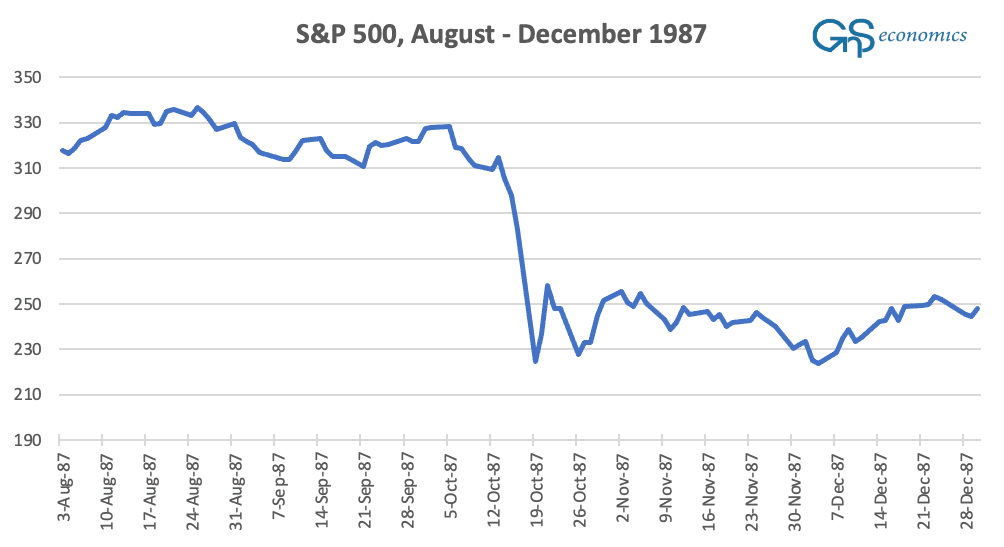

On Oct. 19, 1987, the U.S. stock markets collapsed. They had enjoyed a stellar run supported by the bull market, which started in August 1982. The ‘Roaring Eighties,’ that is, the economic boom of the 1980s, drove equity markets to new records. But in October, indications of a slowing economy, rising interest rates, and stock liquidations of mutual funds broke the trust of the investors. On the day that came to be known as “Black Monday,” the Dow Jones Industrial Average fell by (around) 20 percent, its largest daily fall ever.

The Greenspan put was a policy doctrine, where the Fed allowed the markets to rise rather uncontrollably and then cleaned up after they collapsed. It was aggressively used during and after the ‘Dotcom bubble’ in early 2000s. However, the market bailouts of central banks were pushed to overdrive during the Global Financial Crisis.

In August 2012, the European Central Bank enacted the Outright Monetary Transactions program to halt the rise in sovereign bond yields in the Eurozone. In 2015, in an effort to devalue the Swiss Franc, the Swiss National Bank started to “invest” in foreign assets, including U.S. equities. In many cases, such purchases by the SNB coincided with increased market turbulence/risk, as during the first actual post-Global Financial Crisis rate hike cycle of the Fed in 2016/2017.

On Jan. 4, 2019, due to a threat of an outright collapse of the stock and credit markets, Fed Chairman Jerome Powell ‘pivoted’ from his previous statements of several interest rate rises and automated balance sheet run-off in 2019. Between January and March 2019, the Federal Reserve made a complete U-turn from its earlier stance of several interest rate rises in 2019 to possible cuts and ending the balance sheet normalization program prematurely.

On the 16th, the New York Fed announced that it will add $500 billion in the over-night loans to repo-market. On the 17th, the Fed announced that it would use $1 trillion to mob up corporate paper from issuers. On the 18th, the European Central Bank announced that it would buy 750 billion euros worth of bonds and securities. On the 19th, the Fed announced that it would create lending facility to money market mutual funds. On March 25, 2020, interest rates of short-term corporate debt surged to 2.43 percent above the federal-funds rate, the over-night lending rate of the Fed, which led the central bank to issue a program targeted at the corporate markets.

At the end of May 2020, the Fed backstopped “repo” and U.S. Treasury markets, intervened in corporate commercial-paper and municipal bond markets and short-term money-markets, and bought corporate bond ETFs, including some speculative-grade, or “junk,” corporate debt. It also launched its “Main Street Lending” program, where it provided loans to middle-market businesses. Alas, come June 2020, the Fed had become the financial markets of the United States. The bailout operations enacted by Greenspan had reached the point where the fears that the creation of the Fed would ‘socialize’ the economy had materialized.

The market economy operates through a risk-reward relationship. Gains, booms, losses, and crashes are an essential part of the proper functioning of it. Market bailouts by the central banks have deformed the capital markets and thus the allocation of capital. Market losses have been socialized, while gains have remained, more or less, private. They have made the financial markets more leveraged, more speculative, and thus more fragile.

Now, the question is, can the central banks continue their market bailouts when inflation runs ‘amok’? I am skeptical, but it’s impossible to say for sure.

Many investors and economist are hoping that central banks will be able to continue their ultra-low interest rate and bailout policies, because they fear the collapse that would ensue, if (when) the support of central banks is drawn from the markets. But there really is no other way the massive meddling of the central banks in the markets can end than a crash of epic proportions or a full socialization of the financial markets and the economy.

I don’t think this is a choice any of us needs to ponder for long.