Now, combine strengthening global demand for oil with supply concerns due to U.S. sanctions on Iran, Venezuelan production falling, and OPEC output cuts and the price of West Texas Intermediate (WTI) has risen by 40 percent in the last year to levels not seen since 2014.

So this should be good for Canada, right? Unfortunately, not quite. The link between rising oil prices and Canada’s oil-exporting economy is murky.

The biggest reason why the Canadian economy won’t reap the full benefits of rising oil prices this time is pipeline uncertainty. A secondary reason, says BMO chief economist Doug Porter, is the more competitive tax treatment in the United States. Both factors effectively dampen the capital spending that oil and gas companies would make in Canada, which would lead to greater economic growth and job creation.

Back when the price of a barrel of WTI was well north of US$100 in 2014, the view was that pipeline issues would sort themselves out. “It was an issue back then, but it wasn’t seen as a clear and present danger,” Porter said in a phone interview.

Traditionally higher oil prices have led to a higher Canadian dollar. But not this time. The loonie is being held back by NAFTA uncertainty and a stronger greenback, which is supported by a greater potential for interest rate hikes from the U.S. Federal Reserve and more robust U.S. economic growth.

According to BMO, the historical relationship between the loonie and oil suggests that the currency should be almost 10 cents higher with oil at these levels. Earlier in May as oil reached its highest level since 2014, the loonie plunged to a two-month low near US$0.77.

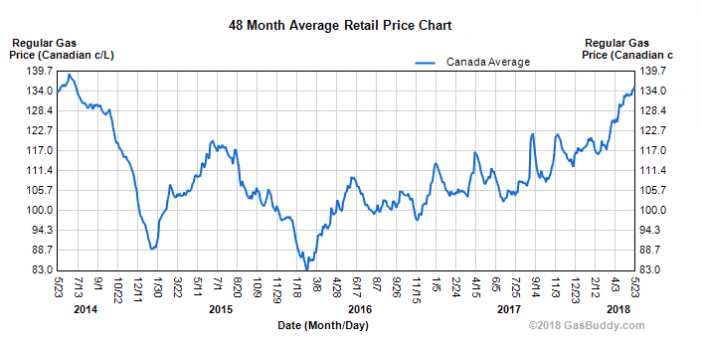

Now, the lagging loonie isn’t shielding consumers from rising oil prices, which is impacting them at the pump. Back in 2013 and 2014, the loonie averaged over US$0.90. Now, with the loonie trading below US$0.80, the Canadian consumer isn’t as insulated against oil price increases. The average Canadian gas price is the highest it’s been since mid-2014.

Higher Rates

The sharp rise in oil prices and its effects on inflation and long-term interest rates is one of the current challenges for central banks. For the Bank of Canada, its April quarterly projections were based on WTI at US$60 a barrel and oil is now nearly 20 percent higher.“I would say the one thing that most of us and the market’s probably been surprised by is the strength in oil prices,” Porter said, attributing the rise in long-term bond yields to this factor. The Canadian 10-year bond yield reached its highest level since early 2014.

The rise in long-term Canadian bond yields also reflects their rich valuation relative to U.S. long-term bonds, according to Andrew Kelvin, senior Canada rates strategist with TD Securities. Canadian bonds often take their cues from their U.S. counterparts and the U.S. 10-year bond yield is at its highest level since mid-2011. In essence, the timing for the rise in oil prices turns out to be poor as it amplifies the rise in Canadian long-term interest rates.

TD also makes the point that the move higher in Canadian rates is not because of expectations for better economic growth.

Risk and Reward

It is hard to pin down a “magic number” for the price of oil at which the economic dynamic dramatically worsens. At current levels, U.S. shale oil drilling should pick up, in the absence of logistical challenges, and put downward pressure on prices.But oil prices have gotten to the point where investors are starting to view them as a threat to global growth, should they push much higher.

The one bright spot for Canada is the rally in the energy-heavy TSX. After lagging the S&P 500 by over 13 percent in 2017, it has outperformed the U.S. benchmark index by more than 5 percent in the last three months, with energy up over 11 percent. That should put some money back in consumers’ pockets.