Back in 1912, before most countries had a central bank, economist Ludwig von Mises wrote that such institutions are inadvisable. Among myriad problems, they provide a moral hazard to politicians. All office holders like to have lower interest rates because it makes them popular and seems to bolster economic growth. Therefore, the central bank will face constant political pressure to reduce rates and fuel inflation.

“When governments do not think it necessary to accommodate their expenditure to their revenue and arrogate to themselves the right of making up the deficit by issuing notes,” he wrote, “their ideology is merely a disguised absolutism.”

How do lower interest rates feed inflation? The central bank has a great deal of influence over short-term rates, the effects of which are impactful on the entire yield curve. Money becomes cheaper and more easily acquired via leverage. That means that banks are granted the opportunity to expand credit and money on the street. More money in circulation reduces the purchasing power of all existing notes.

That’s not the only problem. Lower rates, when they are artificially imposed—instead of flowing from growing savings—drive investment in ways that are unsustainable. This typically affects the capital goods industries the most. These are the industries that make goods that make other goods, things not for final sale but rather intermediate goods. They boom until they bust. That’s how artificially low rates generate economic instability.

The Fed has been remarkably accommodating to political priorities for the better part of a century. It became so with the Great War soon after the Fed’s creation. It is unlikely that the United States ever would have entered that bloody and destructive European conflict without a printing press ready at hand. The result was, of course, the first of many devastating inflations.

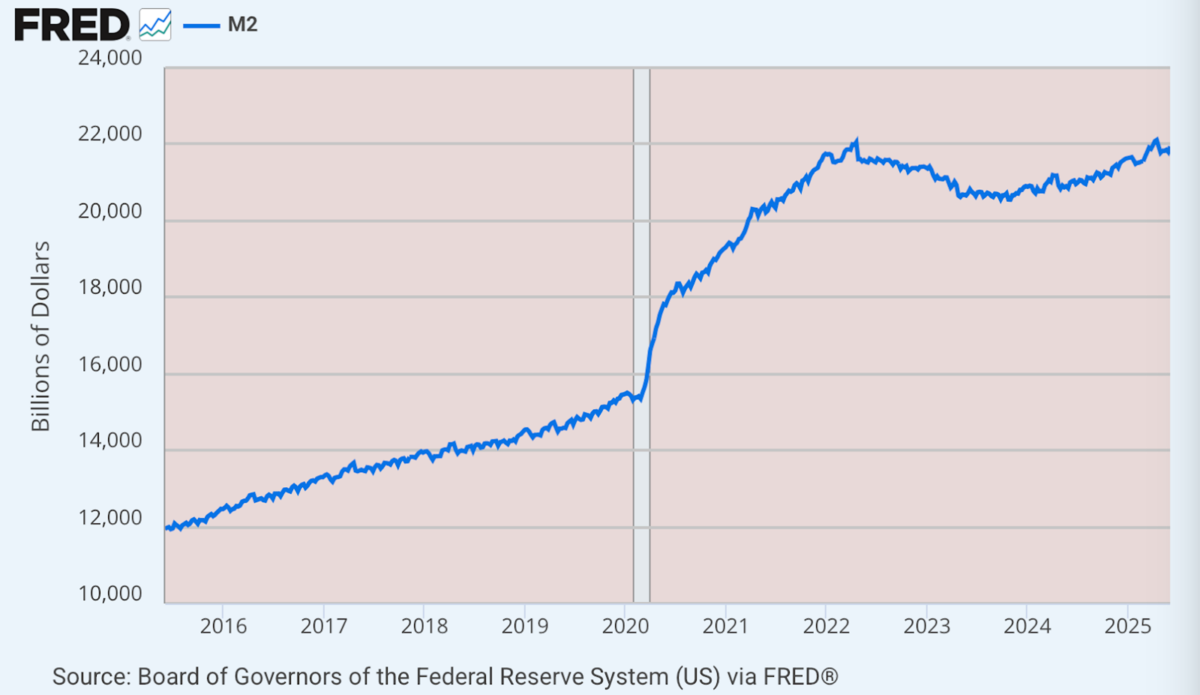

So it was when the COVID crisis broke out. The Fed had been attempting to fix up its balance sheet and raise rates, but the progress was interrupted by a virus from China. The Fed again drove rates to zero and kept them there. The result was a flood of money with no precedent.

That led to a four-year loss in purchasing power of 25 percent and probably far more in many sectors. You can hardly buy anything in this country anymore without being shocked at the prices. Many prices are still increasing to catch up for lost time. Overall, inflation is dying down but certainly not gone.

We might ask the salient question why the inflation of the past four years wasn’t worse than it was. My answer is the obvious one but rarely mentioned. It has to do with U.S. trade relationships around the world. Trade deficits mean goods in and dollars out. In other words, we sent a vast amount of the new money out of the country so that it could not affect domestic inflation.

It’s strange to say as much, as everyone is down on globalism these days, but it was international trade that spared us a more devastating hyperinflation. Instead, we simply exported the monetary splurge to other countries while importing goods made with lower-cost labor and resources.

President Donald Trump is obviously focused on changing U.S. trade relationships with the world. It certainly means a likely reduction in the trade deficit but also means that, in the future, money is likely to stay circulating domestically more so than it otherwise would.

What does that mean for inflation? It means that small changes in the money stock are likely to rev up prices more than they would have in the past. In other words, it could be that a second wave of inflation is more likely with a renewed push for lower interest rates.

Trump is a businessman. He likes lower interest rates. He is also aware that high interest rates are costing the U.S. taxpayer a bundle in terms of debt service. It seems like pure waste. His solution is to demand that the Fed lower rates. That would reduce the cost of debt service, spur economic growth, and inspire more borrowing and investment. This is why he is demanding a cut of 300 basis points, which is essentially unthinkable. It cannot be done without a massive bond-buying campaign by the Fed, which amounts to money printing.

The trouble is that this could unleash another round of inflation that the Fed just completed killing off with the largest and fastest increases in interest rates in U.S. history. As terrible as the Fed was between 2020 and 2023, it has managed the decline in inflationary pressure rather well. It’s all happened because the higher rates have sponged up the remaining excess of money. Today, the money stock sits about where it was three years ago.

Because of this policy, our purchasing power is harmed less than it otherwise would be. With Trump’s new trade policies, there is a real danger in suddenly lowering rates. As good as that might seem politically, it presents genuine dangers of renewed inflation next year and the year after that.

For that reason, the Fed is correct to resist the political pressure to lower rates. That decision could cost the Fed chairman his job, however. As much as I would welcome more oversight for the Fed—can we finally get an audit of this money machine?—this kind of pressure could pose genuine dangers for the American standard of living.

Despite predictions to the contrary, I’m not expecting the dollar’s status as the international reserve currency to change anytime soon. That means continued international demand for dollars as a safe-haven asset and a favored tool of settlement for most of world trade. That protects the dollar from dramatic purchasing power reductions domestically so long as this remains true.

That said, a reduction in dependence on global trade put upward pressure on prices. Adding to that pressure, import taxes can push up prices too. We haven’t seen the evidence yet, but it will surely emerge in time.

Lower inflation is finally here. Let’s just count this as a victory. It’s too dangerous to be demanding lower rates right now. We need a much longer period in which they are high, as they are today. In any case, in real terms, they are not that high. They might be right where the free market for lending wants them to be.

The Trump administration should leave well enough alone and focus more attention on financial accountability from the central bank. And here’s an idea: How about a good old-fashioned audit of the gold supposedly held at Fort Knox, as they promised during the campaign? That’s a much better use of political capital than pushing for looser credit.