Sometime after the Second World War, economists became infatuated with a wild idea, one rooted in the scientism of the time. They put together a model of a perfectly functioning economy with large aggregates they imagined could be forced to play together. If something is imbalanced, the experts could push this button or that one as a countermeasure.

It was the valorization of economics as a profession. Economists loved it.

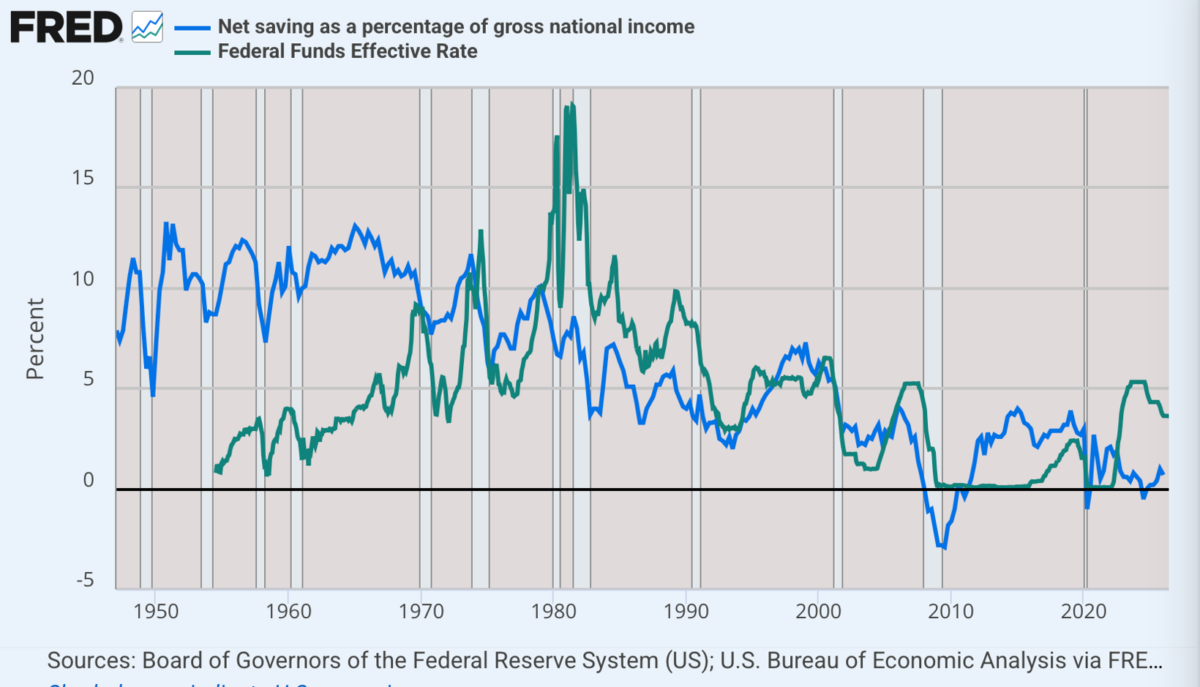

A key element here was the interest rate, which the Federal Reserve can influence in its relationship to its member banks. The federal funds rate could be turned up or down as a means of releasing more or less credit or liquidity into the macroeconomic environment.

The experiments were small at first and not very successful. For example, under the prevailing models, there would always be a tradeoff between inflation and unemployment. You could choose one or the other if need be. You could tame inflation but only by causing higher unemployment. You could drive jobs but only with monetary devaluation.

It’s impossible to describe the vast resources that went into making these models appear to be true. Every journal and every classroom preached them as doctrine for decades.

Then a funny thing happened in the 1970s. Empirical reality destroyed them completely. They broke entirely with the appearance of stagflation, namely high inflation and high unemployment existing at the same time. That was not supposed to happen. It happened anyway.

By the 1980s, the power to manipulate was still in place but the theory lacked any real integrity. Then came the 1987 stock market crash. Alan Greenspan, formerly an advocate of the gold standard, completely switched his opinion. He put out a statement the following day: “The Federal Reserve, consistent with its responsibilities as the Nation’s central bank, affirmed today its readiness to serve as a source of liquidity to support the economic and financial system.”

That was it. No more presumptions that the Fed would carefully manage the macroeconomic environment toward long-run stability. The Fed henceforth would serve as an emergency provider of liquidity. It would bail out the financial markets with newly printed money. Science had broken so the new policy became expediency as a first principle.

The Fed abandoned science as a cover and embraced its real job: backing government and the financial industry.

There was much more at stake, however. The manipulation of the interest rate introduced distortions in the production structure itself and completely changed investment incentives. We’ve never looked back from this switch. These distortions have lasted for many decades now and only became worse.

