The tech boom is a hot topic stemming mainly from tech stock prices. While the sector, as reflected by, say, the Nasdaq index performing brightly over the last year, the overall picture was not good. Small cap indexes like the Russel 2000 were basically stagnant over the same period. Even broadly famous indexes like the S&P 500, excluding the “magnificent seven,” showed a much-reduced rise. No one would deny the unlimited future of tech, but what matters is how quickly it could be transformed into earnings. It seems the market is pricing in an increasingly distant future.

Another anomaly is the story does not seem true in other spacetimes. Japan was benefitting from advanced tech by the late 1980s, but it did not prevent the two decades after the bubble burst in 1990 from being lost.

Similarly, China’s tech, especially artificial intelligence (AI), has been bright in recent years, but the same kind of collapse as experienced in Japan two decades ago is still happening as predicted. Conclusively, tech by itself is not sufficient to lead to a persistent economic boom. Conversely, experience suggests that a prolonged economic bust could jeopardize the tech status afterward.

Although history shows that tech is crucial in sustaining an empire, such a long-term advantage cannot prevent any short-term cyclical or even structural (like Japan and China) bust, as just argued. A second thought confirms that tech is ultimately used to serve various sectors of the overall economy.

Thus, any economic downturn should, in principle, reduce the demand for these techs. In other words, tech’s advance should theoretically be procyclical, or in layman’s terms, it should be positively correlated to the economy. Let’s test-check this hypothesis.

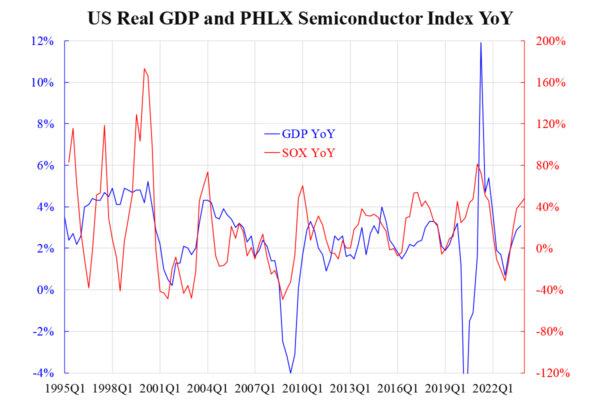

The above chart plots the U.S. real GDP series and the Philadelphia semiconductor index (PHLX, stock code SOX), and compares the year-over-year (YoY) change of both series. The correlation between the two is visually clear, at least in the medium-to-long term.

That says, the boom-bust cycle of the economy probably governs that of the semiconductor activity, except for the artificial recession due to the COVID-19 lockdown. Tech is a narrow kind of investment, so it is ten-fold more volatile than the overall economy, as shown by the scales of two vertical axes.

Notice prior to 2001, during the so-called dot-com bubble, that the SOX YoY was much more volatile than and somehow more detached from the GDP YoY. Now, the two are much more comparable, suggesting the market is much more realistic about tech than it was two decades ago.

Nevertheless, one can neither predict one from another, given the potential bilateral causality behind them. That is, one cannot claim there will not be any economic downturn ahead simply because the tech index is looking so good at the moment. Once turnaround happens, they turn together.

In fact, if we replace the SOX index with something similar to the Nvidia stock price (NVDA), a similar picture will be obtained. Accordingly, it seems wiser to argue from these observations that the U.S. will likely continue its tech empire than claim it will be shielded from any economic downcycle ahead.