speed was very modest with an asset roll-off of $10 billion per month. In January 2018, the speed accelerated to $30 billion per month and further to $50 billion per month in October. The response of the markets was brutal. Selling in the U.S. stock markets commenced in October, and, while there were few brief rallies in November and the Dow Jones Industrial Average (DJIA) rose a little bit by the end of the month, an uneasy mood crept into the capital markets.

In December, selling accelerated to a rout, and it also reached the credit markets. On Christmas Eve, the DJIA recorded its biggest Christmas fall ever. Right after the turn of the year, credit markets were cascading into a panic.

That led to the famous ‘pivot’ of the Fed in early January 2019. Just a few weeks earlier, the FOMC had signaled two to three rate increases and the balance sheet runoff being on an ‘autopilot.’ On Jan. 4, Chairman Jerome Powell stated in a CNBC interview that “there’s no preset path” for rate boosts and adjusting the balance sheet of the Fed. In addition, several regional Fed presidents gave speeches presenting a dovish stance against balance sheet normalization (runoff) and rate rises. The People’s Bank of China also injected record amounts of liquidity into its banking system.

While these combined efforts stopped the market rout, the problems were not over. Not by a long shot.

While the Fed discarded efforts for further rate rises, they continued to shrink the balance sheet till September. On Sept. 16, 2019, rates in the repurchase agreements, or “repo” markets skyrocketed. The $4 trillion repo market is used by big institutional investors to satisfy their short-term, often “overnight,” demand for liquidity or money. If rates in the repo markets stay elevated for any longer period of time, highly leveraged institutions start to fail, and trust in financial markets and the banking sector will become compromised.

Thus, the Fed was forced to step in to provide liquidity to the markets.

These factors, combined with the decreased money-market activity of banks were likely what made the big four banks wary of lending to the repo market if there was even a hint of a potential loss. This “hint” occurred on Sept. 17, 2019, and the repo market imploded.

The Fed responded by enacting its repo facility, for the first time since 2009. On Oct. 16, the Fed also started to buy U.S. Treasury bills at the rate of $60 billion per month. The program was dubbed “Not-QE.” The Fed didn’t consider it a QE program, because in it the Fed bought only Treasury notes with a maturity of less than a year, while bonds the Fed bought in QE programs had maturities of more than a year. This, of course, was just ‘muddying the waters,’ as the Fed was, again, buying debt issued by the federal government.

But, what actually happens in QT?

In it, the central bank rolls off (sells or doesn’t reacquire assets after they mature) investment grade assets from its balance sheet, which results in an over-supply of these same assets. This pushes their price down (yields up) followed by even bigger increases in prices of non-investment grade assets, because their risk/profit ratio worsens with the increasing yields of investment grade assets. This starts a flight to quality (to less risky bonds), which disperses the yields and spreads of the investment and non-investment grade assets further.

Considering that the balance sheet of the Fed is around twice as big as it was in late 2017, it’s nearly impossible to imagine a scenario where QT wouldn’t lead to overwhelming downward pressure in the financial markets. QT and rising interest rates will be like a “double-whammy” to equity and credit markets.

If the Fed goes through with its plan—keeping in mind that it may not have any other option—we can expect serious market turbulence in the coming months, and an eventual crash of equity and credit markets.

The main problem with QT is that there will be very few places to hide. Years of QE have pushed the artificial central bank liquidity to practically every corner of the financial markets, and when it’s withdrawn, the whole financial asset universe will eventually hear the “sucking sound.”