The U.S.–Israeli war with Iran has brought heightened volatility to energy and equity markets, with the price of oil rising from about $65 per barrel of crude before the war to a high of $119 on March 9, before falling back to its current level of about $100. If oil supplies from the Middle East continue to be disrupted, the effects are expected to translate into higher gasoline prices in the United States.

Energy analysts say that in the coming days and weeks, there is limited potential for producers outside the Persian Gulf to make up for shortages fast enough to reverse price hikes. However, if oil prices remain elevated for an extended period, more production in the United States and South America could come online to fill the gap, although it will take some time.

In the longer term, energy markets could experience significant shifts in global production and distribution as nations move to circumvent chronic instability in the Middle East. This could provide opportunities for oil and gas producers in the United States, as well as in South America, to significantly expand their role as key suppliers to global energy markets.

Short-Term Volatility, Higher Gasoline Prices

Before the war in Iran curtailed shipping from the Gulf, about 20 percent of the world’s oil passed through the Strait of Hormuz, a 21-mile-wide passage that analysts call one of the most critical chokepoints on earth. Although not as dominant as it once was, the Middle East remains a critical supplier of the world’s energy, with most of what passes through the strait going to China, India, Japan, and South Korea.

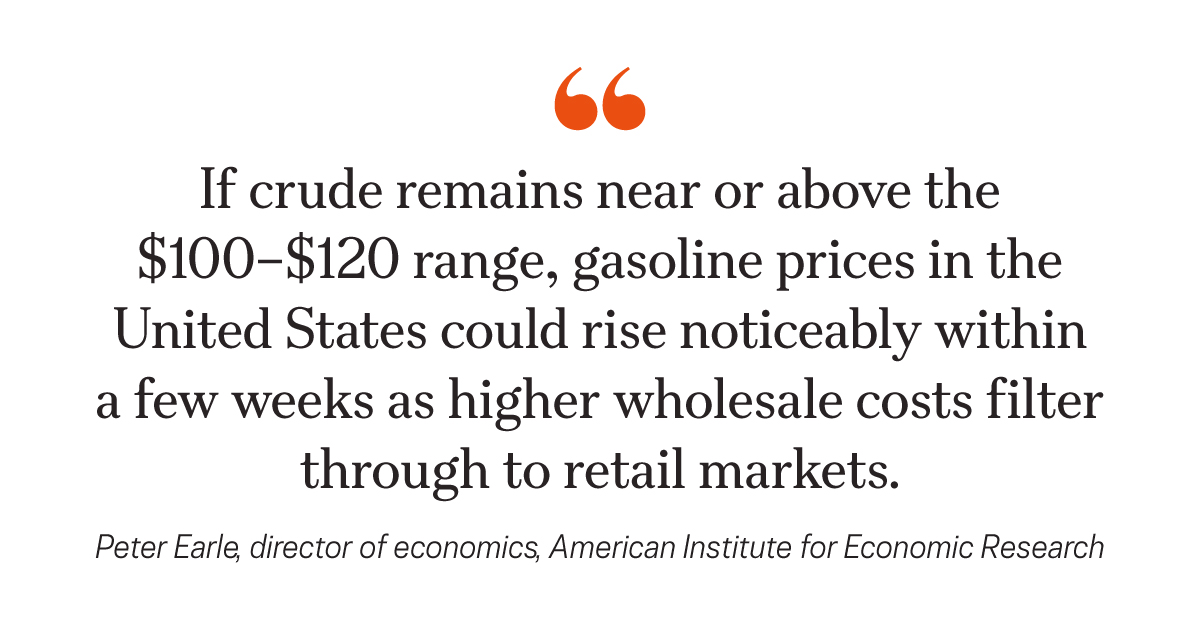

“In the near term, oil markets will likely remain dominated by risk premiums tied to shipping security and military developments in the Gulf,” Peter Earle, director of economics and economic freedom at the American Institute for Economic Research, told The Epoch Times. “If crude remains near or above the $100–$120 range, gasoline prices in the United States could rise noticeably within a few weeks as higher wholesale costs filter through to retail markets.”

