As a nation, we have decisively crossed into a new era as marked by the status of home ownership. It is out of reach for the rising generation of professionals, even those who are well paid and have two income streams. Homes are competing with every other expenditure demand and losing such that it is now almost impossible to achieve for most people.

Private equity is buying up a large stock of those available and the super rich are gobbling whole neighborhoods. The dream that lasted three quarters a century is fading if not already extinct.

That marker is an important one for national psychology. This is because home ownership was central to the construction of the American dream during the Cold War. Starting in 1948, the United States applied vast federal resources to boosting ownership as a way of showing the Soviets what capitalism could produce. The ideal was the nuclear family in a stand-alone house owned and not rented on a single income.

For generations, this was a point of American pride. And it lasted after the Cold War ended, as the national expectation persisted. Houses have not in living memory been treated like a regular good but something in need of relentless promotion and protection. When housing prices began to fall dramatically in 2008, this was seen as a national crisis justifying extreme efforts to prop up prices.

Looking back, this was a bad policy, same as any government policy that favors one form of consumption over another. This path distorts market signalling, This was already obvious by the 1980s. By the turn of the century, the sector had become wildly overblown with cheap credit and funky financial schemes. A collapse of a third or more in pricing is exactly what the doctor should have ordered to make homes more affordable. Instead, the policy was the opposite. Every effort was undertaken to blow the popping bubble back up again.

This policy never made any sense. If the bubble rooted in sloppy risk assessment in mortgage-backed securities was the problem, why would you want to recreate the problem that the bust revealed? This speaks to a core piece of economic wisdom. There is always a reason for a bust, always an explanation for a popping bubble. It is telling us something about reality that we need to know and ultimately achieves something good.

That’s a wisdom that has been forgotten. I recall watching the unfolding of events with a sense of profound confusion. On the one hand, there were all sorts of recriminations concerning who blew up this bubble. On the other hand, every effort was being made to raise prices as if that would fix the problem. No, it does not make any sense. If housing prices had been allowed to settle back in 2008, we might not be where we are today in this position in which the vanishing middle class cannot afford a home.

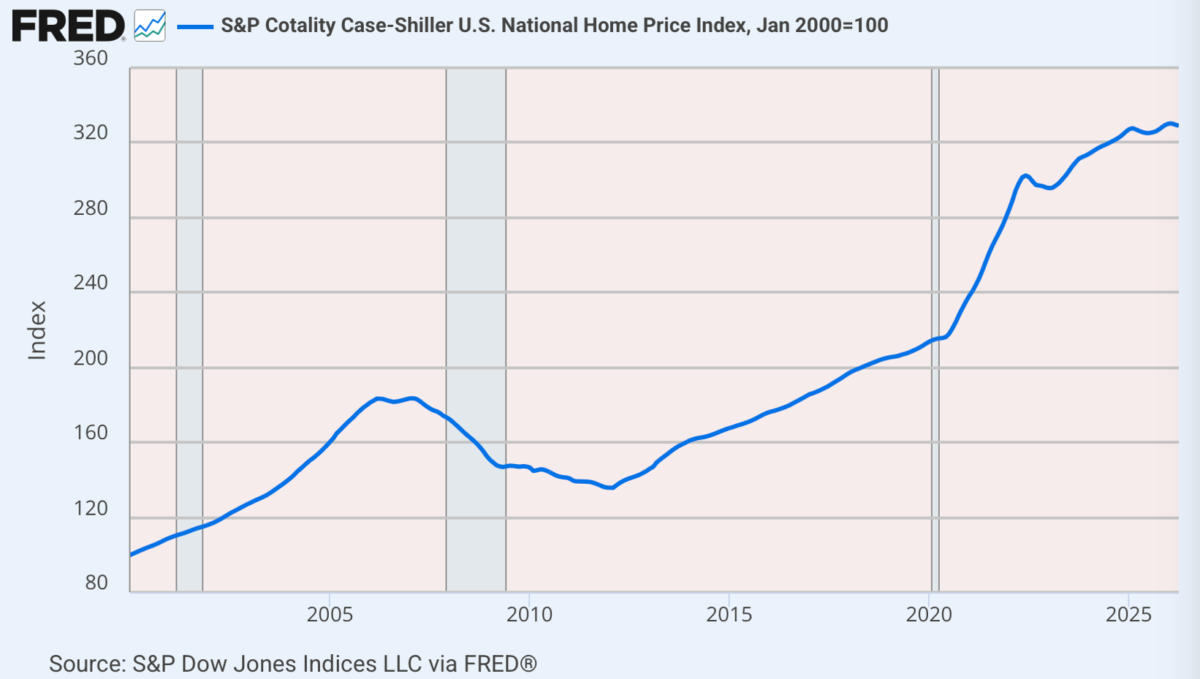

House prices are more unaffordable than ever. Redfin data calculates this threshold using a $430,000 median home price, 20 percent down payment, 6.5 percent mortgage rates, and housing costs under 30 percent of income. Home prices have climbed to $540,600 for new builds, up from $350,000 a decade ago, while wages lag behind amid a 2-5 million unit shortage fueled by zoning limits, high costs, and homeowners locked into low rates.

