The Federal Reserve has unleashed the steepest series of interest-rate increases in decades in a bid to tame soaring inflation—and policymakers warn more rate hikes may be in store.

While the Fed opted not to raise the benchmark federal funds rate at its most recent policy meeting in September, rates are at the highest level since 2001, within a range of 5.25–5.5 percent.

Even though the Fed changes only a single rate—the federal funds rate—this has a direct effect on the interest consumers pay on all manner of variable-rate loans.

Tens of millions of Americans with various types of debt have been impacted in various ways by the Fed’s interest rate increases.

Household Debt at Record High

According to the Federal Reserve Bank of New York’s quarterly household debt report, released in August, overall household debt ticked up by $16 billion in the second quarter, to a record high of $17.06 trillion.An analysis of the numbers by WalletHub showed that at the end of the second quarter, the average U.S. household (which owed a total of $143,762) is getting close to a projected breaking point for household finances.

“Based on our analysis of debt during the Great Recession, the average household is about $14,339 away from truly having to worry about defaulting,” Jill Gonzalez, WalletHub analyst, told The Epoch Times in an emailed statement.

Key question are how the Fed’s rate hikes have affected overall household ability to make debt-service payments and whether they have contributed to a rise in defaults.

According to the latest household debt service data, it seems consumers have been largely insulated from the worst the Fed has thrown at them.

