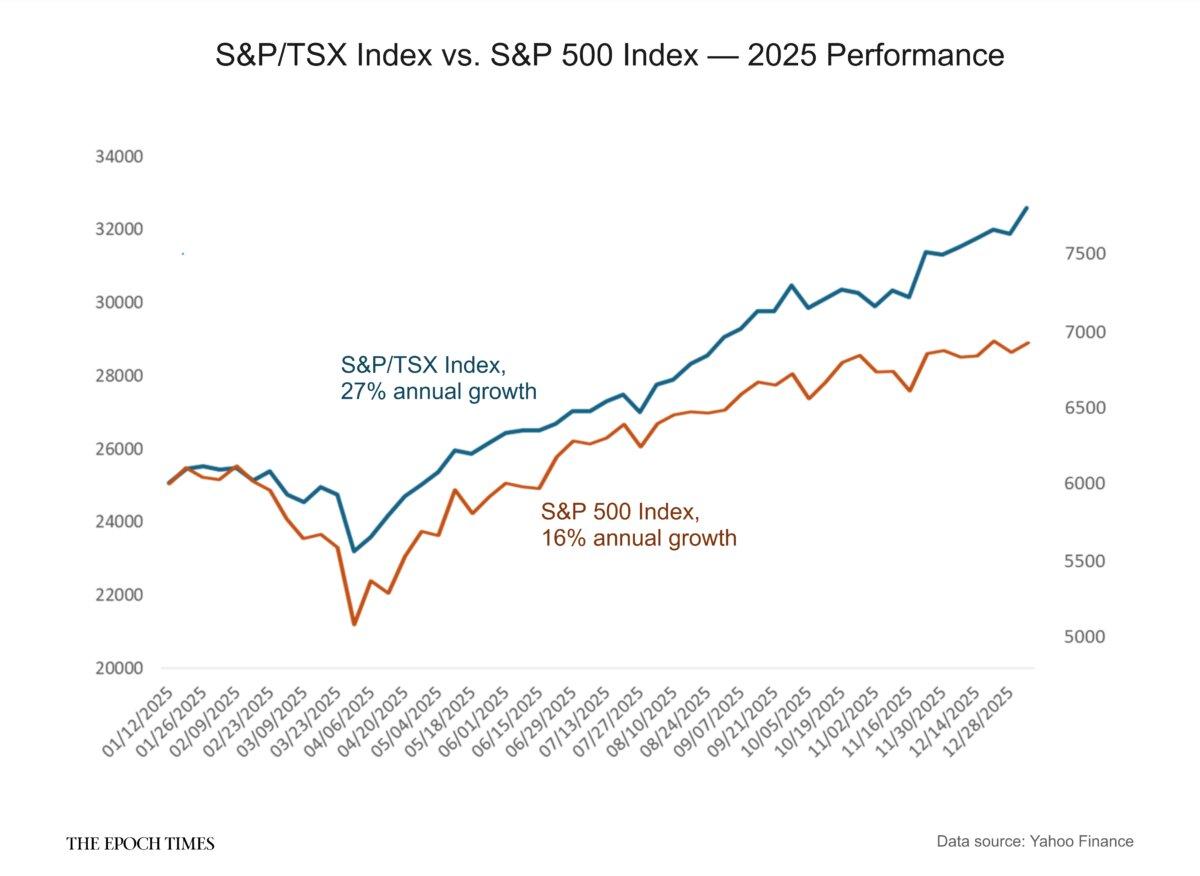

As implausible as it may seem, the Toronto stock market left its American counterparts in the dust last year, despite Canada’s economy being burdened by U.S. tariffs and grappling with its own productivity issues.

Economists attributed this to an outperformance of natural resource stocks due to surging prices of precious metals like gold and silver, which hold a greater weight in the S&P/TSX Composite Index compared to its American counterparts. A lower Canadian dollar and several Bank of Canada interest rate cuts also helped to boost investment.

The stellar performance of the TSX could be seen as surprising, considering that the administration of U.S. President Donald Trump imposed tariffs on Canadian exports while also enacting business-friendly policies domestically.

While the TSX could continue outperforming in 2026 if commodity prices keep rising and foreign capital continues chasing Canada’s resource sector, analysts expect Canada’s stock market growth to be milder this year than it was in 2025.

Porter said the rate cuts in Canada have “definitely helped support the market indirectly.” The TSX could continue outperforming U.S. indexes in 2026 if commodity prices continue to grow, he added.

“I suspect it'll be a close call between [the indexes as to] who performs in the year ahead,” Porter said. “The valuation gap is not as clear-cut a positive for Toronto as it was last year, and so ultimately, it may come down to just how commodity prices fare in the year ahead.”

Kevin Headland, co-chief investment strategist with Manulife Investments, said gold financials and Shopify were responsible for roughly 65 percent of the TSX’s outsized performance in 2025. He also said the S&P 500 saw a larger sell-off following Trump’s “Liberation Day” tariff announcements in April 2025.

“When you start the year, or the first quarter, off a big decline, it’s hard to climb out of that hole,” he said of the S&P 500.

Headland projected that the TSX could see its “momentum” continue if more foreign investment comes into the country for gold, similar to what took place in 2025, but he said he “would be hard pressed to see a similar type of performance for TSX this year as it was last year.”

Headland said that Canada’s stock index is not seen as undervalued as it was before and that earnings growth is not likely to be as high this year. He said he expects that the TSX and S&P 500 could be “perhaps more in line with each other in 2026 than we saw in 2025.”

Carleton University professor of business Ian Lee said a weaker Canadian dollar relative to the U.S. dollar—which “creates perceived values, because you can buy cheap [in the TSX] by converting into the Canadian dollar”—also boosted stock values in 2025.

