It’s impossible not to be amazed by the sudden boom in the price of precious metals, gold and silver in particular. I had been predicting some price moves above $40 but not $110. And for gold to break $5,000 per ounce was on no one’s radar.

Silver has experienced a one-year price run of 279 percent, while gold is up by 84 percent. It’s absolutely beyond belief and cries out for explanation.

These price moves are enough to cause The Wall Street Journal to announce: “The Golden Age Arrives, if Not as Planned.”

The reason for all this action? The speculations concern new industrial demand, a sudden end to price manipulation by the Fed, demand from central banks around the world, and plain-old flights to safety. The last two are the ones that intrigue me the most.

There are three factors causing the rise in demand on the part of foreign and domestic banks. The United States has stepped away from the globalist ideology it had preached and the institutions it had been building since 1948. Since 1973, under the Smithsonian Accords, the dollar has been the world-reserve currency, trusted by everyone as the building block of global trading relationships.

This agreement lasted for 50 years, but it was built on an unquestioned premise that the United States would accept global responsibilities as a neutral handmaiden of world commerce. The intellectuals would be in charge, and the United States would give up its self-interest on behalf of global economic growth.

That was the idea, in any case. The trouble could have been easily predicted by anyone well-schooled in monetary and trade economics. One unbearably obvious issue concerns the loss of grounding and throttles for U.S. monetary policy. With a printing press running full steam for decades, Americans would lose purchasing power both gradually and then all at once. The 1973 dollar has retained only 13.7 percent of its value. This is a disaster for a country that rose to prosperity and prominence in an age of sound money.

