Recently, there were reports that Shenzhen in southern China had its residential property prices slashed by half. Soon after, the Chinese government launched rescue measures, which plans to force banks to lend to the sector even without collaterals. The funniest thing about this is the first clause among the “Three-not-lower-than” requires lending to the real estate by each bank to be no lower than the corresponding industry average. How can every member be no lower than average? Unless all banks lend the same amount.

Previous analyses suggest banks were reluctant to lend but held lots of notes to meet the lending pressure exerted by the government. This is also evidenced by the pattern of sharp lending rise at the end of each quarter (March, June, and Sept.) over the recent year or so.

Early this year, there was already a “profits let” pressure by the government, requiring banks to lend their profits to the property sector. The recent measures reflect banks did not follow suit and are now being forced to do so. This further reflects that the situation is bad enough that things are collapsing.

Were the market to bottom out right now, such forced lending would not be of any problem. But is it? From the official data, housing prices have been coming down from the peak for only a year. Past experience elsewhere suggests housing busts, on average, last for 4.5 years. See, for example, “This Time is Different by Carmen Reinhart and Kenneth Rogoff.”

Experience in Hong Kong gives the same conclusion where the three housing busts over the past six decades lasted for 4.5, 3, and 6 years, respectively. Those 1-2 years retracements are not really busts but corrections.

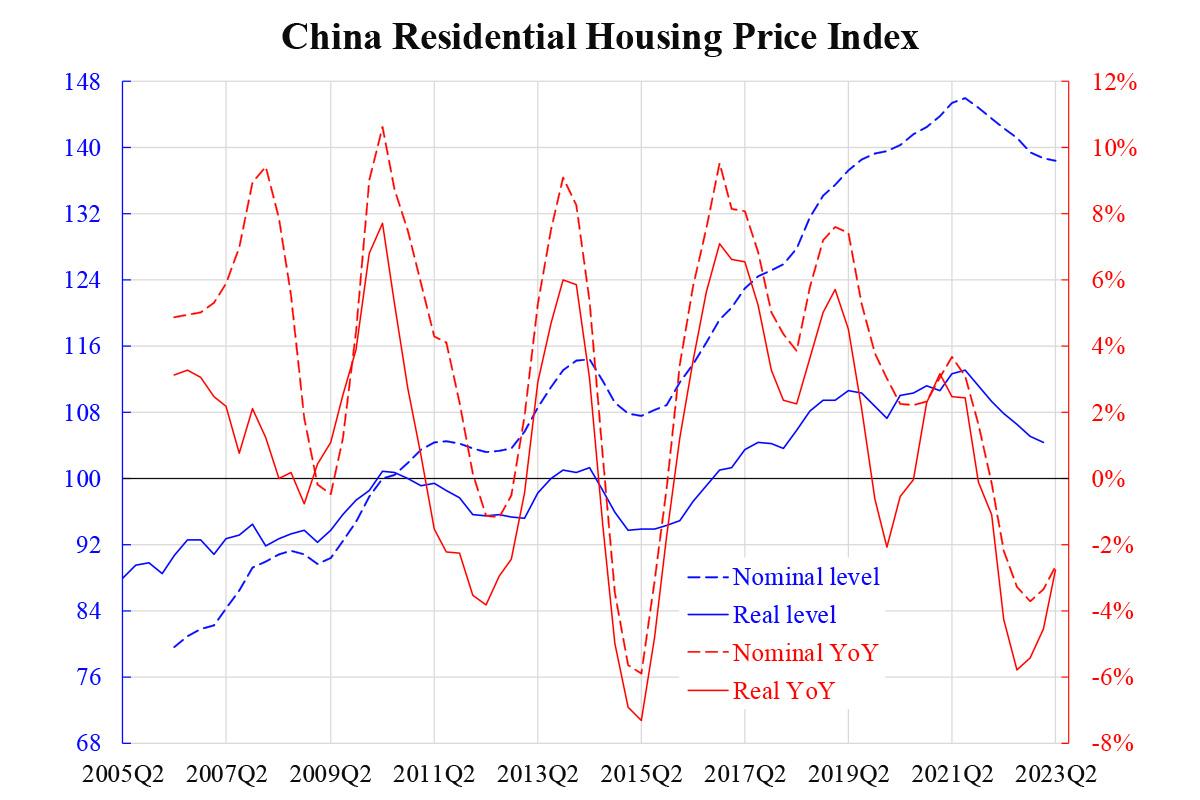

Is China now experiencing merely a correction like that in 2014? It seems unlikely due to a completely different set of circumstances. From the real housing price, we can see it wasn’t really rising prior to 2017. After that, however, the real price surged quite a bit while the economy was running down. There are two kinds of fundamentals behind exogenous versus endogenous factors. The former refers to affordability, which mainly means income and mortgage rate. The latter refers to demand relative to the supply of housing. The exogenous factors were obviously bad.

The endogenous ones were also not good. Those “ghost cities” had been reported for a decade, and recently, there were extreme claims saying the vacancy would be enough for three billion people, more than double the existing Chinese population of 1.4 billion. Even though the actual excess might not be that serious, it is unlikely in near balance. With both unfavorable exogenous and endogenous factors, housing prices must decline meaningfully to reflect these. Experience elsewhere suggests some one-third to two-thirds nominal decline is needed.

Although a specific price cut could be at this discount, the overall index is far from that. This is why banks are reluctant to lend because no one believes the bust is done at this moment. The rescue measures will not make the price go up.

KC Law, Ka Chung