The latest released U.S. inflation was expected to slow down. The rationale behind such a bet by the economists might be the high base of a year ago: March 2021 was at 2.6 percent, and April 2021 was 4.2 percent. If only in this sense, a slower number for last month may not mean price pressure truly eased but simply an arithmetic illusion. Many having wishful thinking would regard inflation as transitory and peak out soon. One reason for having that view was too much reliance on the experience of recent decades where inflation was always contained automatically.

Another main argument that inflation would peak out early or automatically (in a sense without much monetary tightening) is based on the supply-side argument. That says that lockdowns under COVID-19 which cause supply reduction (i.e., logistic blockage) are the true cause. This has been indeed the case two to three quarters ago. However, lockdowns are now already in the past, except in China. Indicators like the Baltic Dry Index which measures the cost of transporting key materials by sea have come down by over half from the peak, suggesting the supply-side argument cannot explain recent inflation.

On the other hand, exceptional monetary boosting over the past two years did create a lot of real effects, indicating that the Federal Reserve might have judged wrongly by referencing too much the experience of 2008. In the aftermath of the financial tsunami, credit was still weak after a prolonged period of zero interest rates and rounds of quantitative easing. This was because of lockdowns in the housing market and banking sector which generated a huge negative demand shock. But this time is different as Carmen and Rogoff termed: COVID-19 was not really a demand shock.

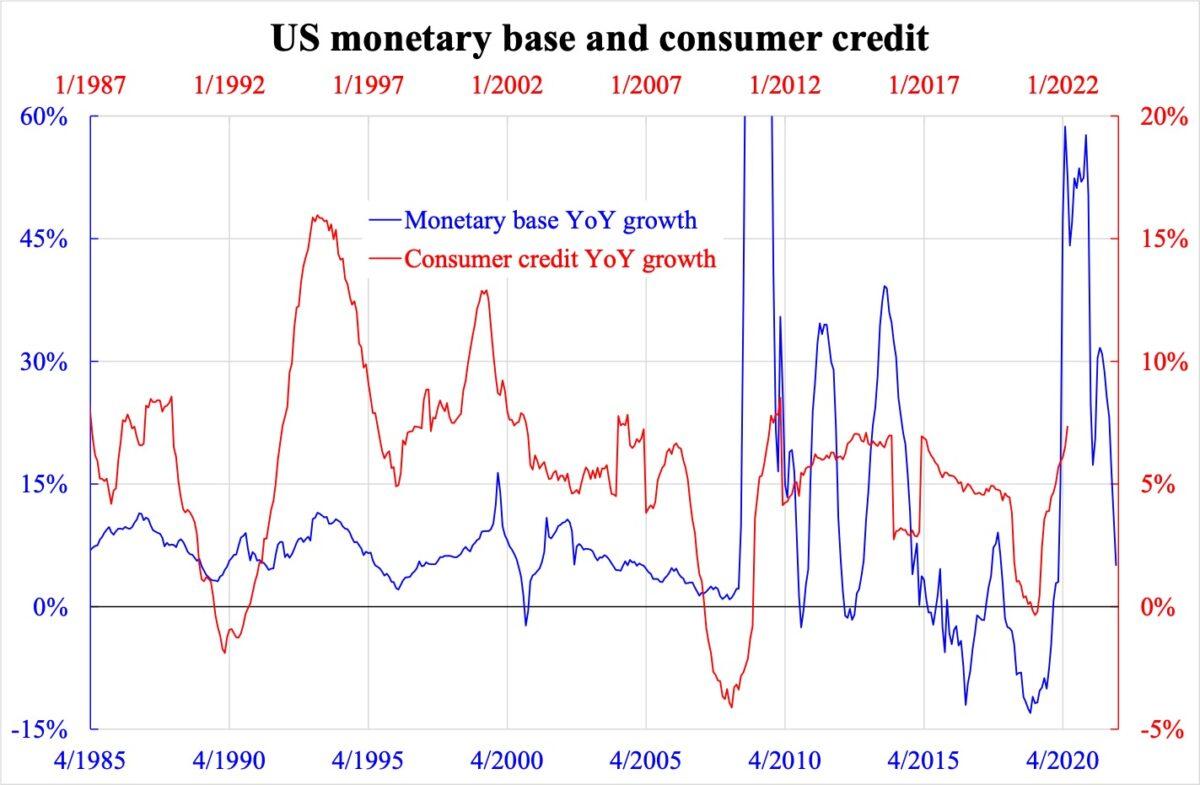

The red line in the accompanying chart shows the consumer credit year-on-year growth. Around the year 2008, the credit crunch was deep and prolonged, but in 2020 it was mild. As the key sectors of housing and banking were both in good shape, lockdowns were obviously a supply shock that would not be responsive to monetary stimulus.

Can printing money resolve any shortage of necessities? But the Fed was doing something like 2008. The ridiculous surge in the monetary base suggests the Fed has been crazy for some time.

Based on the correlation of these two series shown in the chart, monetary base growth is found to lead consumer credit growth by about seven quarters. The recent strong pickup of the latter is vivid evidence of the delayed boosting effect made seven quarters ago. Since the absurdly high monetary base growth is expected to be maintained for over 1.5 years before it comes down meaningfully, the same should be expected for consumer credit growth in a lagged manner. As a result, demand-driven inflation will follow accordingly.

While Jay Powell the Fed chairman has ample tools to tackle inflation, the honest answer is only one tool is applicable: to remove excess money by either hiking the Fed funds rate or selling bonds (quantitative tightening). And the effect of doing so will happen later rather than immediately.