Since the previous Federal Open Market Committee (FOMC) meeting, where the Federal Reserve (Fed) reiterated a longer-than-expected rate hike and a later-than-expected rate cut, the shorter market rates then edged up. Yet, Fed funds futures show the terminal rate stayed at around five percent and moved within a small range of plus or minus 25 basis points. The market is likely to remain in a narrow range, and the terminal hike will likely end in March, May, or June 2023.

One of the possible reasons why the Fed gave such a hawkish signal is probably the persistently high inflation and a strong economy. This year, the core inflation rate has stayed at or above the 6 percent level, while the official unemployment rate remains at 3.6 percent. These are no doubt strong signals of overheating. Based on models of the past, the so-called equilibrium or neutral interest rate was probably three percent or below, but the current trend is upward of three percent or even four percent plus. The Fed funds target rate has just reached above this level.

With such a short period of tightening, one cannot expect any inflation reduction by now. The Fed was undoubtedly significantly behind the curve when inflation reached eight percent (in February) before the first hike. But a turbo chase of rate hikes in recent months does not mean inflation would decline immediately. Since inflation is no longer supply-side driven but demand-driven with a wage-price spiral, the mechanism to bring down inflation must be first to drive up the unemployment rate. That says it needs to create a recession in the first place.

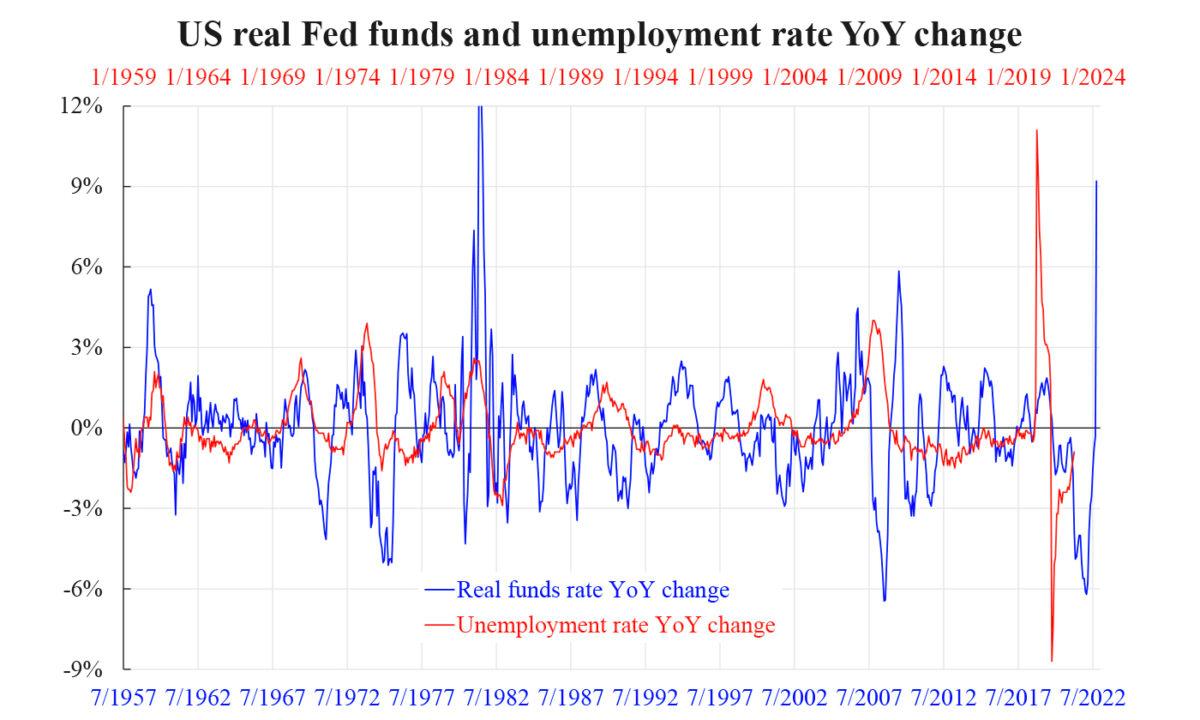

To see this, we have to identify the exact relationship between rate hikes and the change in the unemployment rate; or to be “exact,” we need to know the dynamics or phase lead/lag between them. For the interest rate to generate a real effect, it is the real rate rather than the nominal rate that matters. Thus, the real interest rate is the nominal rate minus inflation. The chart shows a six-quarter time gap to see a correlation between an actual interest rate hike and a rise in unemployment. This time lag is more extended than many have thought.

In other words, the rate hikes since March would not generate a meaningful effect until Fall 2023. As the blue path projects, the red should come down first and then shoot up. This time lag means the unemployment rate might have a year-over-year decline first before rising! As the number a year ago was at 3.9 percent or above, the numbers ahead will likely remain lower than this.

This might be a dangerous signal for the Fed as it may already have gone too far (behind the curve again). They might falsely judge the economy as more solid than expected, yet the change can happen all of a sudden—termed the Minsky moment. If the housing market crashes, the likelihood will be even higher.