I have been detailing the problems in the world economy in several of my previous posts. Now, it’s time to explain where it all began and why the situation in the global economy is so precarious. It all starts with China.

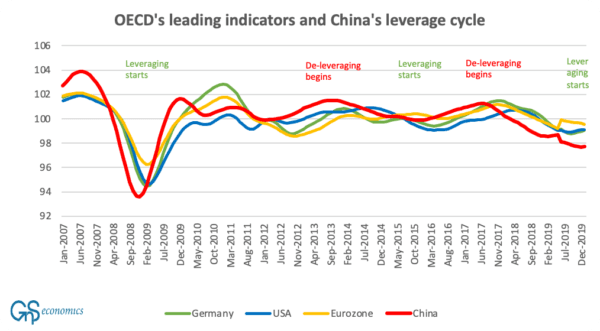

I realized that China—not, for example, the United States—had driven the global economy since the global financial crisis of 2008 and 2009. This was visible from the leading indicators. I (we) estimated that, after 2008, wherever China’s economy was heading, whether in an upturn or downturn, the economies of both the eurozone and the United States would follow, respectively, with a lag of around two to three months and a lag of around three to four months.

What happened in 2015 and 2016, then?

In 2015, Chinese leaders tried to stabilize the Chinese economy by tightening the availability of credit (deleveraging), especially to the manufacturing sector. This led to a slump in the Chinese housing market, which had already weakened in 2014. Because real estate had been the backbone of the Chinese economy for the past two decades, the overall economy soured quickly. The Chinese stock market started to fall, and the global economy followed suit.

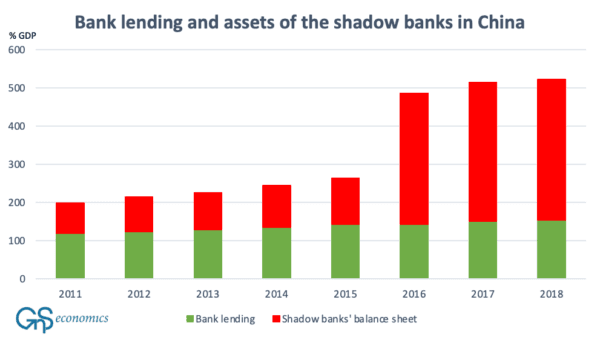

The rapid deterioration of the Chinese economy scared Beijing, and it enacted another round of massive debt stimulus. However, this time around, it didn’t come from traditional sources. The reason why so few noticed in 2016 that Beijing was running yet another enormous stimulus program was because it was orchestrated through the so-called shadow-banking sector.

Shadow banking is a term used to describe part of the financial sector that operates outside of, or is only loosely linked to, the traditional system of deposit-taking institutions. It provides credit intermediation through different institutions, instruments, and markets. Effectively, it’s a deposit-like banking system for firms and institutional investors, but because it doesn’t accept deposits in their traditional form from consumers and corporations, it mostly falls outside the banking supervision, regulative framework, and lending statistics.

Alas, China “saved” the world economy from succumbing to a recession in 2016 by issuing an unprecedented credit spree running through the shadow-banking sector.

It would be truly interesting to know what the current size of the shadow-banking sector is in China, but I have been unable to find the current estimates of it from the reports of the People’s Bank of China (PBC). This may be due to the fact that PBC doesn’t publish its estimates anymore or that it publishes them only in Mandarin, or that I have simply missed them regardless of my extensive search.

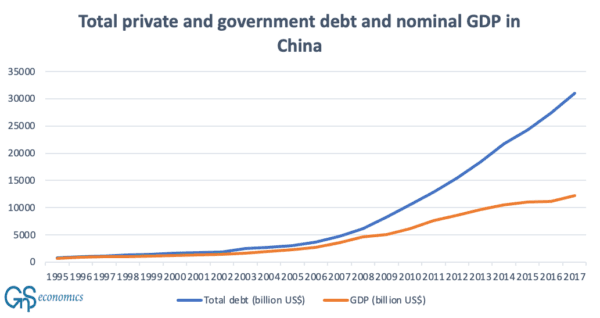

Alas, China’s economy is heading into a nearly inevitable collapse.

It’s obvious that the economic collapse of China would bring serious social unrest and even lead to an outright uprising. I consider this as the primary reason for the tightening grip of the China Communist Party on Chinese citizens. It wants to make sure that when the economy implodes, it has the means to quell the massive discontent it will give rise to.

For the world economy, this isn’t good news, as we have effectively made ourselves into an economic hostage of two totalitarian regimes: Russia and China. It should be noted that this has been our own doing. Our politicians haven’t listened to the voices warning us of the increasing economic dependence on China and Russia.

Now, we are learning that lesson the hard way. Let’s just hope this time the warning gets through to those who should listen.