Congress has been taking baby steps toward medical insurance reform for some years, with slight improvements along the way.

What we really need is a giant leap in the direction of liberating the people from the grip of government, insurance companies, medical associations, and pharmaceutical power. What we need right now is an actual marketplace, not the artifice of a marketplace established by Obamacare years ago. The system still survives, and it is seriously hurting the jobs market now.

Every new hire in any firm with more than 50 employees mandates a $30,000 expenditure for health insurance in addition to other costs and liabilities. This might be tolerable in a booming economic environment, but in harder times, it produces exactly the “no-hire, no-fire” environment that has hobbled U.S. labor markets.

The medical insurance system is so complicated that it is nearly impossible to follow pricing trends. This is by design.

I had a friend who needed a certain patented nasal spray, but it was going to cost several thousand dollars a month without insurance. So he signed up for a crazy system with the usual combination of monthly premiums, co-pays, benefits packages, and deductibles—all terms that mean something different from what they used to mean.

To his amazement, the insurance came with a coupon that made his nasal spray available at no charge. Meanwhile, he is paying $1,500 per month for services he does not use. And the service he gets, by the way, is not even a service; it’s the right to a $50 doctor’s visit. But if you consume anything beyond that, it’s out of pocket up to $7,000 with a $10,000 maximum cost per year.

At least he thinks this is how it works, but he cannot be sure because insurers are always in the position of accepting or rejecting claims. Plus if he is traveling out of state, he cannot be sure to find a provider that will necessarily accept his insurance. And if for some reason his nose gets fixed, he is still paying more than his mortgage for services he does not use.

Among those insured services he doesn’t want are what are called “preventive care.” This is tacked on to every single plan in the Obamacare marketplace. You cannot unselect it. Even in the most basic “catastrophic” plan, there is preventive care. Maybe that seems like a rational idea because a stitch in time saves nine, as the old saying goes. Better to prevent illness than pay more later.

But anyone with experience knows that this is not what preventive care really is. You pay for it, but it is essentially an opportunity to sell more services in the form of diagnostics, screenings, examinations, and vaccines, some of which are included under conditions and some are not. You might not want any of this, but there is no way to decline them. They are bundled as part of every defined benefits package. Preventive care is a sales funnel.

This is just one person. Every single insured person faces some version of this. It’s nearly impossible to generalize about what this looks like for people because each situation is different. Only one thing is clear: The insurer and the insurer’s contractors are making profits while the actual service providers (the doctors and nurses) are buried in paperwork and not making much at all.

Nothing else in the consumer marketplace works this way, with prices, services, costs, benefits, and fees flying in so many different and often unpredictable directions. No product and no service in a market economy is similarly structured. Not even other forms of insurance function in this manner. With home, life, and auto insurance, you know for sure what you are paying and the conditions under which it works in your interest according to your individual risk profile.

If you are on a plan provided by your employer, you are taught to think of your health insurance as a benefit. What people often do not understand is that whatever benefits you get come out of your salary. In principle, you are splitting the cost with your employer, but that’s not necessarily real either because the employer has to get the resources to pay from somewhere.

