The U.S. federal government has borrowed so much money that, over the past year, it has had to spend one-fifth of all the money it collected just on debt interest—which came to almost $880 billion. This fiscal year, interest is expected to reach over $1 trillion.

Americans paid some $450 billion less in income taxes for the year, trapping the government in the pincers of a fiscal crunch.

The country teeters on the brink of a debt spiral that could devolve into a fiscal crisis or hyperinflation, several economists told The Epoch Times.

“The problem is serious because, any way you cut it, taxpayers are paying interest on the mountain of debt that has been accumulated,” said Steve Hanke, a professor of applied economics at Johns Hopkins University. “In short, they are paying something for nothing.”

Congress must dramatically curb deficit spending to instill confidence in investors—who seem to be losing faith in America’s ability to satisfy its obligations, some suggest.

“Deficit spending by the U.S. government is in a runaway scenario,“ said Mark Thornton, a senior fellow at the classical liberal Mises Institute. ”The amount of money that they’re borrowing is at extremely elevated levels and there doesn’t seem to be any regulation or even mild attempts to curb the spending side of the fiscal equation.”

Gigantic Debt

Government debt stood above $33 trillion in fiscal year 2023 (the 12 months that ended on Sept. 30). That’s about $1.7 trillion more than the year before. Interest on the debt has been growing steadily for decades, although at a relatively slow pace to about $570 billion in 2019 from about $350 billion in 1995—an annual increase of some 2 percent.

With the explosion of government spending during the COVID-19 pandemic and the subsequent interest rate increases by the Federal Reserve, the debt cost has skyrocketed by more than 50 percent between 2019 and 2023. Over the past year, it has already surpassed the entire military budget.

The cost is expected to keep growing as old debt issued at low interest rates matures and is rolled over into higher rates.

While the government pays some of the interest to itself, as it holds about 20 percent of the debt in various trusts and funds, interest from that portion of the debt is supposed to pay for future expenses of programs such as Medicare and Social Security.

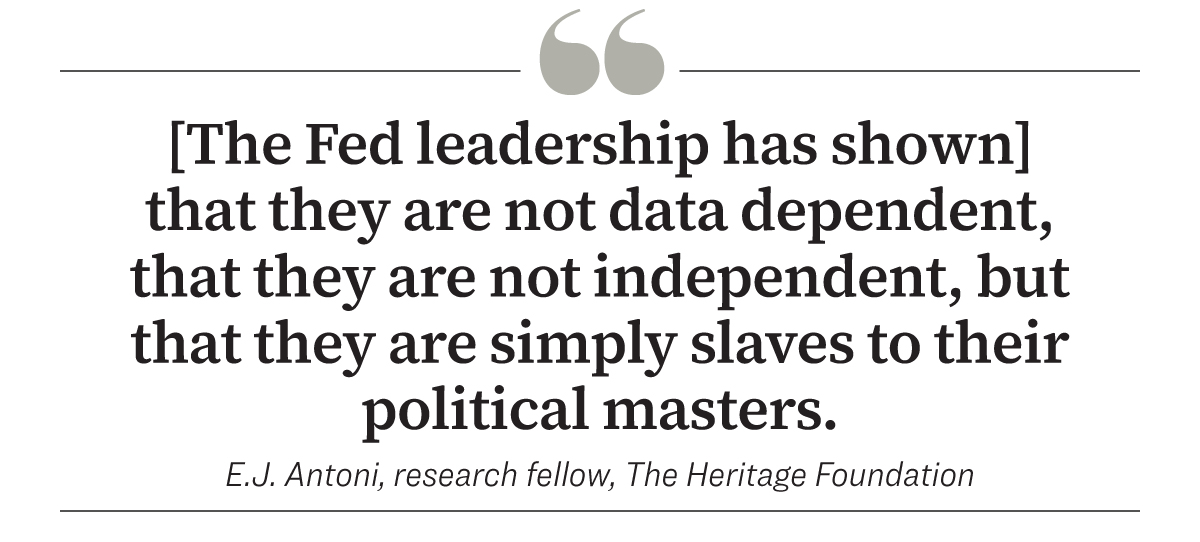

“That money is already slated to go out the door. It just hasn’t gone out the door yet,” said E.J. Antoni, an economist and research fellow at conservative think tank The Heritage Foundation.