For every $10 per barrel that oil rises, gasoline prices generally increase by about 25 cents per gallon at the pump, Earle said, although the recent release of strategic oil reserves, coupled with alternative distribution routes and a gradual production increase from suppliers outside the Gulf, could stabilize prices “if the conflict does not escalate further.”

However, in the near term, efforts to cope with the disruption in the Gulf are only succeeding at the margin. Pipelines constructed by Saudi Arabia and the United Arab Emirates provide an alternative to passing through the strait, but their capacity is limited.

Saudi Arabia’s East–West Pipeline, which runs from the Persian Gulf to the Red Sea, could move up to 7 million barrels of oil per day.

“[It has] not done that for an extended period of time, so this is going to be pushing that, potentially, to a limit that it’s not built for,” Caleb Jasso, senior policy adviser at the Institute for Energy Research, told The Epoch Times.

The United Arab Emirates’ Habshan–Fujairah Pipeline, which circumvents the strait and runs to the Gulf of Oman, could carry another 2 million barrels per day, but compared with the 20 million barrels that normally pass through the strait each day, this would be more “an alleviation, not a complete circumventing of total flow,” he said.

Adding to the risk of attacks in the Persian Gulf is the fact that insurers have been canceling or raising rates on shipping insurance there. The Trump administration has pledged military escorts and insurance guarantees for oil tankers, but these initiatives are still in the works.

Other efforts to meet supply shortages include releasing oil from strategic reserves. On March 11, the International Energy Agency announced that it would release 400 million barrels of oil from its reserves. This is more than double the amount that was released in 2022 to cope with rising energy prices after Russia invaded Ukraine, and would equate to about 20 days of normal traffic through the Gulf.

Stepping Up US Oil and Gas Production

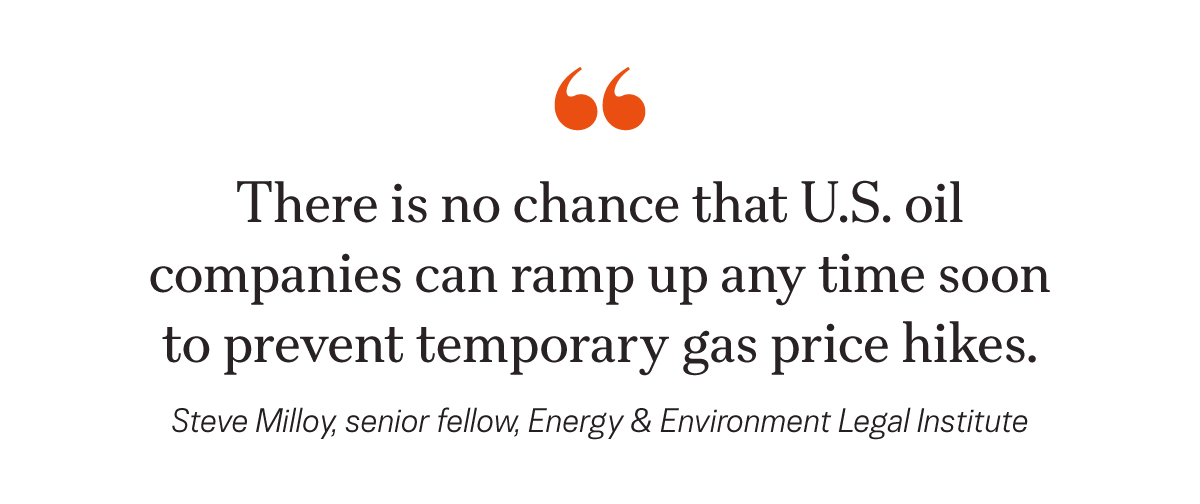

Some are hopeful that the United States can step up its production, but analysts say this will take time.“There is no chance that U.S. oil companies can ramp up anytime soon to prevent temporary gas price hikes,” Steve Milloy, senior fellow at the Energy and Environment Legal Institute and former adviser to the Trump administration, told The Epoch Times.

“We are producing at record levels, and this only covers about two-thirds of our daily needs. We could improve this in the future, but that would be in the future.”

