The Federal Reserve has painted itself into a corner with its fight against inflation, and some experts say it now has no coherent plan for how to get out of that predicament.

William McChesney Martin, Fed chair from 1951 to 1970, famously said that the role of the Fed was “to take away the punch bowl just as the party gets going,” in other words, to cool the economy by raising rates before it begins to overheat. To follow that analogy, however, current Fed Chair Jerome Powell is now attempting to kill the party well past the morning after.

“They have wasted long periods of time to correctly detox,” economist Arthur Laffer told The Epoch Times. Laffer believes that more bank failures are likely on the horizon, which is making Powell think twice about raising rates further, but “there will be a lot more collapsing if they don’t do it.”

‘The Party Is Over’

Economist Nouriel Roubini, renowned for predicting the 2008 mortgage crisis, said in a Frontline interview—which is no longer available—that “we have had literally a few decades of ever-increasing bubbles that have been fed and supported by central banks ... that have been fed by excessive leverage, excessive private and public borrowing, and excessive risk-taking. The party is over.”“This dream in a bubble is bursting and is turning into an economic and financial nightmare.”

Inflation Fighting and Bank Failures

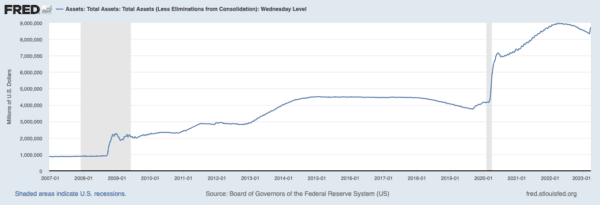

Former Treasury Secretary Larry Summers highlighted the precarious balance of fighting inflation and shoring up struggling banks.Even as it continues to increase interest rates, however, the Fed has simultaneously reversed a policy, known as “quantitative tightening,” of steadily selling off the massive holdings of bonds it has been buying since 2008, which is now returning toward its peak level of nearly $9 trillion. This shift would likely fuel inflation by pushing longer-term interest rates down.

Powell pursued his quantitative tightening strategy “only until the first scream,” Laffer said. “And he got the first scream with less than half a trillion sold. I think the height it got to was $8.8 trillion, and now it’s down to $8.6 trillion.

“That 200 billion caused squeals beyond belief, bankruptcies, runs on banks, all that.

“We have not even scratched the surface of where we should go.”

Today, he said, “safety is not in long-term Treasurys. ... If average inflation were to be, say 5 percent, 10-year Treasurys eventually would have to be 7 percent; today they are 3.5.” Because of rising rates, the value of fixed-rate bonds fell in 2022, causing huge losses for banks that held them.

Trial-and-Error Monetary Policy

The Fed today is in uncharted territory, and some say the central bank lacks a coherent plan of how to get the United States’ economy back on sound footing, opting instead for a trial-and-error approach of making adjustments and seeing what happens.“These people don’t understand what they’re doing,” Laffer said. “Jerome Powell is not an accomplished theoretician on money and banking. He doesn’t have much experience in it, either. And yet he’s facing one of the most serious decision-making situations ever.

“He doesn’t have the requisite tools to be able to make the right decisions. And I don’t just mean him, but the whole board.”

When the policy of quantitative easing started in 2008, buying trillions of dollars of bonds was an experimental effort that was attempted because the Fed had already driven short-term rates to zero and couldn’t bring them down further. At the time, Fed officials acknowledged they weren’t sure whether, or how, it would work.

“The problem with [quantitative easing] is it works in practice, but it doesn’t work in theory," Then-Fed Chairman Ben Bernanke said. Now that they are attempting to reverse it, they still aren’t sure.

Banks Losing the Public’s Trust

While inflation remains a chronic problem, bank regulators must now also cope with depositors’ faltering trust in the banking system. Because banks invest a substantial amount of their deposits in longer-term assets, such as loans or bonds, the banking system can’t survive too many simultaneous demands by depositors for their money. For this reason, maintaining the public’s trust that their deposits are safe and as good as cash is essential to avoiding bank panics that could lead to systemic collapse.“Once you start a run,” Laffer said, “it’s a different game.” For that reason, he supports the decision by bank regulators to guarantee all depositors, during tense weekend meetings following SVB’s failure.

“That Sunday night, I think [Treasury Secretary Janet] Yellen was correct,” Laffer said. “Given that this thing was going to explode on Monday morning, if they didn’t guarantee the depositors, the run would be on, and there is no limit to how far that run goes.

“The only way to stop a run on the banks is to have a guarantee of depositors on the spot. And you can’t wait a week, because it’s gone, it’s over in a week.”

Going forward, however, the goal should be “to ameliorate the short-run financial collapse but allow the incentive structure to be correct,” Laffer said. “All investors in the banks, whether they be bondholders or stockholders, should suffer the entire consequences of the losses, period.”

Guaranteeing all bank deposits, however, creates the risk that depositors will simply go where they can get the highest interest rates, without having concern for how risky the bank may be or how concentrated their savings are within any one institution. As a result of SVB, Signature Bank, and others whose depositors were bailed out, everyone with a bank account will now contribute, through higher deposit insurance premiums, to repay companies and wealthy individuals who lost more than $250,000.

Fed on Its Own in Inflation Fight

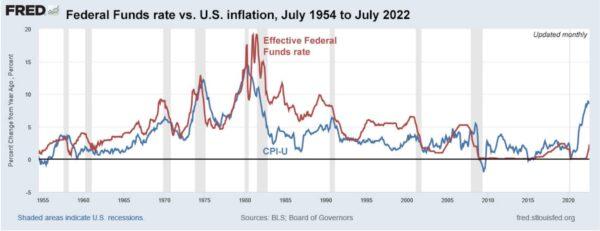

One problem that the Fed has in attempting to quell inflation is that it’s on its own in this fight. In the 1980s, when then-Fed Chairman Paul Volcker pushed rates up to almost 20 percent to bring down double-digit inflation, he was doing so at a time when President Ronald Reagan was cutting taxes and deregulating the economy, thus boosting the supply of goods and services. Inflation was reduced in short order by simultaneously reducing demand and increasing supply, bringing the economy back into balance.The only tool the Fed has to fight inflation, working by itself, is crushing demand through higher interest rates.

If rates are pushed high enough, there will be lower inflation, Laffer said.

“But we’ll get lower inflation with a lot lower output, employment, production—and a lot more despair and hardship.”

A supply-side approach of reducing taxes and regulation, by contrast, will “increase the supply of goods and shift the supply curve out rather than the demand curve back,” he said. “You choose which model you prefer.”