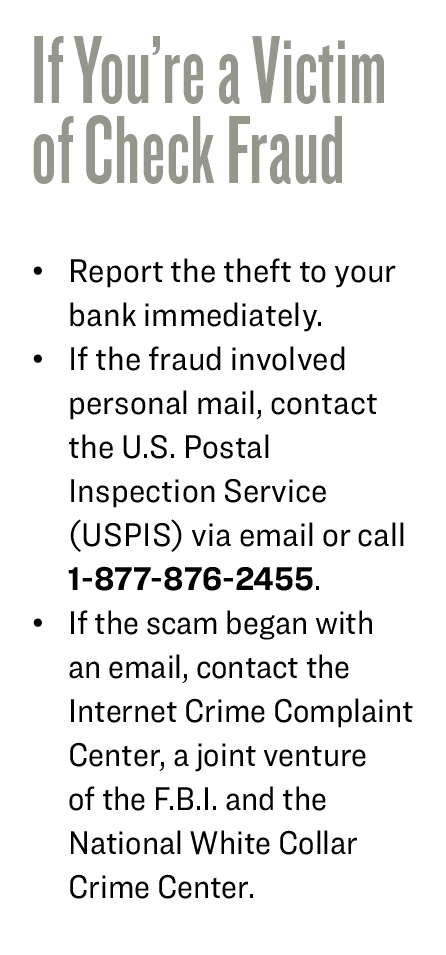

Every year, enterprising thieves find new ways to separate people from their money. In many cases in the United States, this involves several methods of check fraud, which occurs when thieves use a personal or business check to steal money, services, or goods.

The Boston Fed reports that the United States Federal Reserve System collected a total of 19 billion in 1993. By 2022, the number of checks collected had declined to approximately 3.4 billion.

This smaller, yet still significant number leaves many opportunities for thieves, who steal mail from residential and United States Postal Service blue mailboxes. They sort through stolen mail, searching for personal and business checks, as well as bank account and routing numbers. The USPS reported 38,500 mail thefts in 2022, and 25,000 in the first half of 2023.

Despite the use of checks becoming less common, due largely to the ease of online banking, the incidence of check-related crimes continues to increase. According to a report issued in 2023 by the Federal Reserve Bank of Boston, the number of checks collected on an annual basis over the past 30 years by the Federal Reserve declined by 82 percent. There were approximately 680,000 reports of check fraud in 2021, double the amount reported in 2020. A 2024 NASDAQ report indicated just over $21 billion in check fraud.

The term “check fraud” covers a lot of territory, but the one factor all variations have in common is that an innocent person loses money or goods.

Criminals use stolen checks to commit check fraud, often from residential mailboxes or USPS collection boxes. JJ Gouin/iStock/Getty Images Plus

One example is called paperhanging, in which a person writes a check from an account they opened, knowing there are insufficient funds on deposit to cover the amount. Other frauds include check washing, forgery, the use of counterfeit checks, and overpayment.

In check washing, thieves remove the ink from the check, often by applying acetone, then write in a new date, amount, and payee information.

Forgery involves intercepting and stealing new checks from mailboxes or collection boxes when they are being mailed to the account holders, then forging the signature to use them to drain bank accounts.

According to RelyCo.com, a business check printer, more than 500 million checks are forged each year in the United States alone. Due to the sheer volume of incidents, only 25 percent of the cases are prosecuted.

“Residential mailboxes are fertile grounds for scammers,” Zulfikar Ramzan, Chief Scientist and EVP of Product and Development at Aura, a digital safety platform that protects people against scams, told The Epoch Times. “Do not leave your mail unattended; send checks via a post office collection box when at work, or hand them directly to your carrier.”

He advised, “Whenever possible, eliminate the use of paper checks altogether.”

Writing Checks: Precautions to Take

Mr. Ramzan offered a clever yet simple tip to help avoid falling victim to stolen checks, “Use indelible black gel ink pens. The Better Business Bureau (BBB) urges consumers to sign their checks with long-lasting (indelible) black gel ink. This ink is particularly tough to scrub off, making it nearly impossible for scammers to erase the original contents of the check.”

To prevent fraud by means of "check washing," in which the payee and check amount are changed, experts recommend using an indelible black gel ink pen to write checks. Andrey_Popov/Shutterstock

Michael Scheumack, chief innovation officer at IdentityIQ, a private firm providing identity protection for consumers, suggested restricting the check. That way, it can only be deposited in the bank account of the intended recipient. “To do this, you should write ‘For deposit only’ on the back of the check where the signature goes.”

Additionally, “You should never include additional personal details, such as your date of birth, driver’s license number, or Social Security number, on the check,” Mr. Scheumack said.

Monitor your checking account. “Use your online banking features. Be on the lookout for any discrepancies in amounts paid out, or any overdraft notices, reconciling the records every 30 days,” Mr. Ramzan said.

He further advised consumers, “Always shred sensitive documents such as unused or canceled checks, pre-approved credit notices, and bank statements before discarding them.”

“Scammers can steal these out of the trash and ‘wash’ them,” he explained. “Make a point to examine your check supply regularly, and report any missing checks to your bank. And never write checks payable to ‘cash’ or ‘bearer’ since anyone can take that money.”