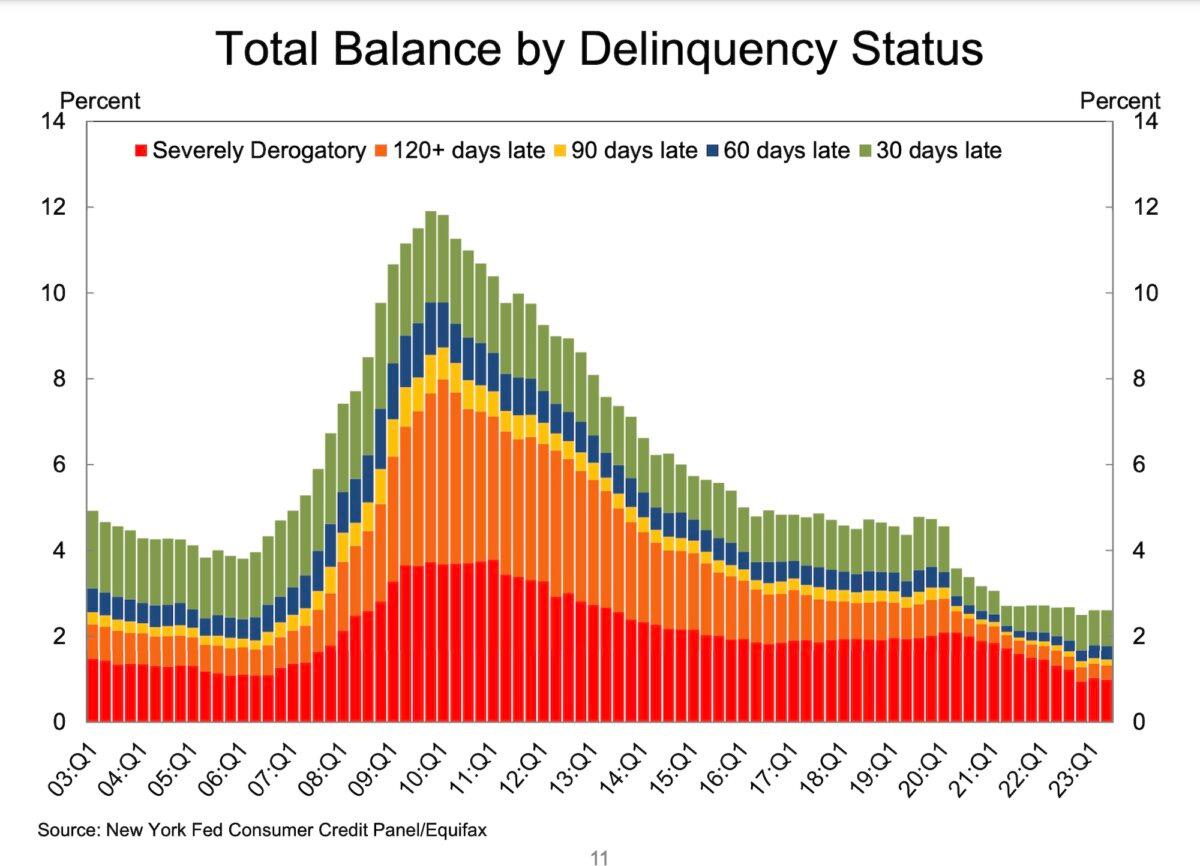

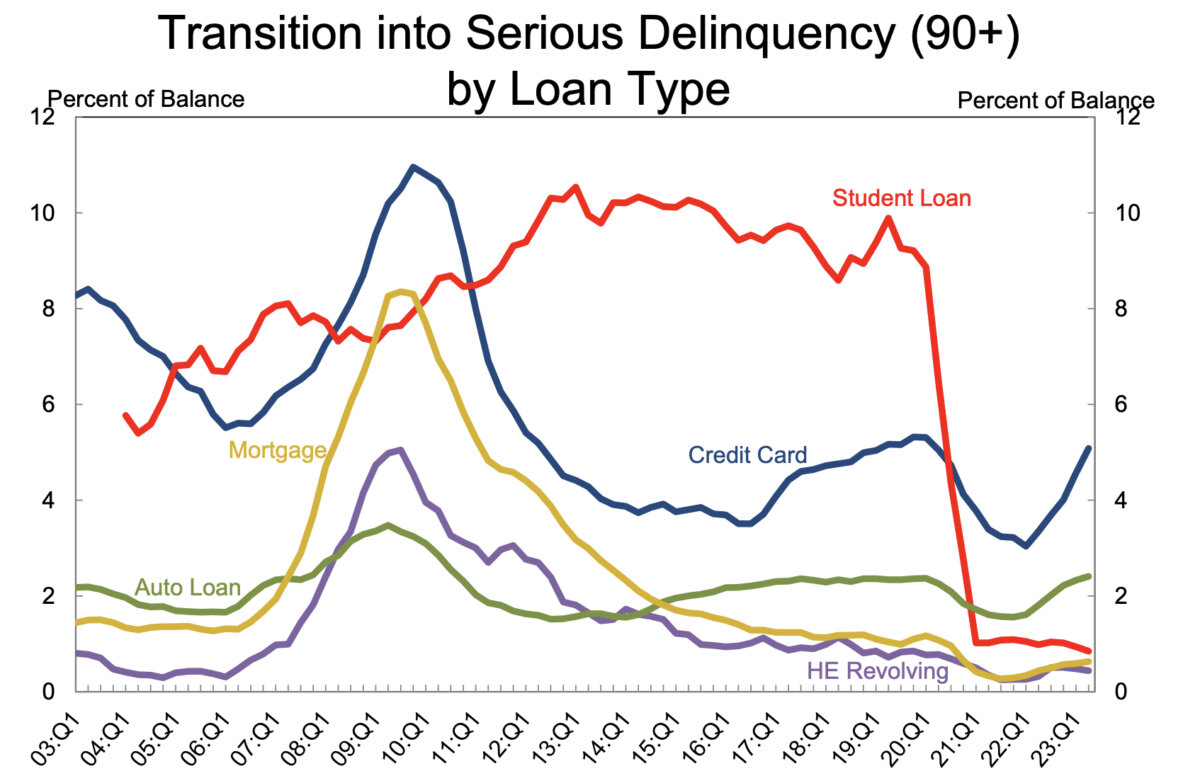

However, there’s been an increase in the percentage of all types of household loans that have fallen into serious delinquency—with the exception of student loan debt.

This suggests that, on paper, households have the means to make various loan payments but, perhaps due to economic uncertainty or squeezed by inflation, they’re starting to fall behind.