“It’s not as if the government has that cash on hand to spend.”

Who Pays?

Proponents of large government deficit spending have argued that servicing the debt isn’t much of a worry since the Fed can print the cash necessary to cover the interest or even buy up the debt. The Treasury would then pay the interest on the debt to the Fed, which would then use the money to cover the cost of its operations and send the surplus back to the Treasury. The government would, in effect, pay the interest to itself.Indeed, about 20 percent of the government debt is held by the Fed already.

However, the reality doesn’t necessarily follow this logic.

“The Federal Reserve doesn’t actually make money anymore,“ Mr. Antoni said. ”They lose money because so much of the Treasurys that they have on the books right now [were] purchased in 2020 and even early 2021 when rates were near zero, so those assets are earning almost nothing,”

Anything the Fed does collect on its portfolio, it immediately pays out to banks and money market funds in interest on reserves and reverse repurchase agreements. The point of those operations is to stem inflation—“keeping liquid cash locked in its vaults so that it can’t multiply in the banking system,” he said.

These operations now cost the central bank some $700 million per day, forcing it into a “huge deficit,” Mr. Antoni said.

“It’s not sending Treasury a dime.”

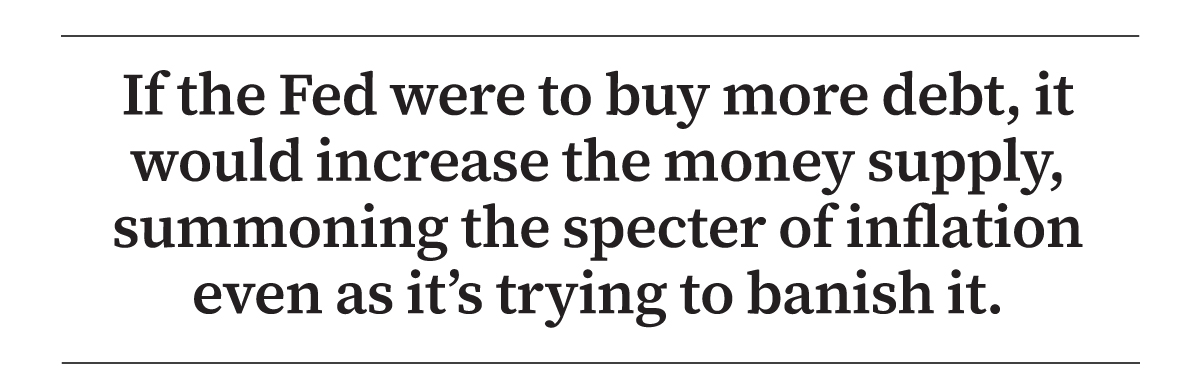

For the same reason, the Fed seems to lack the appetite for more government debt. Over the past year and a half, it has been slowly reducing its debt holdings, siphoning cash out of the market to curb inflation.

“Any time the Fed buys something, they do it with money that’s being created for that purpose,” he said.

“The Fed actually doesn’t have an account with any balance. Their checking account literally has zero balance so when they sell an asset, the money that goes into that account is extinguished. When they buy an asset, the money that comes out of that account is just created.”

If the Fed were to buy more debt, it would increase the money supply, summoning the specter of inflation even as it’s trying to banish it.

Bad Credit?

If the government wants to borrow without worsening inflation, it needs to find somebody to buy the debt with existing dollars.Until recently, that hasn’t been a problem. Despite offering measly interest, U.S. Treasurys served as a safe haven investment—a hedge against risk and an indispensable collateral in complex investment schemes in financial markets.

“U.S. Treasurys were seen as the safest asset. And increasingly that’s not the case today,” Mr. Antoni said.

In August, the Fitch rating firm downgraded U.S. debt to AA+ from AAA.

On Nov. 9, the Treasury had the worst auction of 30-year Treasurys in more than a decade as investors demanded a premium to buy the bond. Demand was down by almost 5 percent from the month before.