Given the extensive volatility in oil markets, many U.S. producers have now been focusing on hedging prices rather than adding new drilling rigs, Alex Stevens, a policy expert at the Institute for Energy Research, told The Epoch Times.

“In the United States, most of the producers need oil sustained in the $85-or-above range before they’ll start thinking of adding more rigs,” Stevens said. The fact that new drilling activity has been limited, he said, is likely an indication that producers are not yet convinced that oil prices will remain elevated for long.

Once American producers commit to expanding their drilling infrastructure, it will still take time to get wells up and running.

“Shale production cannot ramp up instantly,” Earle said. “Drilling programs, labor availability, pipeline capacity, and financing conditions mean it typically takes several months before higher prices translate into significantly higher output. In the short run, U.S. producers might add a few hundred thousand barrels per day, which is small relative to the roughly 20 million barrels per day that normally move through the Strait of Hormuz.”

South American nations such as Venezuela, Guyana, Argentina, Brazil, and Colombia also have the potential to increase production. However, Venezuela, which has the world’s largest proven reserves, has been severely hampered in its ability to produce by decades of mismanagement and neglect under socialist rule.

“Output today is only a fraction of what [Venezuela] produced two decades ago, and restoring production would require significant capital investment, technical expertise, and time,” Earle said. “Even under optimistic conditions, Venezuelan production could probably increase only gradually, perhaps adding a few hundred thousand barrels per day over time.”

For these reasons, markets will likely remain volatile and prices elevated as long as Gulf shipping remains a high-risk venture. However, over time, these all remain viable sources to boost production outside the Gulf and bring energy prices back down to prewar levels.

Long-Term Adjustments

Longer term, the global industry has the potential to shift production and distribution away from the Middle East. The United States already gets the vast majority of its oil either domestically or from sources in the Western Hemisphere, and has been working under the Trump administration to further solidify America’s energy security while boosting energy exports.

“I would imagine you will see policy pressure to have a lot more export capacity for liquid natural gas and for crude oil,” Stevens said.

South American nations could likewise take on a larger role in supplying oil and gas, according to experts.

“You’re going to see a greater push for global diversification away from the Middle East,” Jasso said. “[The Strait of Hormuz is] a chokepoint where, no matter what, Iran is always going to have the ability to cause a lot of chaos.”

Another area that may see longer-term changes is refining capacity. Despite the fact that the United States is the top producer of oil and natural gas, there has not been a major new oil refinery built in the United States since the 1970s.

“If you’re relying on other countries for refining capacity, that can be a bottleneck, and if there’s geopolitical conflict, that can disrupt the market,” Stevens said.

The Iran War and China

Some have speculated that one reason the United States took military action against Iran and Venezuela is the fact that both are key suppliers and client states of China. Whether or not this was part of the rationale to go to war, the impact on China is among the consequences.

“China is the world’s largest oil importer and relies heavily on supplies from the Persian Gulf, so any disruption around the Strait of Hormuz has immediate implications for its energy security,” Earle said. “Even if shipments continue, insurance premiums, costs of freight, and longer shipping routes can raise the effective price of oil delivered to Chinese refiners.”

“If the U.S. can control Venezuelan and Iranian oil production, Trump will be the first U.S. president to gain a strategic leg up on China,” Milloy said. “China’s Achilles’ heel is that it is relatively oil poor and dependent on global production to a much greater extent than the U.S.”

And because of embargoes, China is able to buy from both at a discounted price, although that could be coming to an end.

If the United States can gain control over exports from Iran and Venezuela, it would be “a major strategic advantage for the U.S.,” Milloy said, noting that this could possibly constrain China’s ambitions to invade Taiwan or affect its ability to maintain dominance in markets such as electric batteries.

However, even if these oil supplies are cut off, analysts say, China has other options.

Jasso said that losing the supply from Iran and Venezuela would affect China, but that it would not “necessarily destroy [China’s] economic viability.”

“It’s going to be a challenge for them, but it’s likely that they could call up [Russian President Vladimir] Putin and say, ‘We need more oil,’ and Putin would be very happy to get even more revenue from China,” he said.