It’s a view expressed by former Walmart CEO Bill Simon, who told CNBC in an interview on Oct. 9 that a series of factors—political polarization, inflation, and high interest rates—were all working together to undermine consumers and their propensity to spend.

Ability of Households to Service Debt

As a percentage of disposable personal income, household debt-service payments were 9.8 percent in the second quarter of 2023.That’s roughly the same figure as in the first quarter—and down slightly from the prior quarter’s recent peak of around 10 percent.

And in the first quarter of 2022, when the Fed started its aggressive rate-hiking cycle, that figure similarly hovered around 9.8 percent. This suggests that the rate hikes have had little impact on the average household’s ability to make payments.

Part of the reason that this figure has held steady over the course of the Fed’s rate-hiking cycle (which began in March 2022) is that disposable income has risen during most of that period, although it recently plateaued and seems to be on the cusp of a downturn.

Both in nominal terms and in real (inflation-adjusted) terms, disposable income has mostly gone up since the Fed started hiking rates, offsetting some of the impact of the increases.

Most Household Debt Locked in at Lower Rates

According to Moody’s Analytics data provided to Business Insider, just 11.1 percent of household debt had a floating rate as of the first quarter of 2023.This means that only a small fraction of the total outstanding household debt was adjusted higher as market rates went up in line with the Fed’s rate hikes.

That figure was roughly twice as high several decades ago and it’s another piece of the puzzle helping explain why households appear to have been largely immune from the interest rate increases.

“U.S. households have been largely insulated from Fed rate hikes, as most consumer debt carries a fixed interest rate, the bulk of which is in mortgages,” Cristian deRitis, Moody’s deputy chief economist, told Business Insider this summer, when the analysis was carried out.

Existing borrowers with fixed-rate mortgages have not seen their monthly payments go up despite the Fed’s rate hikes, while most auto, student, and personal loans also carry fixed rates, providing a further buffer to households against rising interest rates.

Transition Into Delinquency

After declining sharply through the beginning of the pandemic, aggregate delinquency rates for all types of household debt were roughly flat in the second quarter of 2023 and remained relatively low.Roughly 2.7 percent of outstanding household debt was in some stage of delinquency as of June 2023, according to New York Fed data.

That’s approximately two percentage points lower than the last quarter of 2019, just before the COVID-19 outbreak hit the United States.

However, there was a rise in the percentage of all types of household debt except student loans that went into serious delinquency, defined as 90 days or more delinquent.

Serious delinquency transition rates on mortgage debt rose from 0.44 percent in the second quarter of 2022 to 0.63 percent in the second quarter of 2023.

Also, the percentage of home equity line of credit debt that went into serious delinquency over the same period went from 0.32 percent to 0.44 percent.

But the biggest jumps were auto loans and credit card debt. Serious delinquency transition rates on auto loans went from 1.81 percent to 2.41 percent.

Credit card debt delinquency transitions went from 3.35 percent to 5.08 percent—an 11-year high.

(Source: Federal Reserve Bank of New York)

Data compiled by Bloomberg shows that the biggest U.S. banks are poised to write off more bad loans in the third quarter than they have since the early days of the pandemic.

JPMorgan Chase, Citigroup, Wells Fargo, and Bank of America are jointly posting around $5.3 billion in combined third-quarter net charge-offs, which would mark the highest level of write-downs for the group since the second quarter of 2020.

A year earlier, when the Fed was relatively early in its rate-hiking cycle, that figure was less than half.

The credit card interest rate has increased to an average of 20.72 percent, according to Bankrate, which noted that it’s the highest figure since it started keeping track in September 1985.

By the same token, LendingTree’s data show that, as of late September, the credit card interest rate stand at 24.45 percent, an all-time high, according to records kept by the firm.

Federal Reserve data on commercial bank interest rates on credit card plans paints much the same picture, catapulting from around 15 percent in May 2022 (shortly after the Fed started raising rates) to 21.19 percent in August 2023.

A recent WalletHub found that the Fed’s interest-rate hikes thus far have increased the credit card debt burden by around $36 billion in extra interest charges over the next 12 months.