On Nov. 10, Moody’s, another rating firm, lowered the U.S. debt outlook to “negative” from “stable,” arguing that polarization in Congress is likely to thwart fiscal reforms.

“People are increasingly realizing today [that U.S. Treasurys] aren’t safe at all,” Mr. Antoni said.

He pointed out that “violent changes” in monetary policy can dramatically affect bond prices.

Nobody would pay the full price of a bond that pays 2 percent annual interest when the Treasury now offers plenty of bonds that pay 5 percent.

“If you bought a government bond, for example, in 2020, it’s lost about half of its value, so you just can’t sell it,“ Mr. Antoni said. ”You’re essentially stuck with that low rate of return.”

Accounting for inflation, the older bonds are now, in fact, losing their owners money, but at least they return something.

“That’s still typically better than the losses you would take if you sold it outright,” he said.

Then, there’s the default risk. Investors are aware that the government will likely one day be unable to pay its debts. So far, that hasn’t been much of an issue, partly because of the “greater fool strategy,” as he put it.

“‘I’m betting that there’s a bigger fool out there who, after I want to sell, is still willing to buy, even though that Doomsday, if you will, is right around the corner,’” he said, summing up the strategy.

“That may sound silly, but there are plenty of investors and investments that operate on that principle.”

The cooling of demand for the 30-year bonds may be a sign that investors are gradually losing confidence that such a fool will be available over the long haul. The Treasury seems to be responding by offering more of the shorter maturity bonds, according to Mr. Antoni.

Yet inflation poses a similar risk to a default, he said, noting that the dollar has lost about 17 percent of its value over the past few years.

“It’s the same as if the Treasury were to turn around and only pay 83 percent of the bondholders and tell the other 17 percent to go pound sand,” he said.

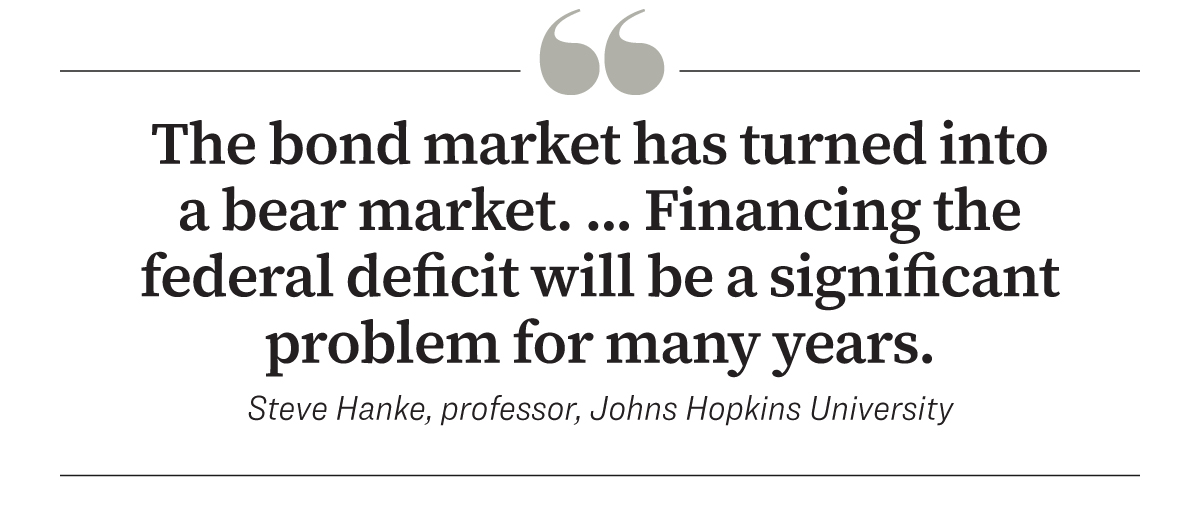

All these factors seem to be souring investor confidence in the bonds. And once spoiled, investor trust is hard to restore, according to Mr. Hanke.

Even if the Fed were to cut rates again, it may not necessarily solve the problem, he said.

