Since the beginning of 2024, the focus on China has switched to the stock market, given the debt defaults and housing market crash. The economic data look too good to be true: it is hard to reconcile a picture with 5.2 percent GDP growth and double-digit unemployment plus a series of debt defaults. The market was obviously not fazed by this kind of artificial data or false news. What’s more, the government openly banned the sales of stocks, which never happens in even much lower tiers of emerging markets nowadays. With all these, the degree of severity is clear.

The recent slump seemed due more to capital fleeing than anything macro or fundamental. The macro figures on paper were no worse than those in COVID-19 times. To quote a trustworthy market-compiled number, the PMI has stayed around 50 recently. Though not good, it was much lower at about 40 in the COVID-19 period. Similar improvement was found in the export sector, where the numbers could hardly be too fake (as its trade partners have the corresponding records). However, the Shanghai stock index is now almost as bad as it was during the COVID-19 period in the spring of 2020.

Why did the capital flee from China? Its political tension with the rest of the world could be a reason but might not be the main one. Such tension has been there since the trade war with the U.S. early in 2018. Although the Shanghai Composite Index had slumped one-third in 2018, it recovered in 2020. Almost all emerging markets are by construction, full of various risks, but this does not constitute a barrier to the flooding of the western market. A cyclical bust is not a reason for a thorough exodus because there must be some long-term funds to buy at the market nadir.

Thus, such an outward flow must be due to some structural or institutional changes. By structural, this means China is no longer having population growth (but decline), is no longer a world factory producing massively, is no longer enjoying long-term real estate bubbling (but deleveraging), and therefore is no longer having high economic growth. These structural macroeconomic changes result in not only a secular bear stock market (long-term stagnant index, as exhibited from 2007) but probably a new secular downtrend (probably from 2021 onwards, but yet to be confirmed).

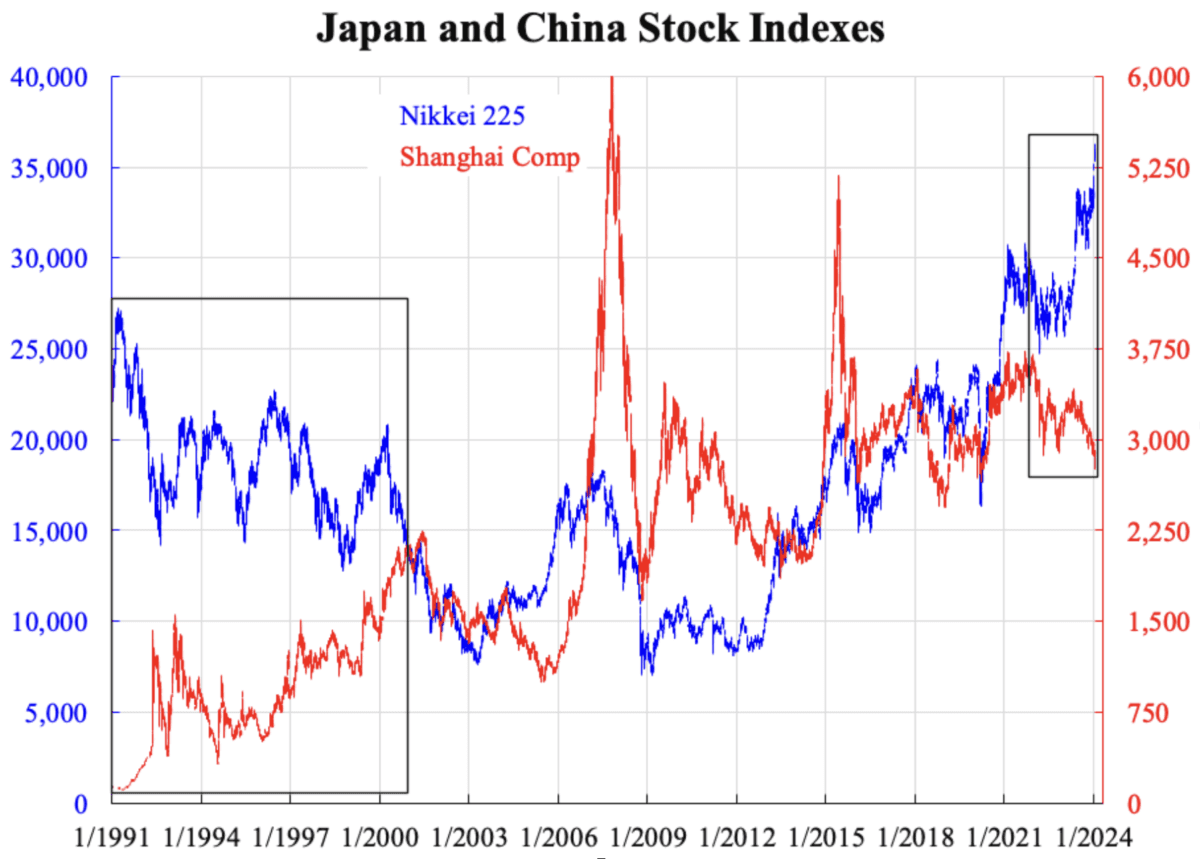

Japan is one of the few examples showing this. In the accompanying chart, we can see a good co-movement of the Japan and China stock indexes in the two decades from 2001 to 2021. Prior to that was an “Asia ex-Japan” period, as labeled by the financial market, where Japan’s declined while China’s rose. Now is the opposite, “Asia ex-China, and China,” where the two have reversed.

Apart from the structural reason, the institutional one is lacking in Japan. In order to sustain a one-man ruling regime, China is experiencing severe infighting where the whole of capitalism might be overturned. To Xi, the vanishing of the capital (rich) class is essential for the CCP. The market has felt this institutional change strongly, which explains why capital has fled massively without returning.