Fifteen years ago, the entire housing sector sunk from its highs. Because so much debt is involved in this market, carried by banks but then bundled without regard to risk and resold in financial markets, this turn of events precipitated a financial crisis that spread around the world. Government and central banks undertook unprecedented actions to save the system with bailouts.

Meanwhile, homeowners around the country found themselves in a strange position of being financially underwater. This happens when monthly mortgage payments are far higher than the existing property values can justify. The test was this: If you could sell your home in the morning and buy it again in the afternoon and make much lower monthly payments, the property is underwater.

As a result, people just started testing the system. The bank says they'll repossess your home in the event of nonpayment; fine, take it. Anything is better than burning cash at this rate. Homes around the country stood empty as bankers rocked up to shells stripped of lighting, fireplaces, toilets, and appliances. Crazy times.

In 2007, the conventional wisdom was that housing as a sector could never face such a crisis. The sector is too diffuse. Prices are mainly affected by local conditions. The risk profile of mortgage loans is individuated and not likely to be systematically wrong. The system is solid, they said, and not vulnerable to dramatic cyclical shifts.

Stop worrying!

At the end of 2008, everything was different. The people who said it would never happen disappeared from public life or changed their story. Suddenly, the airwaves were full of voices claiming that they knew all along that this would happen. And, truly, some people did warn.

The response by the government seemed to work, but it was always fishy. The Treasury worked with the Federal Reserve to bail out banks and financial companies on a selective basis. It was called “quantitative easing,” a neologism for credit expansion or old-fashioned money printing. It just sounds more scientific that way.

Friends of big shots got billions of dollars while their competitors were allowed to go belly up. The financial sector was carefully culled, leaving mostly compliant firms who know how their bread is buttered.

The Fed itself embarked on a newfangled zero-interest-rate policy, or ZIRP. But aren’t positive interest rates a normal feature of the market economy, and aren’t we kind of playing god to force the system into some other pattern that would suggest that time has no cost and that money is infinite?

Shut up and trust the experts, they said. The central bankers have it all under control. The guy in charge of the Fed, Ben Bernanke, was later awarded a Nobel Prize for his amazing innovation of making interest rates go away. He’s a magician, and he saved the world!

Some people predicted terrible inflation. I was among them. Where did we go wrong in our predictions? We hadn’t paid close enough attention to the little card trick that Bernanke had up his sleeve. For all the billions and trillions of dollars in quantitative easing, the Fed allowed the banks to use the new paper to build their balance sheets back up. But instead of lending the new money on markets, the Fed just decided to pay the banks to keep the money off the streets.

This was the whole point of ZIRP. If money pays nothing in the market and the Fed is paying something, the banks have every financial incentive to keep their deposits stored at the Fed. That way the money printing won’t result in any serious inflationary effects.

If you are following this, you might be thinking: This is all pretty nuts. How can the Fed create trillions of dollars in fake money, give it to banks that they can add to the asset side of the ledger, then that same money flows back to the Fed to earn interest, and then we thereby claim that a system in collapse is now newly sound? This all sounds like alchemy.

And it was indeed alchemy—just as foolish and fake, but it can work so long as no one is testing whether that thing that shines like gold really is gold.

Meanwhile, there was indeed a massive cost to this policy, but it was less discernible and socially distributive than inflation, at least in the short term. The zero-interest-rate policy had two main effects on the production structure. It discouraged savings and investment in short-term projects simply because they were paying zero or negative returns. The only real action in the markets—money hates being dormant—was in more speculative and long-term projects.

Among those “roundabout” production processes that ended up with a giant subsidy were media companies, tech companies, large corporations, and, of course, housing development. In other words, the solution to the problem of the housing bust was to double down on the very conditions that led to the problem in the first place! The result was a massive distortion that lasted from 2008 until very recently.

Watching all this unfold in real time was surreal.

“Housing prices are collapsing. What should we do?”

“Let’s bring them back up again.”

“But maybe they were too high, the sector overbuilt, and perhaps this is an opportunity to restabilize the markets with a housing sector that operates in a more realistic way?”

“Are you crazy? No, we are going to fix the problem by recreating it!”

And so they did. Did we learn nothing from 2008? We learned, but they didn’t. They merely patched up the problem temporarily. They deal with the question of overextended mortgage markets by creating the very conditions that would guarantee the problem would happen again.

Those of us who pointed this out were simply shouted down. In a culture in which we only live for the day, think only about the next election cycle, scramble simply to keep low prices at bay, and think only about surviving from one opening and closing bell to the next, our critique of the policy fell on deaf ears.

And here we are a decade and a half later with a problem that isn’t only similar, but worse. After the lockdowns and the trillions of dollars printed up to cover up the devastation, housing boomed to impossible degrees. In the fall of 2020 and extending for nearly a year later, many homeowners were faced with crazy great offers on their homes.

People were frantically moving to get out of lockdown cities and states and move where mysophobia was less on display. Plus, Americans were flush with cash because the wise and benevolent government was dumping it directly into the pockets of the citizens, giving generous payments to everyone for no apparent reason. They wanted to spend it on something and deposits on homes, especially at zero percent financing, seemed like a good bet.

If you wanted to prevent another housing boom–bust, U.S. policy was perfect. Look at mortgage rates adjusted for inflation. They feel lower than ever after 2008 but nothing compared with life after lockdowns with zero rates plus inflation kicked in. This is exactly a prescription for a repeat of disaster.

