The United States is in recession. While two consecutive negative GDP prints is a raw (technical) measure of a recession, there’s no escaping from it anymore.

How does one prepare for such an event?

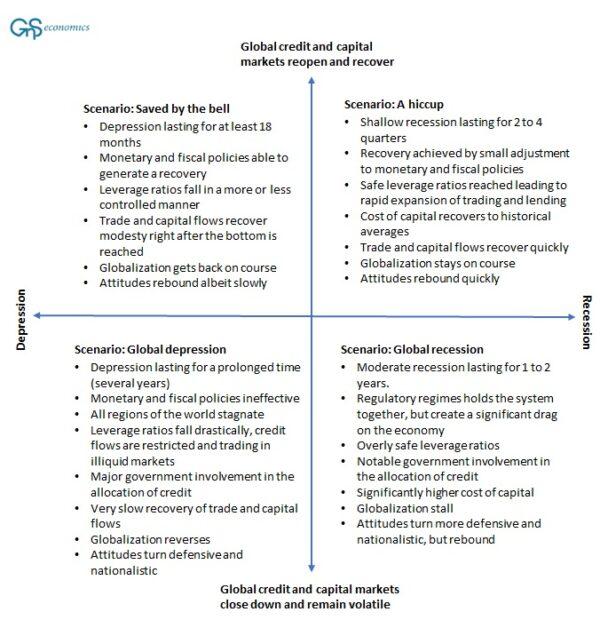

However, let’s start with a generalized take on how recessions and economic depression affect the economy, trade, banking, and income. In simplified terms, economic downturns can be presented using a four-sector model according to the depth of the downturn and its effect of the credit and capital markets.

Scenario 1

Let’s first go through the recession dynamics. In the upper-right corner, we would be facing a shallow, possibly a localized recession, concentrating on a certain area and/or some countries, from which recovery would be quick. Credit and capital markets would stay functional throughout the “ordeal.” Governments and central banks would have plenty of tools to combat the recession (e.g., interest rates would be high and government debt low). In addition, the indebtedness of households, corporations, and investors would be moderate entering the recession, and leverage among them would reach safe (low) levels quickly. Global trade would be unaffected. An example of this would be the recession that followed the bursting of the tech bubble during the late 1990s. We clearly are not there now.Scenario 2

In the lower-right quadrant, we would be facing a global recession. Downturn would affect all sectors of the economy, and capital and credit markets would become dysfunctional or they would even run a risk of a closure. The availability of credit to households and governments would diminish, and the price (interest) of credit would rise considerably. Government involvement would be needed to keep credit flowing. Leverage among households, corporations, and investors would fall heavily. Global trade disruptions would emerge. Authorities, however, would be able to contain the fallout, and recovery would start relatively quickly. An example of this would be the global recession of 2008–09.Many are hoping that we would be entering the lower-right quadrant, but that is unlikely. Leverage ratios, especially among corporations and investors, are very high—in some cases even extreme—and central banks and governments have very little room to maneuver, at least using traditional methods, such as interest-rate cuts and issuance of more sovereign debt. Several governments, like those of the United States, Japan, and Italy, are highly indebted. This means their ability to stomach higher interest rates is gravely limited.

Scenario 3

In the upper-left quadrant, the hit on the economy would be heavy, but authorities would be able to stop it from escalating into full-blown global depression though monetary and fiscal policies. As explained above, this is unlikely now, as authorities really do not have much traditional capacity left. It is, of course, possible that governments and central banks will do “whatever it takes” to stop the recession from escalating into a global depression, but that would require some extreme measures, such as central banks taking an extremely large role in the capital markets, the issuance of central bank digital currencies, and government taking over large parts of the economy. It would “socialize” our economies and turn them to something very different than what they are now.Scenario 4

This plot line would affect households and corporations in drastic ways. The availability of credit would collapse or disappear altogether. Credit lines of households and corporations would be withdrawn, wherever possible, and the global flow of credit would simply seize up. Market liquidity would collapse, and equity and bond markets would crash. Unemployment would skyrocket, globalization would reverse as countries would pivot toward protecting their own assets and citizens. Attitudes would turn nationalistic and defensive. Recovery would be painful and slow.‘Prepare, Secure, and Capitalize’

Our survival strategies for firms, households, and investors follow a simple logic: prepare, secure, and capitalize. At its heart is the concept of “counter-cyclicality,” derived from Keynesian economic theory. In it, corporations, households, and investors mitigate the effects of business cycles and aim to exploit them instead of slavishly following them. Naturally, this is easier said than done—but it can be done!“If the Fed pushes ahead with strong rate rises and hastened balance sheet run-off, artificial liquidity will be drawn from the markets and financial conditions will turn noticeably tighter during the summer. Thus, we urge everyone to enjoy the summer, because fall is likely to bring ‘heavy skies’ over the global economy and the financial markets.”

Come fall, the “perfect storm” is likely to be upon us.