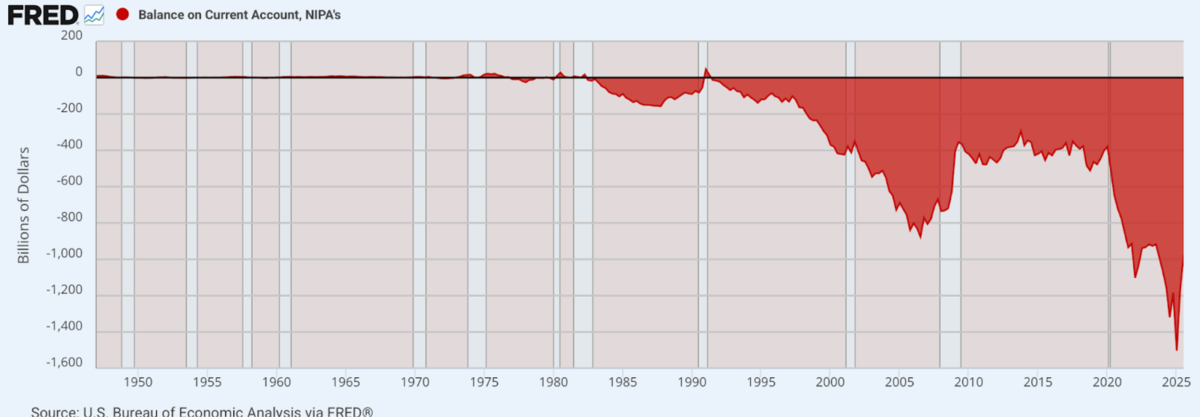

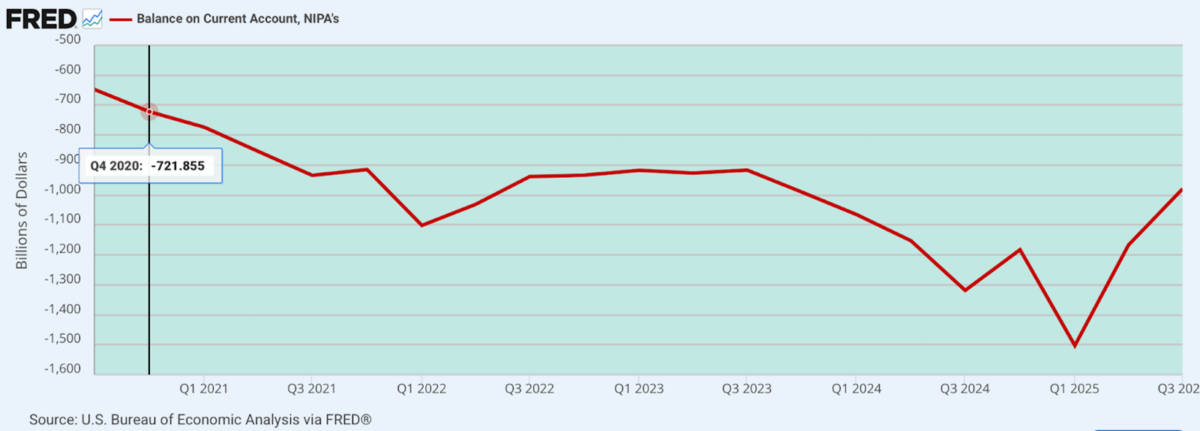

There are other implications of the system for trade. Such a system would create permanent wage and cost imbalances such that production would gradually become more advantageous for nearly every country in the world, and the United States would simultaneously become a net importer.

Nothing like this would have happened in a 19th-century-style gold standard, in which trade settlement was baked into the system. After 1973, however, the demand for dollars would be practically without limit all around the world, thus yielding ever-worsening trade deficits.

This is not money that other governments somehow owe the United States. This is just a measure of outgoing dollars relative to incoming by virtue of the exports of goods. Obviously, the role of the United States as a manufacturer has dramatically changed, despite its long history of being an exporting nation. This has fundamentally disrupted economic life in the country.

President Donald Trump is not a master of international economics, but he intuited a major problem and was determined to find a fix. He found his answer in the tariff, speculating that he could impose such taxes as a proxy for normal currency settlements that happened under Bretton Woods. Whether that theory works out in reality remains to be seen, but there is no question that the changes he has enacted have dramatically reversed the position of the United States vis-a-vis world trade.

These changes have amounted to a genuine shock to trading partners, national leaders, and central banks. They have responded with an obvious logic. If the dollar is no longer a neutral arbiter and will be deployed in the economic interest of the United States, what is the next-best thing? Where is the trajectory headed?

There is an obvious answer in gold and silver, which have been the foundation of monetary economics for all recorded history. Six thousand years is a long precedent, and the assumption is that in a world of tremendous uncertainty and upheaval, gold and silver are the best bet for what will be the future of monetary economics.

On Sept. 20, 2022, The Wall Street Journal announced that gold has lost its status as a haven. That turned out to be unbearably wrong. Nor did Bitcoin serve as a replacement, contrary to predictions at the time. Indeed, Bitcoin has been in a bear market during these exact times when gold and silver have been on a bull run more ferocious than anything we’ve seen in 50 years.

In an age of fiat everything, it’s utterly remarkable that the world’s smartest money is defaulting back to find and hold what is real. That means more mining, more prospecting, more digging, more shipping, and more safekeeping in huge vaults. It’s like the 1890s all over again.

What we are seeing right now is huge investors moving vast sums to physically stored precious metals while pouring the balance into mining stocks, even as health-insurance stocks and internet stocks are taking a beating. For those who love market fundamentals and time-tested truths, these are glorious days.

What of the speculation that Trump’s attack on the Fed has involved backroom prodding to end the price fixing and manipulation of the gold and silver price? I cannot confirm these rumors. If they are true, what we are seeing now is less of a sudden bull market and more of a catch-up rally to what should have been the price all along.

Does this mean a genuine return to the gold standard? That would be the best answer, but the vast liabilities on a global scale make that unlikely for now. Debt is the driver of the global economy, and it won’t be paid back, at least not in current dollar valuations. A more likely scenario is another wave or two of dollar inflation to make servicing the debt less punishing, because you are paying it back in cheaper dollars.

This is a cruel path, but it again points to the need for a safe haven.

Big trends in investment and finance follow large themes in public life. In a pandemic, money chases pharmaceuticals. In a war, money chases defense stocks. And when interest rates are suppressed, the money follows leverage.

If this is true, what does the gold and silver boom say about our times? It suggests upheaval in the stable monetary system dating back half a century and more. We are watching a gradual return to the real, perhaps not yet as policy but as investment. This is the core reason why everyone is talking about precious metals again.

It’s not a bad idea to head to the coin shop, just to see if they have any product remaining.