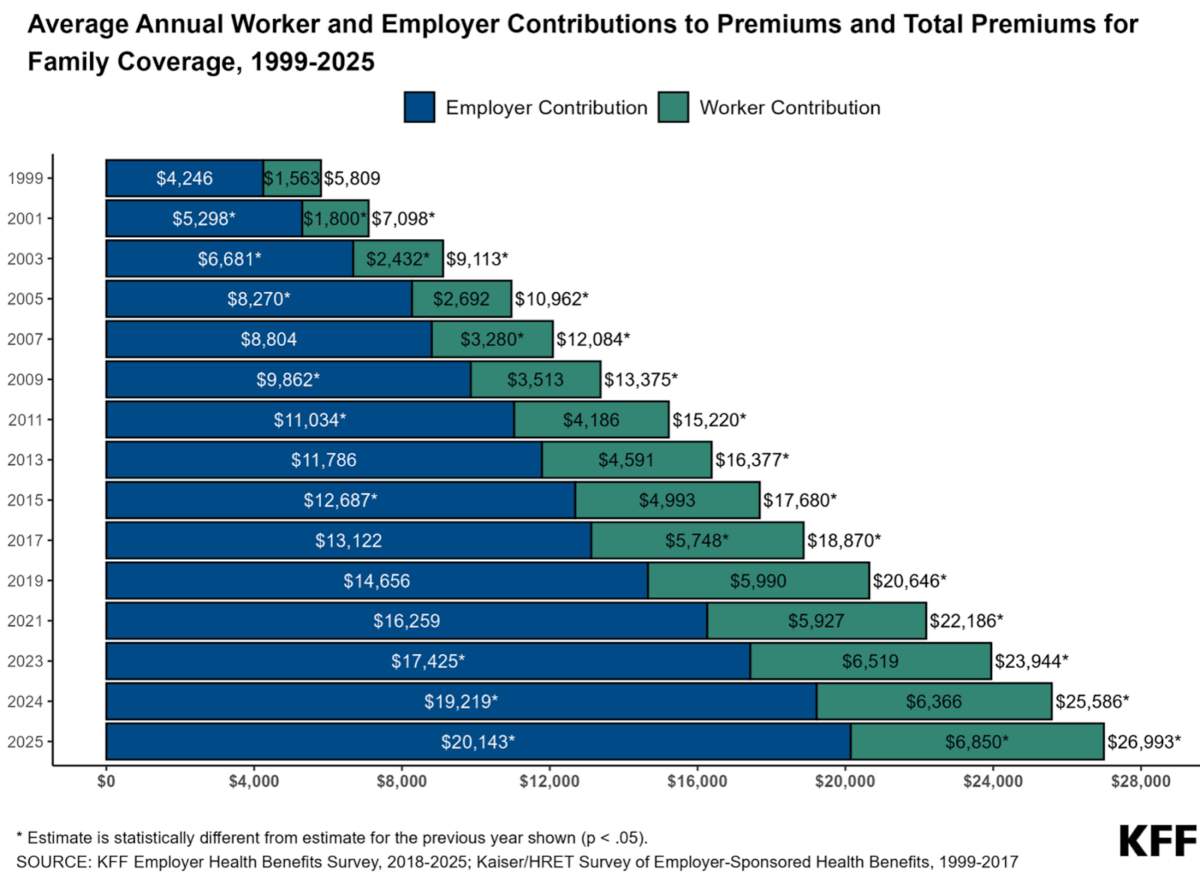

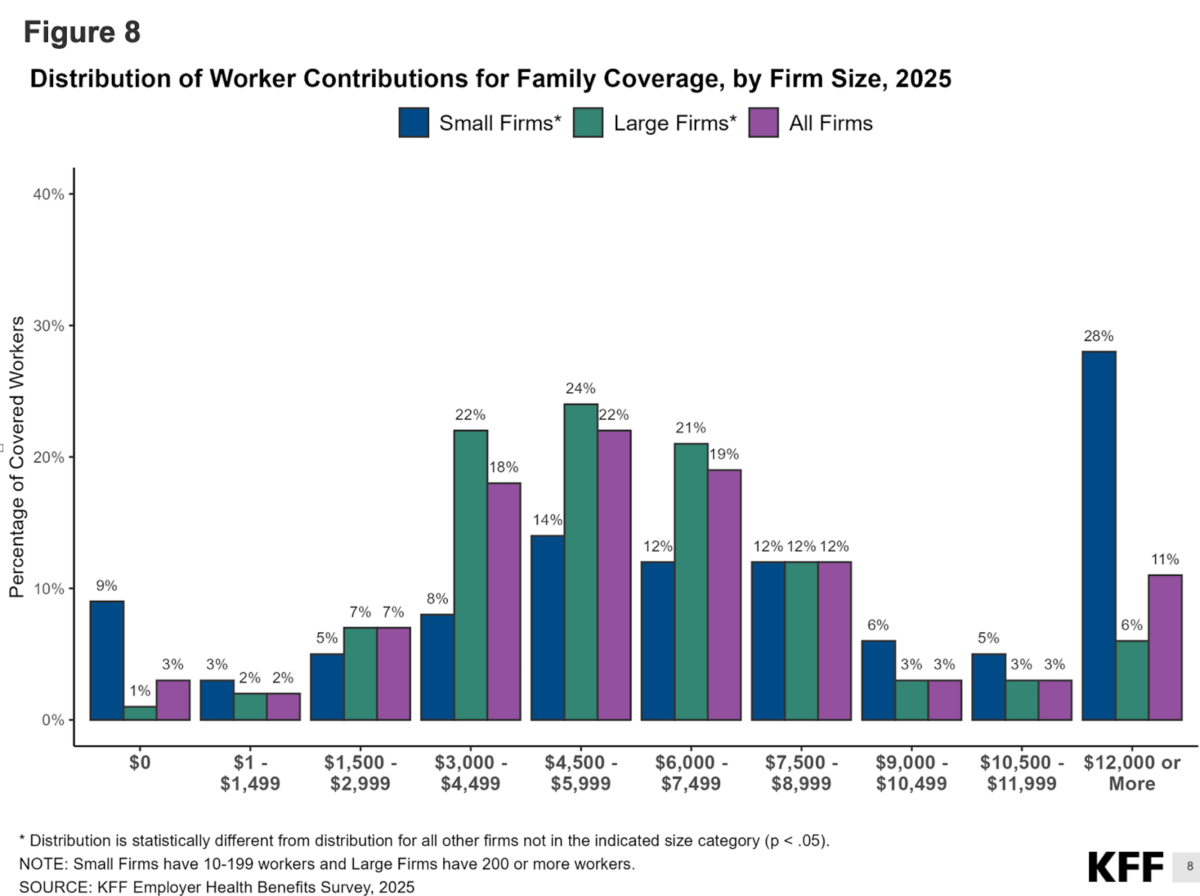

When the 2026 numbers come in, there will be shock and awe. The distribution of costs for these plans hit small firms particularly hard and increasingly so. They are bearing an ever-higher burden relative to large firms.

The costs are rising enormously, particularly this year. Every so often, I check the marketplace to see what I would pay as an individual. Having just checked, it is now double what it was just three years ago, from $800 to $1,600, with a deductible beyond co-pays and a list of free benefits that I don’t really want but for which I must pay anyway.

None of this is sustainable. It is killing hiring. Individuals who are in a position to do so are actively dropping their health insurance and living off whatever benefits have been accumulated in a legacy health savings account. It is far more rational to drop coverage entirely, live well, limit risks, and bank the money.

Other options for people include doing medical tourism abroad or joining a medical co-op such as a health share company. They can be religious or secular. They are not insurers as such but can cover medical bills at prices that are a small fraction of the expense. These are growing in popularity for a reason. But employers cannot use them under existing law.

Digging through the enormous bureaucratic mess—as complicated as or more so than any Soviet economic plan—makes one wonder: Maybe all this confusion exists for a reason. It makes it harder to reform. Hardly anyone can wrap one’s brain around it with enough clarity even to improve it.

This is why it is best to focus on principles first, and those principles are decentralization, patient choice, and direct producer-consumer relationships between customers and service providers. Keeping those principles in mind leaves one with four huge priorities right now.

