Commentary

The potential U.S. debt ceiling and U.S. dollar status problems reignite the discussion of de-dollarization. The status of U.S. dollar will no doubt be firmly anchored in the financial market, which has already been discussed here previously. But the U.S. dollar share of goods trade is claimed to be jeopardized by the Chinese mouthpieces and some international bodies recently. For foreigners, one camp expresses this openly to please the Chinese Communist Party for more business. Another camp might have this thought based on recent observations.

There are at least two observations to consider. First, China did get more trade partners invoicing in their bilateral currencies (non-U.S. dollar), and second, China and some of her trade partners did have a higher share of goods trade invoicing in their bilateral currencies. Yet there are subtleties here. On the first point, most newly joined countries are very small in economic size or even on the brink of some sort of crisis. On the second point, the share of non-U.S. dollar goods trade is still very small, although it has been increasing in some of these countries, mainly at a few percentages level.

Although China is concerned; its largest export destination is still the United States, taking 17 percent. The second is Hong Kong taking 8.5 percent, while the third and fourth are Japan and South Korea, already taking less than five percent. Among Hong Kong’s main re-export destinations excluding mainland China (57 percent share), the largest is again the U.S. taking 6.4 percent. One can see even China cannot evade receiving U.S. dollars from exports. Among the top 14 export destinations, Hong Kong probably might pay non-U.S. dollars (yuan); the next is already the 15th largest–Russia.

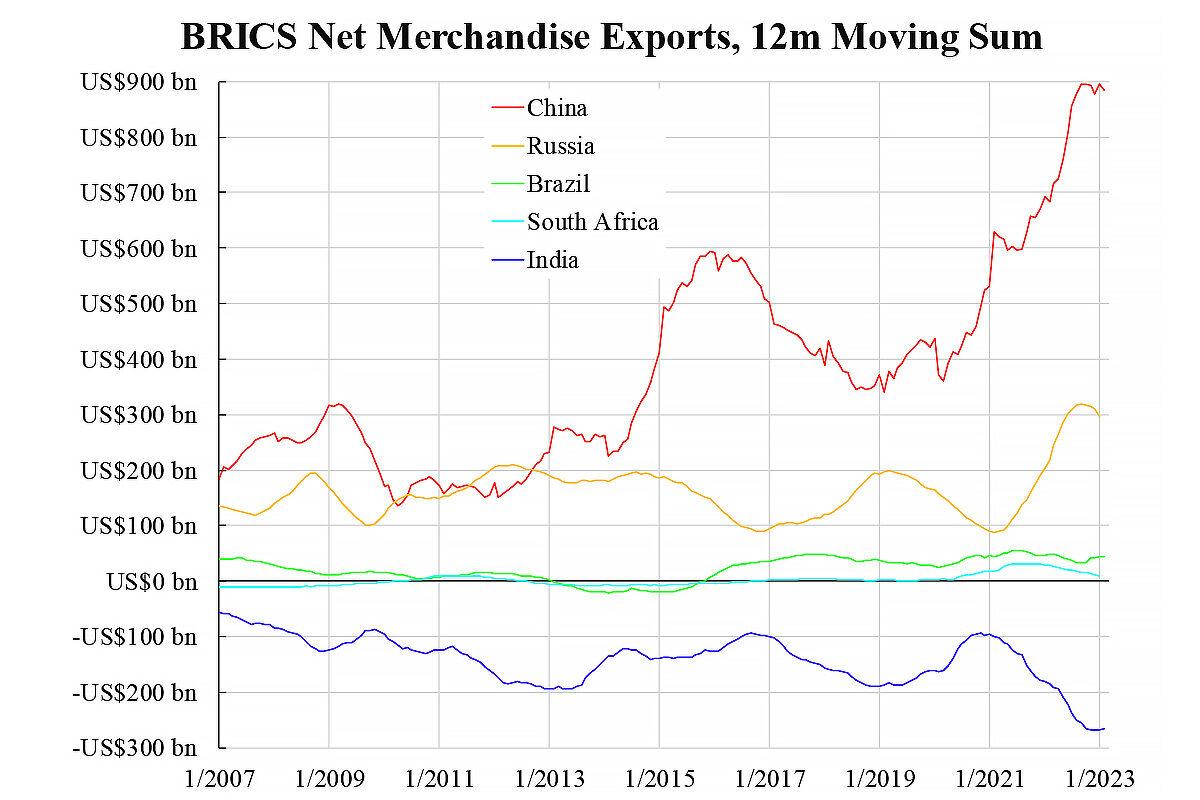

Viewing the issue more broadly, one can see such de-dollarization among the camp of emerging markets (EMs) is infeasible. The accompanying chart shows net exports of BRICS based on World Trade Organization (WTO) monthly data annualized by a 12-month moving sum. Among these giants, EMs, all but India are net exporters, meaning that they all are net receivers rather than net payers of foreign exchange. From the balance of payments (BoP) point of view, only India has the potential to build up an international currency as only she keeps paying.

Here are the subtitles again. India imports the most from China, double the amount of her second largest importer United Arab Emirates (UAE). Would China and UAE be willing to accept Rupee by exporting to India? The answer is obvious. The Chinese mouthpieces keep praising the yuan internationalization, yet they just empty talk without understanding how this can be achieved, with earning export foreign exchange being another goal at the same time. Even China-Russia cannot be a sustainable pair because both of them are large net payers.

According to the 2022 WTO data, the United States is still the largest net importer, which is already larger than the sum of the second to tenth largest net importers together! And all G10 belong to the Western camp. As countries in the anti-U.S. camp are mostly net exporters, de-dollarization remains just an empty talk stage at this stage.