Debt and War

Geopolitical interests have seemingly turned against the government bond market too, particularly with China exiting its massive position in U.S. Treasurys.“At this point, it’s becoming not just a financial issue, but a national security issue,” Mr. Antoni said.

At the current pace, China could be U.S. debt-free in a few years, in what he expects to be a preparation for war.

“It effectively isolates you from the Treasury’s ability to selectively default,” Mr. Antoni said, referring to the government’s canceling of its debt held by another country as a form of economic sanction.

“If we borrowed a bunch of money from China and then China turns around and invades Taiwan, we can say, ‘You know what, all of our debt that China owns—it’s now voided. We’re not going to pay that money back,’” he said.

Such a step could have been used against Russia upon its invasion of Ukraine, “except that Russia already sold off all their holdings of U.S. debt,” Mr. Antoni noted.

“So I think it’s reasonable to believe that China getting rid of all its U.S. debt could be a prelude to war,” he said.

Fortunately for the United States, China isn’t trying to flood the market with its stash of U.S. Treasurys, but mostly letting them expire and not buying more. The likely reason is that it bought the bonds at times of low interest and would have to sell them much cheaper now, Mr. Antoni said.

Who’s to Blame?

It would seem most obvious to blame excessive government debt on the government, particularly Congress. But the economists put much of the blame on the Fed.It’s true that lawmakers are responsible for approving the budget and, regardless of party, have long failed to balance it. But it’s the Fed that has made borrowing so expedient by setting interest rates extremely low for much of the past two decades.

“[Before that,] for many years, the debt did not grow as much because it would have been prohibitively expensive to grow it,” Mr. Antoni said.

Mr. Hanke said, “The Fed should be blamed for allowing the money supply to expand at an excessive rate.

“Inflation is always and everywhere a monetary phenomenon. And, as night follows day, interest rates follow the course of inflation. So the Fed, by not paying attention to the rate of growth in the money supply, is a culprit.”

The Fed’s buying up of government debt during the gargantuan pandemic spending set off the inflation avalanche and continued well into 2022, even after the pandemic effectively ended.

“Exhibit 1 is ironically titled the ‘Inflation Reduction Act,’ an act that is filled with government subsidies and giveaways,” Mr. Hanke said.

The initial round of COVID-19 spending in 2020 didn’t cause much inflation because the Fed spent the two prior years slightly tightening the money supply, according to Mr. Antoni.

“You had an economy that was growing quickly, and you had money supply that was shrinking, both of which are very deflationary,“ he said. ”So as a result of that, there was a lot of cushion, if you will, built into the economy to absorb all of that excess spending in 2020. Inflation takes off in 2021 because that cushion is no longer there. So anything else was just fuel on the fire.”

He has no confidence that the Fed will keep rates high long enough to put the inflation boogeyman back in the closet.

“We’re still not back to pre-pandemic levels of price increases and people just have no confidence that the Fed is going to get us there,” he said.

Mr. Thornton argued that “the Fed has very little prospects of doing anything that wouldn’t cause secondary problems.”

What to Do?

If the Fed isn’t up to solving the problem, it will be up to Congress to step in. However, it'll take a “tremendous jolt” to move the needle, according to Mr. Thornton.“It really needs to be across-the-board spending cuts that capture the attention of investors, business leaders, entrepreneurs, workers,” he said.

However, it need not necessarily be complex.

“All you have to do is just reset every budget, every government benefit, every government paycheck back to, say, 2018 levels,” Mr. Thorton said.

“That would solve the problem. It would solve the fiscal problem, it would solve the psychological problem that people are having about the U.S. economy.”

Such cuts would be inevitably called “draconian” in the media and would need to be large enough to “upset” government workers as well as beneficiaries of government programs, he noted, suggesting a major political sacrifice.

At the same time, the government would have to take steps to reinvigorate the economy by cutting taxes and barriers to business, he said.

Mr. Thorton pointed to Alabama’s new rule that frees overtime work from state income tax.

“That’s the type of thing we need to be doing on a much larger scale and we need to be doing it nationally,” he said.

“Hopefully, you’ll see politicians responding with at least some efforts in the right directions, but they’re going to have to really make some significant progress and very quickly and I would not bet right now that they’re going to do enough.”