1. There need to be off-ramps for employers to hire people without the mandate that they provide health insurance. There also need to be tax-advantaged ways for employees to trade in their benefits for higher wages and salaries. This would not be a difficult change, but it addresses a crucial problem in the American medical system today, namely that of third-party payments. This is an accident of history in any case, a result of wartime price controls. This system should be ended completely with incentives, and the mandates on business must be relaxed to the point of eventual abolition.

2. Insurance providers need to be liberated entirely from defined benefits plans. Providers need to be able to offer plans with any range of benefits, even the most minimal, with any premiums, co-pays, deductibles, maximum spends, and the rest of the preposterous financial machinery. There is no reason why individuals could not be paying as low as $100 a month for minimalist coverage.

3. Every individual should be permitted to save for medical spending needs without facing tax consequences. That is to say, the right to a health savings account should not be contingent on already having health insurance. This way, people would just accumulate capital under personal control and thus eliminate the moral hazard of feeling as if you have purchased benefits that you are not using. Millions would flee the system now in favor of personal control of medical decisions.

4. I cannot resist one final push to put actuaries to work assessing individual health risk rather than forever being forced into risk assessments based on large population pools. No other insurance system requires this. Indeed, authentic insurance means insuring against particular risks that pertain to the insurance case in question.

If a reform plan did these four things, the most pressing problems of the medical marketplace would be largely solved. There are many other issues to address, but nothing can happen as long as these reforms are not in place. The Republicans should already have done all this last year. Now it is probably too late. They will pay a big political price for this, because there is a growing population impatient with the awful system as it is.