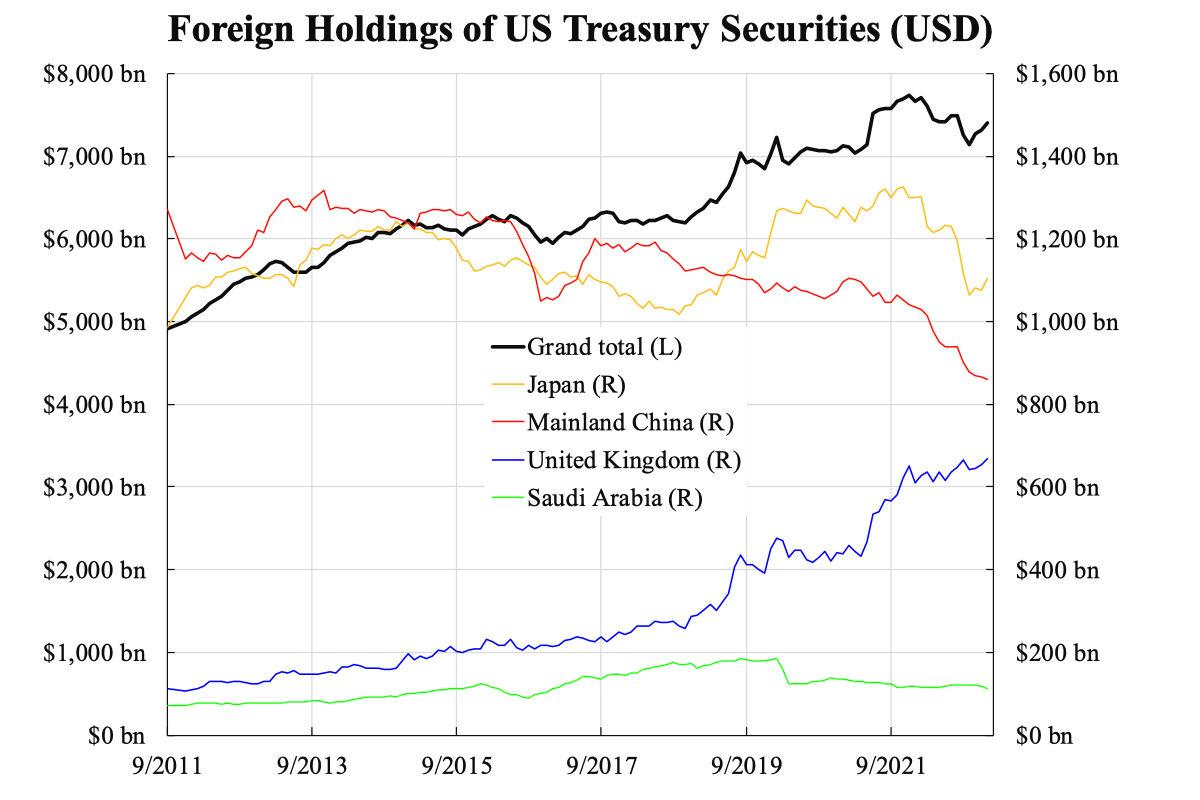

One of the recent news warnings about the status of the U.S. dollar was the continuing slash of U.S. Treasury securities holdings by mainland China. It’s latest holding in January was US$859.4 billion, a year-over-year drop of 17 percent compared with that of US$1,033.8 billion in January 2022. Seventeen percent is undoubtedly a significant decline compared to the overall total of 3.3 percent fall. Yet there are reasons justifying this: China exports fell by ten percent at the end of end-2022, with foreign sell-off of China sovereign bonds and other outflows, that 17 percent was explainable.

Regardless of the reasons behind it, did China’s reduction of U.S. Treasury securities impact the total amount? From the accompanying chart, one can see the answer is a crystal clear “No.” Since 2014, not long after Xi became the leader, China has been underweighting U.S. Treasury securities. But an interesting observation is that such a downtrend is linear in most of the early years and then declines more quickly since 2021. To those familiar with China’s data, this is precisely the trend of GDP growth so the story can go without conspiracy.

There has always been a story about China’s underweighting in U.S. dollars. But think carefully about it; what else is there to switch to? The euro is already undertaking a similar campaign as the dollar. Gold is unlikely, as there is probably not much gold for China to buy. Anyone who thinks twice would realize that China cannot easily diversify its reserve holdings. We might not have to complicate things but accept that China is earning less forex and having more outflows, so it is reducing its U.S. Treasury securities to compensate.

U.S. Treasury securities’ total foreign holdings have increased over the past decade. The actual reason is inflation. All central banks have been printing money aggressively in the quantitative easing era, the United States is no exception. It is natural to see the absolute amount of money (treasury holdings) increasing over time. The visually linear uptrend of the total suggests it is likely no structural change to the attractiveness of treasury securities; otherwise, we should have observed a turnaround.

It is interesting to see the breakdown. While China, the second largest holder, has been holding less, others are not. The largest holder, Japan, has been holding a stable amount for over a decade. Most other European countries, including the UK, the third largest holder, have been overweighting. The holding remains flat even for countries that China is getting close to, like Saudi Arabia. Simple counting shows the proportions of countries overweighting and underweighting U.S. Treasury securities over the past year (from January 2022 to January 2023 are roughly equal.

The overall trend seems related less to yield and more to the strength of the dollar. The 10-year securities yield declined between 2009 and 2019, then increased from 2020 to now. The dollar index rose from its lowest point of 70+ in 2009 to over 100 in recent years.