The best explanation of this relies on what is known as the Austrian Theory of the Business Cycle, as fully explained in the 1920s but with roots that date back centuries. The typical explanations of the theory are wildly overcomplicated. So I will attempt here to explain in the clearest possible terms.

Let’s begin with how economic structures are supposed to work. In classical economics, the savings rate shapes the interest rates, which pays a return on thrift, one roughly equal to national productivity or general output. That in return reflects financial returns. So in the long run equilibrium, you have interest = savings level = output = financial returns, with due consideration for innovation and surprise and so on.

This basic understanding was the consensus in the 18th and 19th centuries. An underlying presumption of that consensus was that money was not a tool of the state. It was sound, based in gold or silver. That presumption ended with the final blow to the gold standard in 1971. Money became paper, printable unto infinity. That create a terrible moral hazard for the central bank.

When the Fed forces down the interest rate, it begins to skew the classical equation. It makes leverage more profitable than saving by gaming financial returns, such that borrowers always make money by diverting leverage to investment. This creates a mess. It’s been going on for decades. In some ways, it is shocking to consider.

In a loanable funds world of classical economics, the natural interest rate emerges from people’s time preference and the marginal productivity of capital. Savings supply loanable funds; investment demand for them. In steady state, higher savings leads to a lower natural rate and longer, more roundabout production processes that boost future output. Investment patterns match savings patterns which fit with the willingness to delay consumption for investment.

The rate of interest roughly tracks the economy’s sustainable growth/productivity trend. Financial returns, real investment returns, and the return on thrift stay aligned. Deviations come from real shocks (tech, demographics, preferences), not systematic policy distortion. This is the coordination mechanism: interest rates are prices that balance present and future investment and output.

Where the Fed’s intervention breaks stability is when a central bank (the Fed) pushes the market rate below the natural rate via credit expansion/reserve creation. It doesn’t increase genuine savings. It creates “fiduciary media” or new purchasing power for borrowers before savers have deferred consumption.

This falsifies the price signal. Borrowers (especially leveraged ones—corporations, real estate, financial institutions) see cheap capital and ramp up long-duration, high-order investments (skyscrapers, tech infrastructure, asset purchases) as if society had become more patient.

Savers, facing artificially low yields, either consume more, reach for yield in riskier assets, or get crowded out. Leverage becomes the dominant strategy because the “return on borrowing” exceeds the distorted funding cost. Result: a malinvestment boom. Resources flow into projects whose completion would require higher future savings than actually materialize. The structure of production lengthens unsustainably while a false prosperity dawns.

When the credit expansion slows (or can’t accelerate fast enough), rates rise, asset prices correct, and the liquidation/reallocation phase hits. That’s the bust. It results from a period in which borrowers always make money by diverting leverage to investment. It’s not that every project succeeds—many don’t—but the aggregate effect is overinvestment relative to voluntary saving, plus a bias toward financialized and speculative plays.

This is exactly what the Greenspan “put” did. It falsified signals that ended up punishing the very people that a classical economic structure would reward: the savers and careful investors. It subsidizes borrowers to benefit financialized industries. It subsidizes long-term projects in a while that it not supportable by underlying saved resources.

In 1987, this kind of policy was just getting started. The same and worse happened with the turn of the millennium, following 9/11, and in 2008, to the point of absurdity. The Fed slammed rates to 0 percent. At this point, all capital was directed toward borrowing and using financial markets as nothing but a time arbitrage opportunity. So long as financial earnings were higher than borrowing rates, the clever money would win the game.

The Fed tried to unravel this ridiculous program in 2019 but then came the virus. The central bank doubled down yet again on zero rates, prompting more absurd distortions. This went on for three years. At this point, all bets were off. Leverage became a way of life, a deep addiction. There was no going back: not for Congress, not for corporations, and not for households. The result was a devastating inflation but also the financialization of everything.

It was the result of policy, one that punished thrift while leveraged corporations took over, resulting in the creation of private equity that gobbled up everything in sight while small business and the traditional workings of consumer-centered capitalism withered.

The only real path forward is through sound money and a Fed that lets the interest rate float as it should. Given the level of savings—real savings from households and businesses—I’m assuming that short-term rates should be far higher than they are. But the credit addiction is so pervasive today that this is not likely.

The beauty of economics is that it elucidates forces that cannot be gamed. Try it and you end up with a mess every single time. You can only paper over those messes so much. We’ve tried and it has not worked. The Austrian theory explains how and why. Tragically, it is not loose money that catches the blame but rather capitalism itself. In this way, discretionary monetary policies pave the way for socialist agitation and political shifts toward tyrannical government.

The lesson: never mess with the interest rate. Nothing truly good or lasting every results.