Even assuming a naïve linear downtrend of YoY core inflation from September 2022, it will not return to 2 percent until the year’s end. The latest rebounded MoM core number suggests two things: First, so far inflation downtrend is still driven by the energy bear market. Unless energy prices keep plummeting, there will not be too much downward driving force in the coming months. Second, there is still fundamental, persistent upward pressure behind, which is likely due to the strong real activity. The latter is, in turn, a result of previous monetary accommodations.

In principle, if excess money generated solely nominal effect without real effect, then a complete withdrawal of such excess should drive inflation back to the original level. In reality, however, monetary policy would have both nominal and real effects (just a matter of how much each). The real effect generated would also accelerate inflation. To curb this part, the real activity needs to cool down before inflation can come down. If this real activity refers to the labor market, then the sign of slowdown is certainly unclear, given the latest strong job numbers.

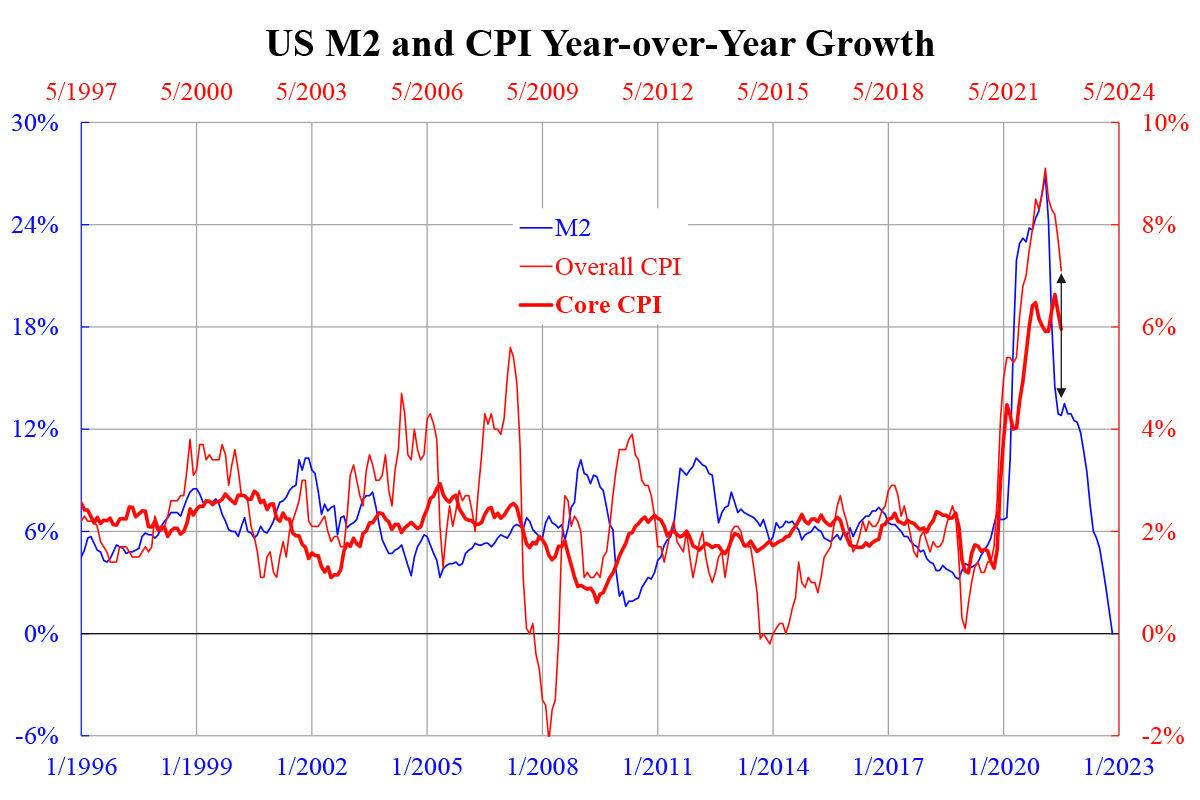

Accordingly, the monetary tightening so far seems to have curbed only the direct nominal effect. Here tightening refers not to using interest rate hikes but to a cut in broad money growth. As we have discussed before, the time gap between money and price growth can be up to 1-1.5 years which is confirmed empirically again from the accompanying chart. Nevertheless, this updated chart shows a wide gap between the latest inflation and the predicted level from previous broad money growth. The shortfall is likely because the real effect failed to be curbed.

Since the tightening started 16 months ago (the time gap between the two horizontal time axes), the shortfall is not due to a delayed effect not yet seen. Rather, it is likely the extent of tightening is not enough—a space problem more than a time problem. Intuitively, even if inflation is lowered while the interest rate is hiked, the real interest rate by now is still negative even for the lowest measure of inflation (core PCE) being subtracted by the highest measure of interest rate (6-month Treasury yield). This is not tightened at all since 4.x percent is merely a neutral level.

All these suggest inflation will not come down very quickly. A probable exception is when a housing market crash happens. If it does not happen and inflation remains high, Fed might be forced to hike until it does happen—isn’t it a fate that cannot be avoided?