Argentina’s new president announced a shock therapy. The first eye-catching change was to devalue the official peso exchange rate by 54 percent. While the official ARS to U.S. Dollar rate changed from 366 to 800, the black-market rate was still much weaker at about 1,000. This means such an act could only make the official price less fake compared to the true market price, and was a concession under market pressure. Such an act is also not meaningful for those who are using U.S. Dollars instead of ARS. Inferentially, who would still use a currency that depreciates speedily? Such an act is, by and large, futile.

Currencies devalued actively by the central bank versus those depreciated under market forces are entirely different. The former is a beggar-thy-neighbor policy such as the one practiced by the Bank of Japan, which tries to restore the competitiveness of a country by lowering the aggregate price level abroad. The feasibility of such an act rides heavily on the fact that exchange rate misalignment is not serious and that depreciation can be done in an orderly manner. In some cases, there could be no misalignment at all where a depreciation is an intended policy consequence.

The latter type is entirely different. It is the macroeconomic fundamentals that are so bad that misalignment is already significant, or fundamentals are deteriorating so quickly that rapid depreciation pressure arises. In either case, there is usually a strong tendency for the central bank to defend the exchange rate at the onset. However, such war is usually undertaken via foreign exchange intervention, where the central bank conducts direct purchases of the local currency. However, this requires an unknown amount of foreign exchange reserves, typically either U.S. Dollars or gold.

Macro fundamentals normally refer to two types: one at the governmental level and the other at the national level. On the governmental level, fiscal balance, which is periodic revenue less expenditure, measures the flow, while governmental reserves less debt measures the stock. On a national level, the current account balance, which is periodic net exports, measures the flow, while the country’s net assets are less easy to measure. All these indicators are often presented in percentage of GDP, which is the final variable that governs all other healthiness variables.

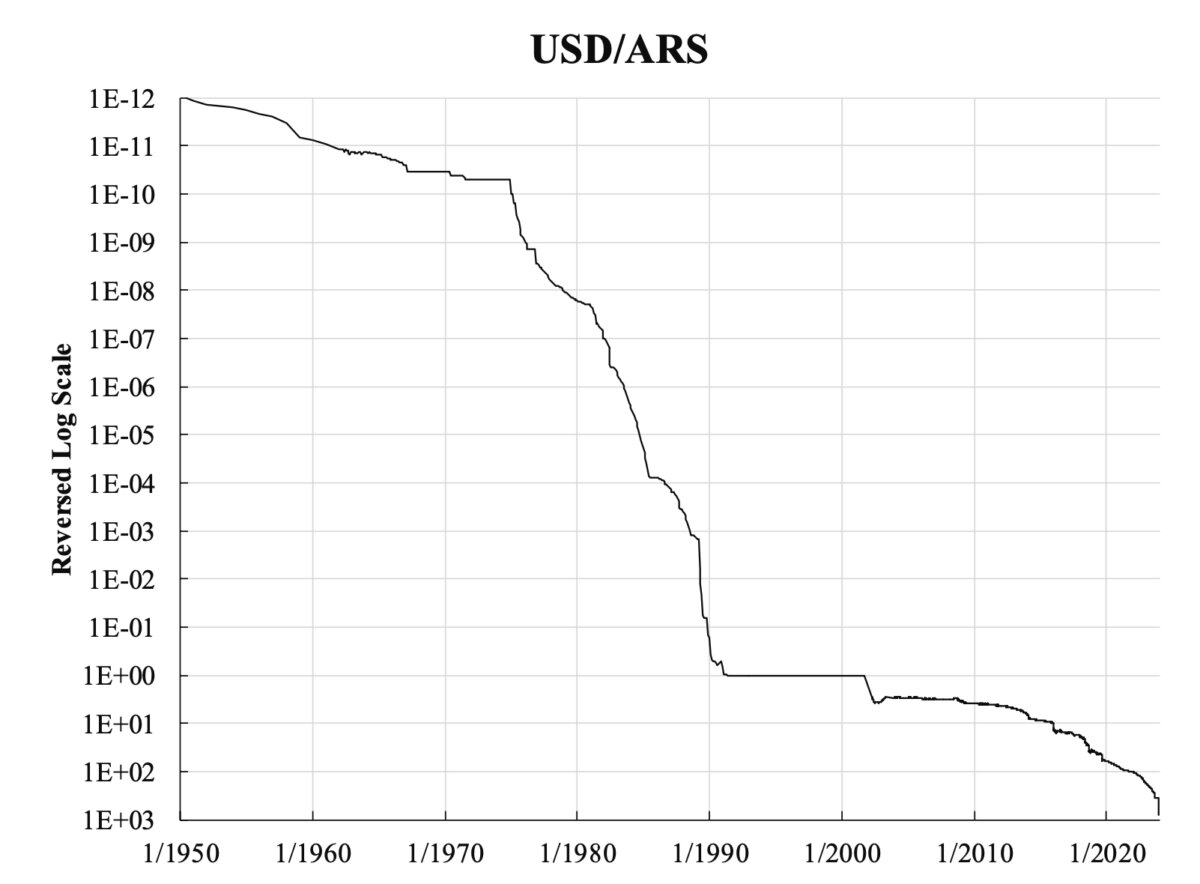

Clearly, Argentina didn’t do well in all these indicators. However, how bad each of these indicators, the resulting crisis, is unknown, which is just like how bad a habit can be, its fatality effect is unknown. However, a persistent deterioration of fundamentals would bring persistent depreciation pressure. As the attached chart shows, peso devaluation has been a problem since the era of WWII. A sharp depreciation is certainly not a solution. Although tightening is a natural way out, it is easier said than done. Citizens’ cooperation is never easy.

By definition, more savings means less consumption and, hence, lower prosperity, but this, in turn, means less savings. Now there is no practical prescription to get out of this vicious circle.

KC Law, Ka Chung