The BRICS camp will include six more members. As is wishfully thought by Russia, this will de-dollarise the world. De-dollarising the financial world is nearly impossible, without any doubt, given the overwhelming dominance of the U.S. dollar. What the BRICS camp regards as possible is de-dollarising along the line of external trade. Although external trade involves goods and services, the latter is mostly absent in many emerging economies. These countries mainly export natural endowments (fossil energy) or labor-intensive cheap products.

Among the eleven members of future BRICS, China is the only potential candidate to “internationalize” its currency through trade. There are several measures of currency share, including bank transactions (by Bank for International Settlements) and central bank reserves (by International Monetary Funds), but only that by Society for Worldwide Interbank Financial Telecommunication (SWIFT) is relevant to external trade and most favor China. The next BRICS member on that list is South Africa, whose rand (code name ZAR), ranked 21st with a share of only 1.3 percent.

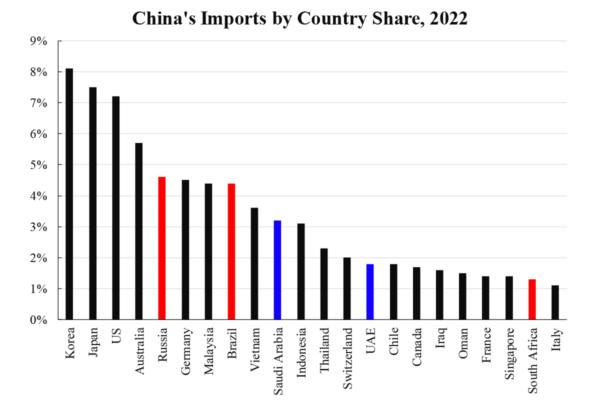

Were China to “internationalize” its currency within this camp, then at least China would need to (net) import substantially from the other ten countries to pay them yuan. But this precondition is not satisfied. As the accompanying chart shows, only five out of eleven BRICS members were among the top 20 plus (actually top 30) of China’s import partners in 2022, with two of them (in blue) still not yet joined. All these five partners add up to only 15 percent of total China imports. These add up to $380 billion and are less than 1 percent of M2 reported at the end of 2022.

Indeed, not all of China’s imports from these countries were settled by paying yuan; in fact, probably only a tiny portion was done so. Thus, the potential room for the yuan to “internationalize” in the BRICS camp by way of external trade (essentially imports) is small.

Look at the major import partners again. The first four and Germany belong to the Western camp and will certainly not be accepting the yuan. The successive candidates, including Malaysia, Vietnam, Indonesia, and Thailand, are, in theory, potential members to accept the deal. However, none of these South Asian countries plan to join the BRICS camp. Moreover, there has been massive production relocation from China to these countries. The acceptance of the yuan might mainly reflect this kind of activity which used to be conducted in China.

Whether to settle a trade in which currency is ultimately the decision of entrepreneurs. Even if the platform is there, business decisions depend primarily on realistic factors such as exchange rate and interest rate outlook and any potential sovereign or country risks. The answers are already on the wall since the outburst of COVID-19 and then China’s debt crisis with persistent yuan devaluation and interest rate cuts. This explains why BRICS and South Asian countries add up to a decent portion of China’s trade, yet the yuan takes up only 3 percent of the SWIFT payments, which is already the record high share.