As a final word of caution, Mr. Ramzan advised using a bank that provides checks with at least one of the following features:

- a mixture of visible and invisible fibers that can be seen under close examination or by exposure to UV light.

- a 3D, reflective holostripe made of metal that makes counterfeiting almost impossible.

- high-resolution microprinting as a font around the border of the check, which is difficult for scammers to replicate.

- watermarks that are only visible at certain angles, and can’t easily be copied.

- chemical voids that produce the word VOID if photocopied or exposed to “washing” chemicals.

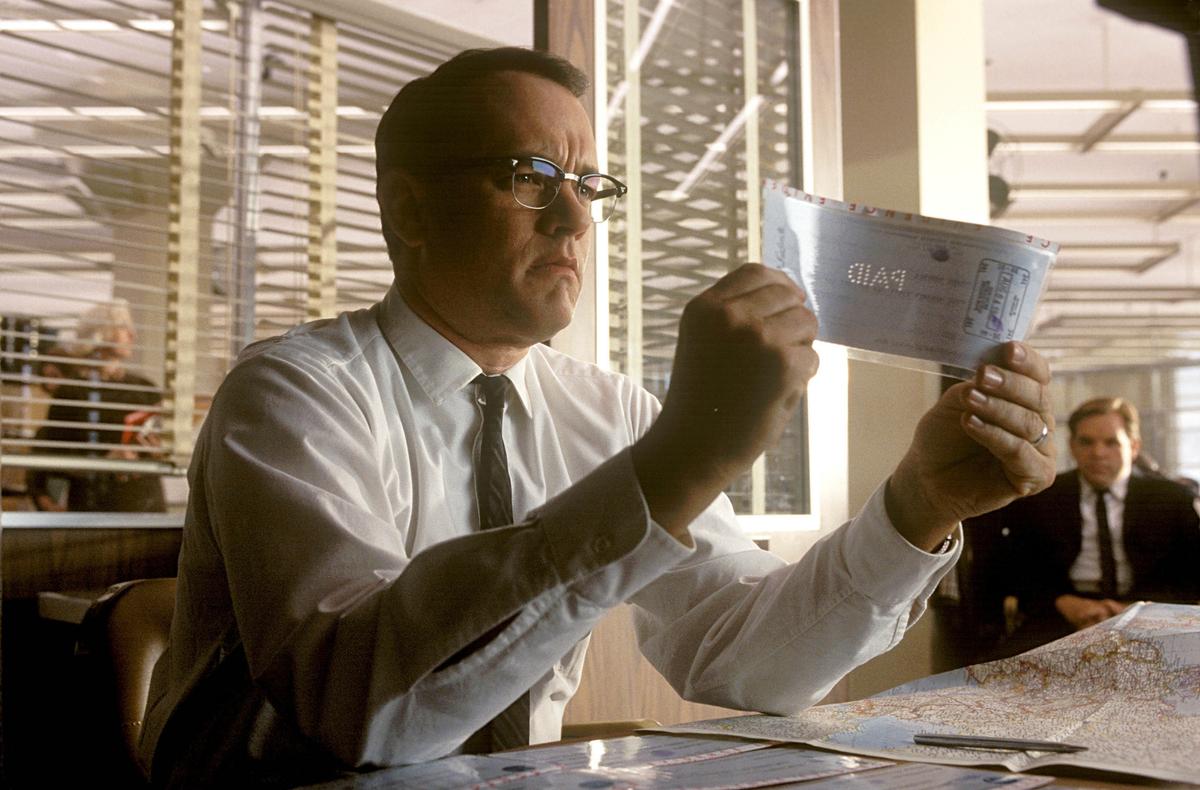

Counterfeit Scams: When It’s Too Good to Be True

The common factor in most “too good to be true” scams is how they use the lure of “easy money” to deceive victims.Thieves with access to advanced graphics programs and printing equipment can create very authentic-looking counterfeit checks. In one instance, scammers convince unwitting victims to cash or deposit the counterfeit checks. Then they ask the victim to refund some portion of the amount very quickly, or forward it to another person in the form of cash, a prepaid debit card, a personal check, a bank electronic wire transfer, or a person-to-person transaction like Zelle. When the victim becomes aware of the fraud, they can never reclaim the funds they sent.

Counterfeiters can produce very realistic checks, complete with watermarks, making close inspection a must. A scene from the film “Catch Me If You Can,” where Tom Hanks plays an FBI agent trying to track down a con artist played by Leonardo DiCaprio. MovieStillsDB

Here are some examples of scams:

- You were hired as a mystery shopper after responding to an online ad, and were sent a check as initial payment before doing any work, with instructions to deposit it and send a portion to another mystery shopper. This is a scam designed to steal the amount forwarded.

- You’ve been advised you won a lottery or other cash prize. As a “winner,” you are asked to deposit the check, then send funds to cover taxes and processing fees.

- Someone purchases goods from you. You are overpaid by the buyer, and asked to send a check for the difference.

“Do not deposit these checks, or checks from unknown senders, or checks associated with out-of-town banks.” He also advised closely scrutinizing the check date, sender name, and financial institution for errors or dubious characteristics.