The New York Community Bank (NYCB) crisis recalls the banking crisis of last March. Similar to what happened last year, crises always emerge suddenly, without clear symptoms beforehand. At the end of January 2023, NYCB’s stock price plummeted by over 30 percent in a day and continued to drop to 30 percent in a few days afterward. We cannot easily claim the U.S. market is inefficient (in terms of information flow), but the iron fact is almost nobody is aware of a crisis of this kind until the collapse takes place. This seems to be the intrinsic nature of a crisis.

Since the financial tsunami in 2008, many types of early warning indicators or signals have been developed by academics and policymakers. Various scholars build different models and arrive at different conclusions. Some conclude that sharp changes in asset prices, like equity or housing busts, are indicative. In contrast, others conclude fundamentals like credit or debt or GDP ratios are the key indicators of bank health. Some even compare different composite indicators to evaluate which kinds are the best. As a least common multiple, almost everything counts.

We all know many factors are important, but it will not be of much use without simplifying to one or a few candidates. One key difficulty here is undoubtedly due to the nature of the crisis. Such nature is chaotic and unpredictable, such as physicists not being able to predict weather and geologists not being able to predict earthquakes. Because each chaotic event has complex dynamics behind it, factors cannot be identified with high certainty by standard analysis like statistical modelling. This explains why different scholars conclude differently despite their work being scientific.

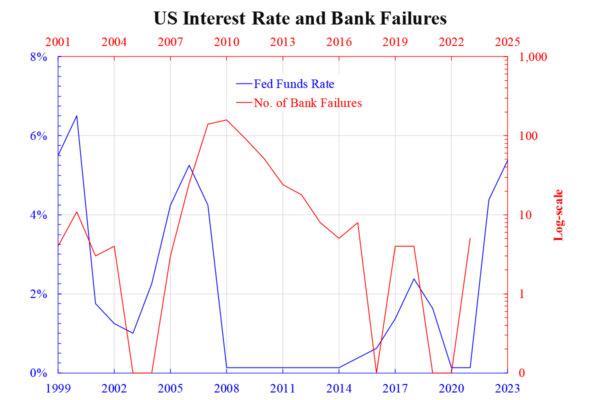

To visualise this idea, we might try using interest rate as a single factor to predict a crisis. We all know bank (and even company) balance sheets are sensitive to interest rate movements. Interest rates, being a theoretical cause of banking crises, should not be difficult to establish. Empirically, policy interest rates somehow lead to bank failures by about two years, as the attached chart shows. Even with some technical tricks, such as employing a semi-log model (taking log only to the dependent variable), the explanatory power does not look high.

Not every rate hike cycle would have the same impact on bank failures. Not only is the time lag between rate hikes and bank failures unstable, but the lagging effect of rate hikes also varies from time to time. This poses a great difficulty in making it an early warning signal, especially when the timing is highly uncertain. In fact, many other factors share a similar nature by producing highly uncertain relationships. One can imagine when all these uncertain indicators are aggregated into a composite, no one really knows the mechanism that is going on inside.

While the exact spacetime is unpredictable, it does not mean the event itself is unknowable. Like China, where banks are heavily indebted in the bursting real estate sector, such a potential crisis is knowable, albeit not many symptoms are reported. In this sense, these are not really black swans (unforeseen events).

KC Law, Ka Chung