Sixty years ago, economist Beryl Sprinkel wrote a book titled, “Money and Stock Prices.” Sprinkel was my boss and mentor at Harris Bank in Chicago, and later he became chairman of then-president Ronald Reagan’s Council of Economic Advisers.

His book explained how stock prices respond fairly predictably to changes in the money supply. Sprinkel’s historical data show stock prices consistently react to changes in the money supply in the same direction.

As the Federal Reserve increases the money supply, the extra money lifts stock prices before filtering through to the economy to increase overall spending. The opposite occurs when the Fed slows the growth or reduces the money supply. The shortfall in money drives stock prices down before filtering through the economy and slowing the pace of spending.

Since the early 1960s, I have closely followed the relationship between money and stock prices. One key change involves the measurement of the money supply. Changes in the way the Fed conducts money policy at times makes it necessary to avoid the more conventional measures of money.

In 2008, those who focused on our monetary analysis were able to avoided the collapse in stock prices associated with the financial crisis. Once the money supply began to increase in early 2009, our analysis provided a signal to buy stocks.

While the relationship between money, properly measured, and stock prices generally has been reliable, it has not been perfect. All types of factors, including rational expectations, can affect the relationship between money, stocks, and the economy. One example is the recent disconnect between money and stock prices.

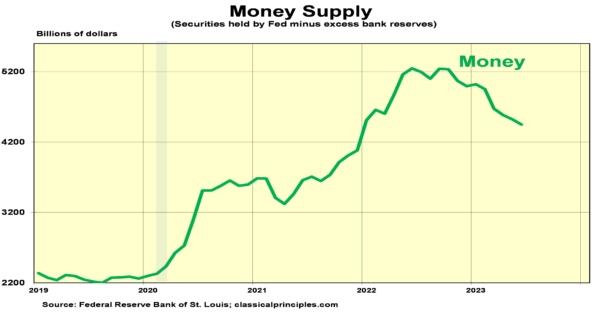

The chart below shows my current preferred measure of money. This measure consists of changes in the Federal Reserve’s holdings of securities as well as changes in bank deposits with the Federal Reserve.

From mid-2021 to mid-2022, there was a surge in money as the economy recovered from the government shutdown. By mid-2022, soaring inflation led the Fed to begin curtailing money growth. By June 2023, the money supply was down 15 percent from a year ago. Despite this decline, the money supply in June 2023 was still up 20 percent from where it was two years ago. The erratic up and down in money has created mixed economic signals, making it difficult for businesses and investors to respond to this dramatic shift in policy.

Fixed-Income Markets: A Normal Response

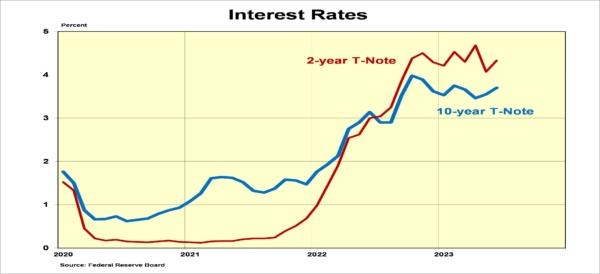

Financial markets have responded in different ways to the shift in monetary policy. Fixed-income markets have responded to the sharp increase in interest rates in a manner consistent with history. The increase in the federal funds rate from essentially zero percent to just over 5 percent was accompanied by other sharp interest-rate increases. As the next chart shows, interest rates at the shorter end increased faster than longer-term interest rates. This is typical of a period of significant monetary restraint. When shorter-term interest rates move above longer-term rates, there is an inverted yield curve, which is often associated with a highly restrictive monetary policy.Traditional measures of the money supply also show significant rates of decline, providing further confirmation monetary policy has turned restrictive.

The Disconnect

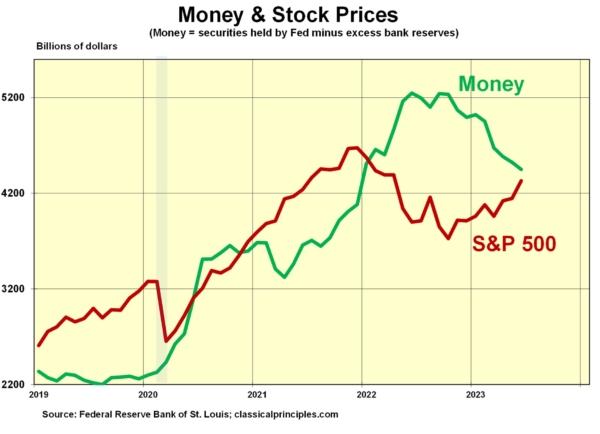

While the behavior in fixed-income markets has been normal, the behavior in stocks has been abnormal. Stock prices began to decline at the beginning of 2022, seemingly in anticipation of monetary restraint which began six to nine months later. By autumn of 2022, when the Fed’s monetary restraint was beginning, stock prices hit their lows, with the benchmark S&P 500 Index down 25 percent from its peak. Since October 2022, as monetary policy became progressively more restrictive, stocks rebounded sharply. The S&P 500 is currently up 20 percent from its October 2022 low, but down about 9 percent from its all-time high at the beginning of 2022.The rebound in stocks since October is a disconnect from the market’s normal response to monetary policy. As with the previous decline prior to October, it appears stock market investors are anticipating a rapid decline in inflation and an end to the Fed’s monetary restraint.

This unusual development suggests some cautionary warnings with respect to stocks. Investors should consider that first-quarter 2023 S&P 500 earnings were 20 percent above their longer-term trend. Assuming further strong gains during a period of monetary restraint would be another anomaly. Investors also assume inflation will decline fairly rapidly and that interest rates are close to their peaks. Finally, stock investors seem to assume the Fed’s continued sales of securities will not be a problem for the economy.

It would be wonderful if these assumptions were correct and stock prices continue to move higher. However, with a restrictive monetary policy entering its second year, it is too soon to dismiss the impact of an ongoing policy of monetary restraint. Lags between monetary restraint and the economy suggest the main impact of such restraint will come in the last half of this year. While there are still signs showing an economy growing at a rate of 2 percent, there are also indications the economy is much weaker than it appears.

Tax receipts to the Treasury are highly erratic, but can still provide an indication of the health of profits and wages. With three quarters of the current fiscal year behind us, receipts are down 11 percent from the year-ago period. Even more concerning, tax receipts for April and May are down 24 percent from a year ago.

Stocks currently have incorporated a number of very positive assumptions about inflation and the economy. So long as the Fed continues to take money out of the economy, the history of money and stock prices suggests a defensive position toward stocks is more appropriate.