In this tech era, most nations are talking about how “tech” they are. By definition, tech is something that enhances goods production or services provision by lowering costs, shortening time, or increasing scale (or a combination of these). It follows that with given (same) factor inputs, including capital, labor, and resources, output delivered within a certain period will rise. (Think carefully. We see this incorporates all three ingredients just mentioned). This is why tech growth is the residual of GDP growth unexplained by factor (capital and labor) growth.

Tech is intangible, but capital and labor are not. Capital (a stock) is the accumulation of investment (a flow) netting depreciation, while labor is simply manhours, which is measurable. Given output (GDP) is quantifiable, it does not matter whether tech is tangible but that it is derivable. Yet this is more than a simple subtraction because we want to exclude noise from the data: output might move not because of these factors but external shocks. A simple linear regression can remove such effects. Stated exactly, tech outputs less input contribution and less random noise.

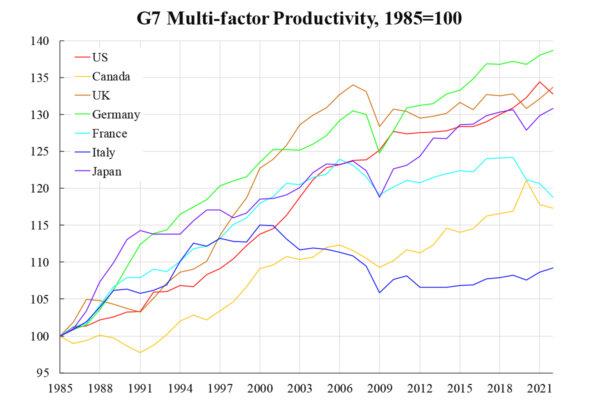

Most developing countries are producing fake official statistics; this is true even for large nations such as China, India, and Russia. If even the output number (GDP) is not trustworthy at all, any further analysis is bound to be garbage in garbage out (GIGO). Organization for Economic Co-operation and Development (OECD) compiles such tech series. It labels it as multi-factor productivity (MFP), which is basically the same concept as total factor productivity (TFP)—a common term used in economics. The accompanying chart shows the cases for G7 countries.

Notice that the series plotted are not MFP growth rates but the levels. There is a growth form of these series, but the discussion here belongs to a long-run macroeconomic (growth) context where yearly data are used; thus, presenting it as a level seems more suitable. One observation is evident: prior to 2000, the growth trends of the G7 MFPs were more or less at a similar pace. From then on, Italy (blue) was one exceptional member that peaked and declined, whereas Canada (yellow) turned stagnant. Others remained on an uptrend until recent years, when France (cyan) dropped.

The sustainable runners are somehow out of expectations to many. Germany, as a leader of Europe, has been regarded as lacking a growth engine, but the MFP uptrend has been decent. The UK is another country famous for its low productivity, yet this is inconsistent with data in the long run. Finally, Japan was thought to have never recovered for over two decades since 1990. It turns out that Japan’s MFP has been doing very well except for exceptional years like 2009. Frankly, Germany and Japan never gave up their tech industry. Probably neither did the UK.

Nothing sophisticated has been done in this piece; we present the data, reminding the reader that the actual data might be different from one’s deep-rooted impression. Then, one should not be surprised when U.S. stock indexes break record highs, as do the DAX, and probably so will the Nikkei and UK FTSE later on.

KC Law, Ka Chung