As the first round of the banking crisis fades, the market is refocusing on inflation and interest rate hike. Although U.S. inflation did come down, whether measured by consumer price index (CPI) or personal consumption expenditure (PCE), the year-over-year (YoY) downtrend was slow, and the month-over-month (MoM) decline was not persistent. For other advanced economies, the inflation downtrend is also uncertain, with some seeing rebounds in recent months. Against this backdrop, quite some central banks are cautious about ending tightening now.

For the time being, we confine our discussion to the United States as the Fed’s decision is the most indicative and influential. Three quarters ago, overall YoY inflation was higher than the core one by two to three percent—depending on whether the CPI or broader PCE measure is used—but now the gap is only 0.5 percent (for both measures). Core CPI inflation came down slowly while core PCE inflation stayed flat over the recent four data releases, suggesting overall inflation might not easily move down quickly as overall inflation converges to the core one, probably what the Fed is suspecting.

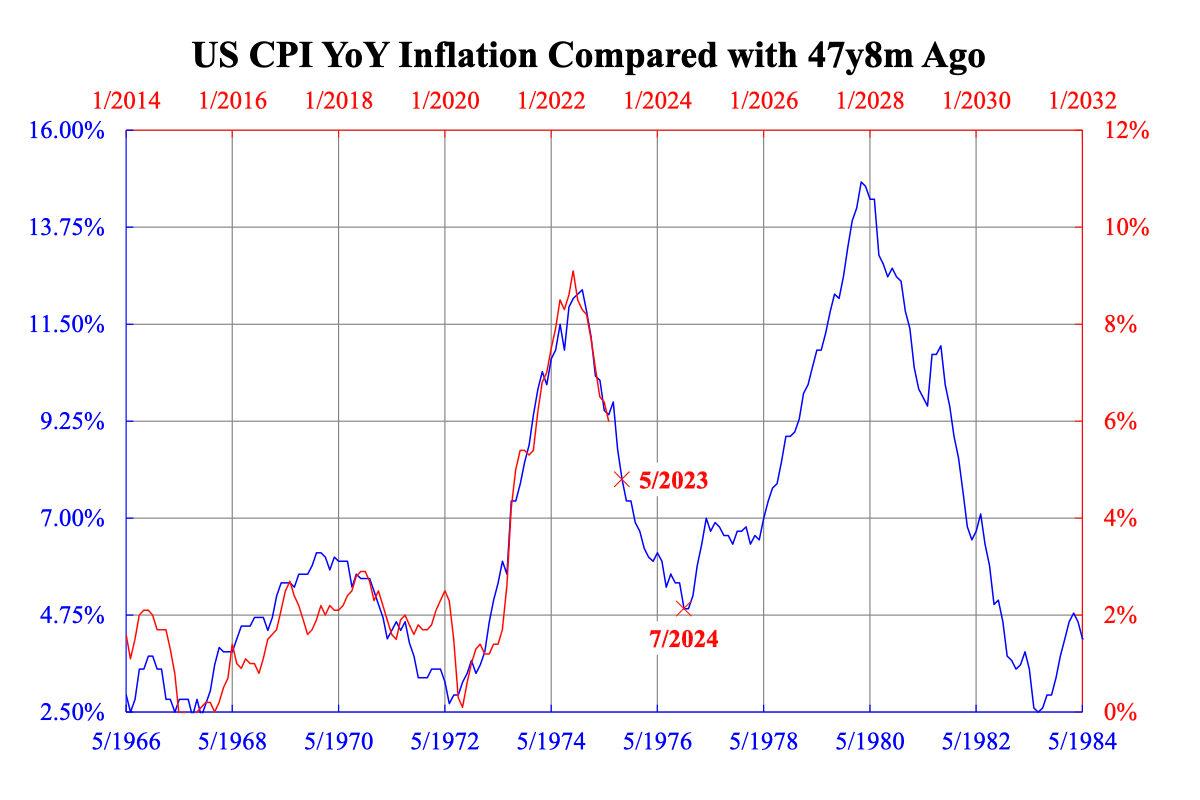

The latest strong jobs number supports this conjecture. Obviously, more tightening is called for. Based on the recent downtrend of inflation, a simple extrapolation exercise concludes that the inflation level will still be far above the Fed’s target of two percent after the next hike in three weeks’ time or even after one more hike in mid-June. Based on the comparison of inflation with 47–48 years ago (in the mid-1970s), the accompanying chart shows by the middle of this year, when the Fed can observe the data of 5/2023, overall CPI YoY inflation will still remain high at nearly five percent.

There can be two scenarios. If tightening is still not enough by June, the chance of further hikes to overdo will be high as there has already been a banking crisis. As long as the second round of the banking crisis has not yet arrived, the jobs market will remain strong, and inflation will resist falling. But if tightening is already enough, this means inflation will come down quickly as it did in the mid-1970s. However, this means a recession occurred at that time. Inflation is a lagger, paradoxically, its speedy downtrend will confirm that recession has already arrived.

In either case, a recession is inevitable, just a matter of sooner (enough tightening) or later (with further tightening). In this sense, how many more hikes are of less relevance given the almost certain recession outlook. Arguing forward, because the recession will drive down inflation, rate cuts will also be inevitable as inflation heads towards two percent under recession. This means the Fed will inevitably be cutting rates sharply, where interest rates staying high at the current level is a highly unlikely outcome. The long-tenor sovereign yields indeed priced this in some weeks ago.