The year 2023 seems a turnaround year for the world economy: Not only in the real estate sector, where prices are on the rebound. Indeed, inflation and the interest rate hike will still be the focus, at least for the first half of 2023; recession, if any, should be later. The picture is getting clearer: inflationary pressure stems mainly from the strong labour and spending markets. Nevertheless, it is unclear whether the current policy stance is restrictive enough to bring inflation down meaningfully. The actual reason behind this is the monetary policy is very slow in transmission.

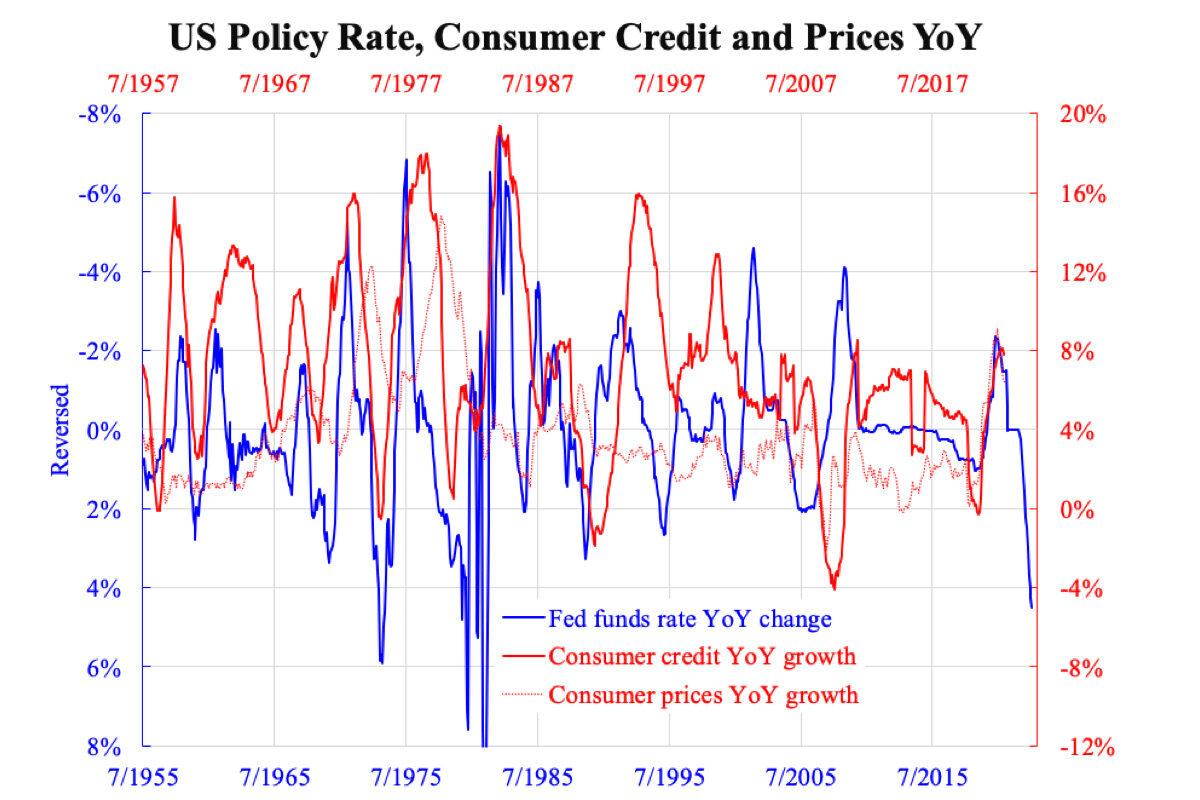

In principle, interest rate hike targets mostly credit, which, as the logic goes, drives inflation. Using the entire historical time series of Federal funds rate and consumer credit from the Federal Reserve, the accompanying chart shows that the year-over-year change of fund rates leads year-over-year percentage change of consumer credit by two years (compare the horizontal time axes). Theoretically, the price of lending (or cost of borrowing) instantly affects lending (or borrowing). But it affects only the new loans while all other outstanding ones are unaffected.

This is easiest seen in the mortgage market, where only newly made agreements would apply. It takes time for loans to mature, roll over, and produce an effect. Since the tenor of lending is usually longer than that of deposits (the intrinsic nature of banks to earn interest margin), it is easier to see broad money (M2, which mainly comprises deposits) slow down first before credit. Why the time lag is two years depends heavily on the effective tenor of lending, which is mainly empirical. It can vary, but two years seem to apply nowadays.

Because of this, central banks targeting inflation need to act at least two years before inflation arises, and this is why most of them project inflation to 2-3 years ahead. However, whether they know what to do is one thing, but whether they can do it is another. This round of central banks (not confined to the Fed) acted not ahead but at least one year after inflation had accelerated. Although they have been catching up quickly in the last few months, they tend to stop before inflation is certified dead. This is one of the significant risks.

Another risk, as can be identified from the chart, is that the effect of rate hikes on credit is not so certain. With a two-year time lag, consumer credit growth was projected to decline sharply by now, but it hasn’t. The relationship between the two has become less clear over the past few decades. Yet another uncertainty the time series shows is the relationship between credit and prices. Far more factors govern aggregate price than are discussed here. Some of the mechanisms are not well known.

The speedier the rate hike, the more likely the risk of being overdone. Never downplay the possibility and severity of recession ahead, if any.