![(Data: Federal Reserve Economic Data [FRED], St. Louis Fed; Chart: Jeffrey A. Tucker)](/_next/image?url=https%3A%2F%2Fimg.theepochtimes.com%2Fassets%2Fuploads%2F2023%2F04%2F21%2Fid5212336-1-JAT-2023.04.21-1200x917.png&w=1200&q=75)

Once the Fed started noticing inflation, it decided to clamp down. The difference between 2020 and 2008 was the missing card trick. No longer was the Fed paying higher than market rates for bank deposits. Instead, the new money was arriving into bank balances via deposits from individuals and businesses. Banks scrambled to find a home for it in fixed-rate bonds that soon became devalued when the Fed repriced the debt with a new interest rate policy.

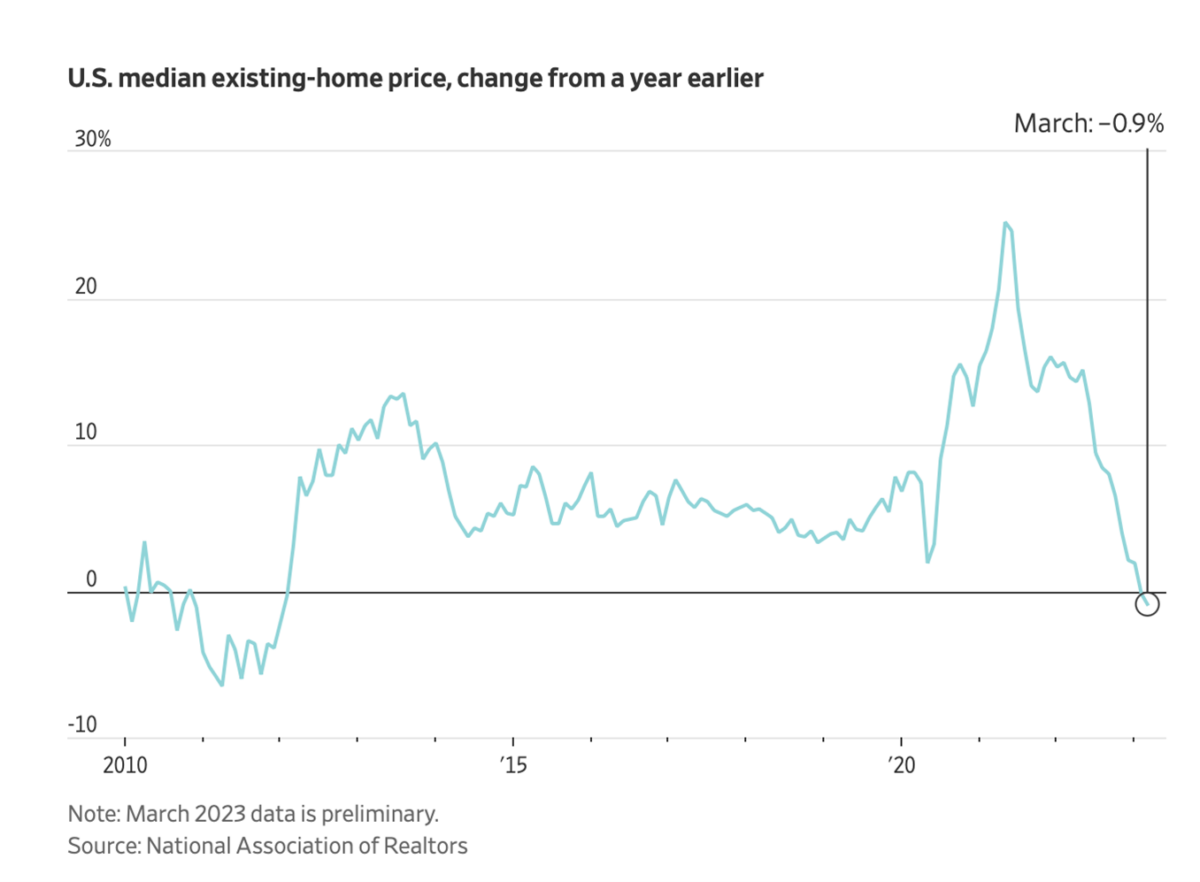

Sure enough, median prices in March 2023 were down by 0.9 percent, the second consecutive down month for the first time in 11 years. Sales of existing homes in the same month were down by 2.4 percent from February and 22 percent from a year earlier. Mortgage rates are up too: 6.39 percent from 5.11 a year earlier.

The trouble with such deflationary markets is that consumers don’t know precisely when to act. Buying now could land you in a situation with a leveraged asset that still has further to fall. And there can be no doubt that this is going to happen. The housing price index is still rising in real terms given inflation but falling in nominal terms. As inflation cools over the coming months, the whole sector is going to face tremendous deflationary pressure, the same as in 2008.

Incredibly, the federal government under Biden just released a new formula for pricing mortgage risk that actually punishes the best borrowers to subsidize the worst. This is a major factor in how things got so screwed up last time.

Why do we keep doing this? The short answer is that these policies are in everyone’s short-term interest even if they’re disastrous in the long term. And herein lies the problem: The whole of U.S. policy today revolves around surviving another day. The Fed is enabling this financial pathology.

There’s no question that the Fed will bail out housing again, especially since it’s working hard now to create room within its balance sheet and policy structure to initiate yet another round of quantitative easing or whatever they'll call it next time.

If the resulting crisis is big enough, maybe Fed chief Jerome Powell too will be rewarded with a Nobel Prize in economics!