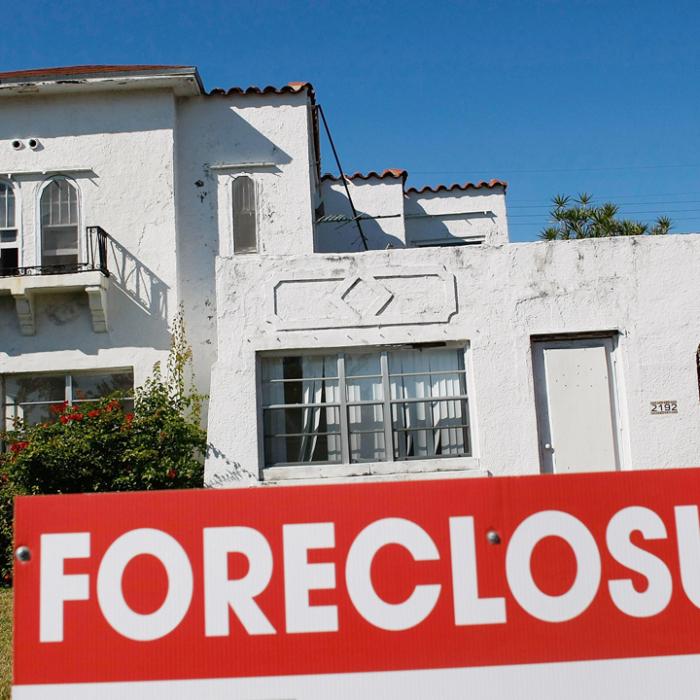

The Veterans Administration (VA) says it has helped 145,000 veterans stay in their homes over the past year and avoid foreclosures.

On the back of that success, the VA is doubling down and calling on mortgage companies to pause future foreclosures of VA-guaranteed loans through May 31, 2024.

However, some are skeptical about the VA’s long-term goal and have other concerns.

The moves came just days after a National Public Radio (NPR) article reported that thousands of VA loan borrowers risked losing their homes after the COVID forbearance program ran out.

“My impression whenever I see the VA get involved in interfering with markets in general is that I get a little bit nervous,” said attorney Benjamin Krause, a military veteran who assists veterans across the country with legal representation.

“The agency doesn’t have a history of doing this and when they get involved in the markets, it’s not a great thing for vets. The VA’s intent here is to buy mortgages in foreclosure, aiding those suffering from homelessness and challenges due to the COVID foreclosure moratorium,” he told The Epoch Times.

“No one wants veterans to lose their homes, including banks, but the solution of more VA interference in the existing markets is not the solution,” he added. “The VA should not be in the business of direct lending to veteran homeowners, and the agency lacks legal authority to do so.”

‘Taking on Too Much’

Mr. Krause says the last thing the VA should be involved in is the mortgage business.“So the VA is already paying for abortions and sex changes and to me, adding mortgages seems like they’re taking on too much. My concern is they had this program all ready to go 10 days after an NPR story that I call B.S. There’s something else going on.”

In that letter, the MBA requested that the VA provide a 30-day public process for review and comment on the VASP program, adding, “At this point in time, we are unable to support the VASP proposal without additional information to assess the borrower impact and the ability of servicers to deliver it without undue costs or risks (compliance and reputational).”

“I think this is the starting off point for something bigger,” Jason Ous, a military veteran who for over a decade handled foreclosures for a Midwest regional bank, told The Epoch Times.

“We need to be paying attention to how our government is spending resources and in this instance, these foreclosures are a product of the [COVID] forbearance the government enacted, which unintentionally created the problem to begin with.”

The program allows military borrowers to obtain a zero-interest, deferred-payment loan to cover missed payments and modify their existing VA loan to achieve affordable monthly payments for the duration of the extension.

‘No Meaningful Alternatives’

Some see the moves by the VA as a step in the right direction for veterans who need immediate mortgage assistance.“The foreclosure pause is badly needed as veteran borrowers have had no meaningful alternatives to foreclosure for over a year,” Steve Sharpe, senior attorney at the National Consumer Law Center, stated in its newsletter.

“We applaud VA and the Biden administration for taking necessary steps to protect veteran families, and we look forward to the release of VASP.”

But for Mr. Krause, the image of the VA becoming a direct mortgage lender is troublesome.

“Veterans should be wary of this proposal as they should’ve been wary of the foreclosure forbearance program in 2020,” he said.

“Veterans participated in a massive mortgage relief program that resulted in higher interest rates, lower home affordability, and now over 140,000 veterans unable to refinance their homes.”