The Federal Reserve has had an artificial demand boost due to likely supply shortages expected as a result of the COVID-19 pandemic leading to a near double-digit inflation, the dollar-decline voices have also re-emerged.

Such voices have not been heard for some decades.

The first time could date back to the early 1970s when the Breton Woods system collapsed and the U.S. dollar value was no longer linked to gold. Money moved from the U.S. dollar to gold at the onset.

However, gold cannot be a substitute for money in daily transactions and its price bubble burst a decade later in the early 1980s when high inflation was curbed.

Other candidates were expected to emerge to challenge the dominance of the U.S. dollar.

The 1950s to 1970s were bright times for industrial development when Germany and Japan were top performers. Naturally, their currencies—the German mark and Japanese yen—were expected to rise and take over some share of the market from the U.S. dollar.

Although the Plaza Accord in 1985 boosted both currencies to appreciate for five years, both countries then fell into prolonged recession. The German mark has since disappeared into the Euro and the Japanese yen depreciated sharply and the U.S. dollar has continued to dominate world markets.

The same story repeated in 2007 but this time the candidate was China. Before that, there had been loud voices claiming that the Chinese yuan would take over from the U.S. dollar. Since the financial tsunami in 2008, Chinese economic growth has been coming down linearly for a decade, and China’s capital account is still closing tightly where capital outflow pressure remains very high.

Some cycle believers would argue that after a century of the U.S. dollar’s leading status its dominance is already coming to an end. They point to the pound sterling’s leading status that lasted more than a century from the industrial revolution to after World War II but there is nothing concrete to argue a similar duration for the U.S. dollar. To see the status of the U.S. dollar as money, it is necessary to examine how currencies are normally valued.

Apart from a unit of account where nowadays most monies can perform (while gold cannot), the other two functions—medium of exchange and store of value would be crucial to judge the status of the U.S. dollar.

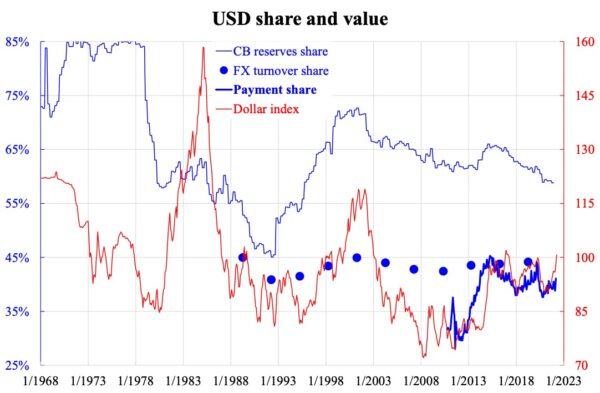

The former is often measured by two standard yardsticks: the FX turnover share as reported in the triennial survey by the Bank for International Settlements and the payment share by SWIFT. While the latter is updated monthly, its history is short and only goes back to 2010. The triennial survey has a longer history but is infrequent; the next update will be at the end of this year.

From the accompanying chart, the FX turnover share seems to move in tandem with the dollar index, but the movement has been limited to a narrow range of 40 percent to 45 percent.

For payment share on the SWIFT platform, it moves much closer to the dollar index; the volatility seems larger but has been mainly confined to 38 percent to 45 percent. The two conclude a similar 40 percent share.

On store of value, the indicator is the worldwide central banks’ reserves share by currency. The U.S. dollar share has been declining since the formation of the Euro in 1999 but is still sitting at around 60 percent. Even though the U.S. dollar may not lead forever, it is not expected to lose its status in the short run.