Outperformance in 2025

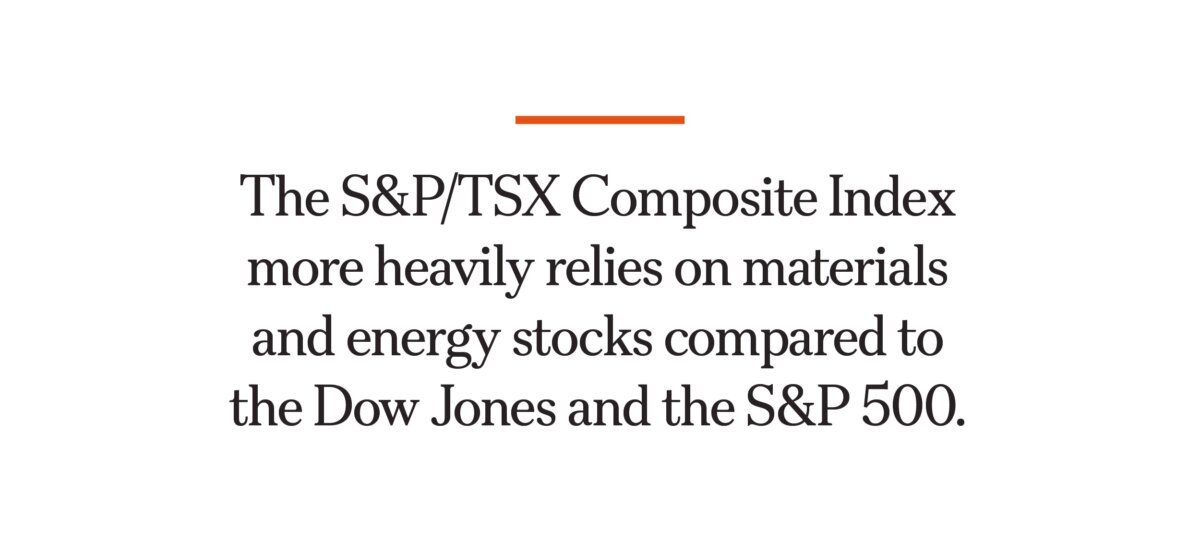

The S&P/TSX Composite Index, compared to the Dow Jones and the S&P 500, more heavily weighs for materials and energy stocks, both of which performed well in 2025 in relation to other sectors like information technology and communication services. The vast majority of the “weight” in the S&P/TSX Composite Index is made up of Canadian stocks, but it also has the S&P 500 weighted at 0.6 percent.

Lee said that silver and gold going “through the roof” helped the TSX’s performance because it is more heavily weighted in commodities than its American indexes.

“I don’t think it’s because the Canadian economy is a better investment overall than the U.S. If you look at any of the metrics, whether it’s productivity or whether it’s the GDP growth rate, the U.S. economy is stronger and doing better,” he added.

BMO’s Porter said the TSX tends to outperform the S&P 500 when commodity prices are rising, but 2025 had “nuance” because some commodities did not perform well, while others like gold miners and fertilizer companies “almost doubled.”

Porter said that even if gold is taken out of the commodities picture, the TSX would have still outperformed the S&P 500 in 2025, which he said is “very impressive” given the headwinds facing the Canadian economy due to U.S. tariffs.

By contrast, Porter said financials and consumer discretionary stocks did not do as well as commodities. Financials include banks, insurance companies, asset managers, and wealth managers, while discretionary stocks include retail, travel and leisure, restaurants, and entertainment.

Financials constitute 33.1 percent of the S&P/TSX Composite Index, whereas consumer discretionary stocks account for 3.3 percent. In contrast, for the S&P 500, financials represent 13.4 percent, while consumer discretionary comprises 10.4 percent.

Other factors having an impact on boosting the Canadian stock market include the Bank of Canada cutting interest rates faster than the U.S. Federal Reserve, said Porter. The Bank of Canada cut interest rates four times in 2025, to the current 2.25 percent, while the Federal Reserve cut rates just three times, to 3.75 percent.

Trend Continues in 2026?

Porter said that the TSX could continue outperforming U.S. indexes in 2026 but that this would likely depend on whether commodities continue to perform well.Headland said that with investors coming to Canada to “chase” the gold market in 2025, that trend could continue with investors searching for undervalued mining and energy stocks.

The BMO report said West Texas Intermediate (WTI) crude oil prices are likely to remain at an average of US$62 a barrel in 2026, down from US$65 a barrel in 2025, as “fears of a growing oil market glut remain the dominant concern and are likely to continue to weigh on prices in the near term.”

Headland said oil will likely be in a “tight trading range” in 2026 due to lower demand and to supply being maintained at the same level. “Therefore we don’t see much of a tailwind in energy companies as a result of just the commodity price increase, or lack thereof,” he said.

If the Canadian dollar were to rise in value after the U.S. Federal Reserve decreases interest rates, that could also increase profits for foreign investors and drive Canadian stock prices higher, Headland said.

If the Canadian dollar were to rise in value after the U.S. Federal Reserve decreases interest rates, that could also increase profits for foreign investors and drive Canadian stock prices higher, Headland said.He said action by the Canadian government could improve the “perception” of the value of energy and resource stocks for investors. “If the Canadian government remains committed, and we start getting closer to shovels in the ground, I think investors could be interested in certain areas of our material sector, which would ultimately be positive for the TSX,” he said.

The Conservative Party has criticized the MPO, saying the federal government should instead remove measures like the Impact Assessment Act that make it more difficult to build projects. The party said Ottawa should simply “get out of the way” and encourage development by cutting taxes and red tape.