Just consider that in 1950, half of the population was married with a home by the age of 30. That number has declined through the decades, hitting one quarter in 2010. Today only 12 percent of the population is married with a home by the age of 30. That is more than a small change. That is a revolutionary shift.

Economists call for more supply through easier zoning and permitting. Tax cuts would be great too. There are ways out of this predicament. But that raises the taboo topic: do we as a society really want lower house prices? Donald Trump had promised to increase supply but then reversed himself, observing that many people have most of the wealth tied up in their homes. If prices fall, that kills savings too.

There is a bit of an illusion operating here. When we say that people have their wealth in their homes, that is not in the form of liquid funds. Sure you can borrow against equity but that’s very risky and even dangerous. If you do not, your very high house price gets you absolutely nothing other than a pretty picture of some numbers on a Zillow page. If you get joy out of that, fine, but that’s not the same thing as discretionary income.

And yes, you could sell. But if there are no buyers for your product, you might have another source of trouble. You might wait and wait an uncertain period of time.

Keep in mind, too, that vast numbers of existing owners are carrying mortgages locked in at 2 and 3 percent while a new mortgage is going to cost twice as much. So you would certainly have to downsize your property and make much more for less. Most people don’t want to do that, which means essentially being locked into one’s home and luxuriating in the belief that it is of high worth even if there is nothing you can do to unlock it.

Generally speaking, it is a poor policy decision to decline to pursue any direction that might cause prices to fall where they need to be. Seeking to boost supply, restrict supply, keep prices high, and lower them are mutually incompatible goals. In effect, the decision to keep housing prices inflated amounts to a huge subsidy to Baby Boomers at the expense of Gen Z. This only further drives young people to more terrible ideas like rent control and socialism.

It makes no sense at all that a couple with a combined income of $150,000 cannot afford to buy a home. It’s because of the 232 percent increase in housing prices over 26 years. People were slapping heads and wrists over the housing bubble of 2008 but it was already blowing up again after 2012. Today there is no concern that this is a bubble and yet you only need to look at the charts to see what kind of disaster is brewing here. It’s a post-lockdown boom that makes the old boom look like a warmup.

It’s only a matter of time before price pressure tips the other direction simply because markets will run out of buyers who can afford to enter the markets.

With all this said, let me offer you a different perspective sent to me by a reader who is a real estate agent. She says that young people are buying houses all the time but doing so requires a change of values.

“Let me tell you what they knew. They knew it would take sacrifice just like every generation before them had to sacrifice to reach their goal. Just like the athlete practicing for years to get to their dream of the Olympics. The principle is the same. What they didn’t do was wear designer labels, drive high-end cars, go on one or more vacations, and spend on hair and makeup. They cut back on eating out and they brought their lunch to work every day instead of going out to lunch. They kept the same iPhone for years and so on. They sacrificed, just like every generation before them had to in order to buy a house. The issue is not they can’t, the issue is they are not willing to do what it takes to reach their dream of a house.”

It’s not a bad point. We have not only an affordability crisis. We have a values crisis. People raised in a time of exploding prosperity have no idea what it means to do without. We can see this in exploding credit card debt. You can see it every night at the downtown bars and restaurants. If these people are constantly pleading poverty, why are they spending $400 for a night on the town, $1,500 for concert tickets, and $3,000 for a beach vacation?

We need to get real. In the old days, people knew that living well requires deferring consumption, saving money, thrift, and economization, not just keeping up with the Joneses, as they used to say. We’ve forgotten that money doesn’t grow on trees, even if the Federal Reserve acts like it does. For a few years from 2020-2023, it seemed too. That experience made a huge mess of a generation’s perceptions of what it takes to be prosperous.

Fixing the housing problem is not merely technical. It speaks to the spiritual collapse over 75 years. You can have prosperity and you can have an entitlement mentality but you cannot sustain both for the long term.