This copy is for your personal, non-commercial use only. Distribution and use of this material are governed by our Subscriber Agreement and by copyright law. For non-personal use or to order multiple copies, please contact The Epoch Times Reprints.

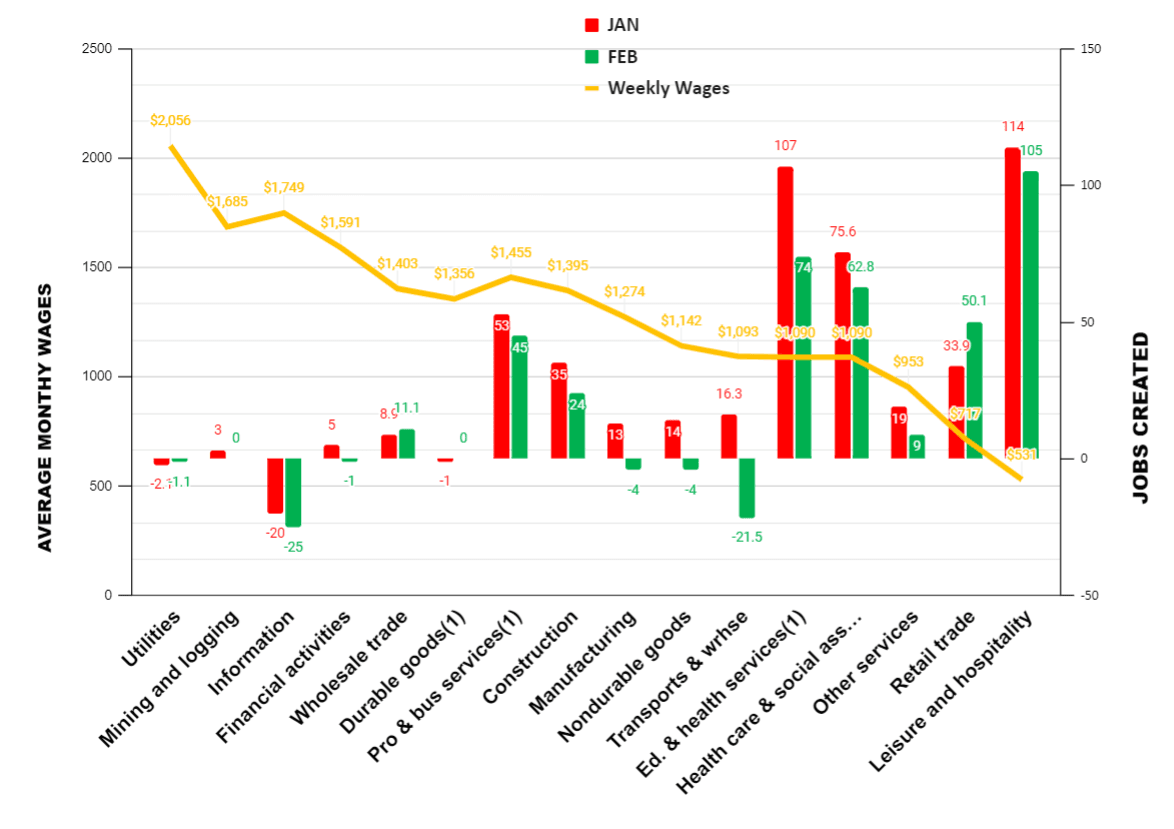

New jobs created printed at 311,000 on March 10, according to the Establishment Survey, far exceeding market expectations of 205,000 jobs. The Household Survey printed lower at 150,000. Net revisions were down 34,000 from December and January. The overwhelming majority of jobs were in the lower-wage sector, and job losses occurred in some of the higher wage sectors, as illustrated in our exclusive chart of Jobs Creation by Average Weekly Wages.

(Source: The Stuyvesant Square Consultancy, "February Jobs by Average Weekly Wages (Establishment), 2023)

The Federal Reserve

Notwithstanding the recent jobs report, the overall focus of the markets has been on the Federal Reserve. We had predicted in November that the terminal rate would settle somewhere between 5 percent and 6 percent, likely closer to 6 percent, and even possibly as high as 7 percent. We reiterate that view today. In his testimony earlier this week, Federal Reserve Chair Powell left little doubt that the Fed was set to increase rates, but would be data-dependent. Members of the policy-making arm of the Fed, the Federal Open Market Committee, will supply their dot-plot projections at the next Fed meeting on March 21–22. Those projections will help the public judge the Fed’s future direction.

Depending on next week’s release of the Consumer Price Index, we expect the Fed to return to a rate increase of 50 basis points (bps), possibly—but not likely—75 bps. (A basis point is 1/100 of a percent.) Many, however, expect the Fed to go more lightly, at 25 bps. Those others support that view by the moderation in the rate of increases in hourly wages and continue to assume a “soft landing” is in sight. We reject the notion of a soft landing, and think it far more likely the Fed will increase rates and then pause in the third quarter, as the effects of the recession we predict in that quarter sets in (it will be declared in 2024).

Our view on that is contingent upon the assumption that there is no widespread contagion from the March 10th seizure of Silicon Valley Bank (SIVB) by California banking regulators. We understand SIVB had a highly concentrated, little-diversified balance sheet. So while a large bank in its own right, it is not one that is considered a “SIFI,“ or systemically important financial institution, as of 2022. We note bond yields are dropping as bond prices increase on enhanced investment risk from alternatives, largely on what most see as a declining economy.

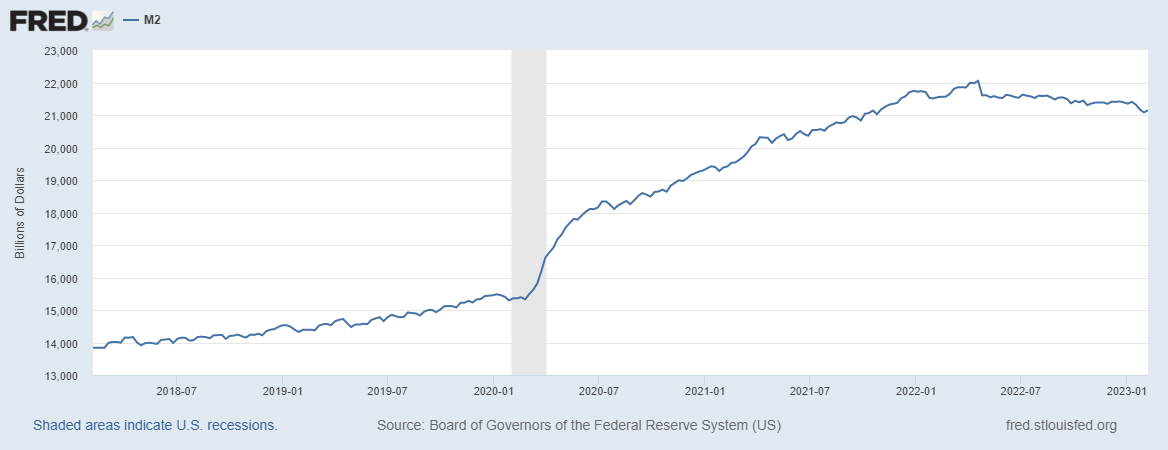

All that aside, the overwhelming cause of the inflation is the astronomically high level of money in the economy. Money, measured as M2, pumped into the economy for pandemic relief is still more than 33 percent higher than it was pre-pandemic, from $15 trillion to more than $21 trillion today. While the Fed has taken measures to wind that down, it has done so far too gradually in our view. We’ve said so, and repeatedly, for some time. We should be down to first-quarter 2021 levels by now.

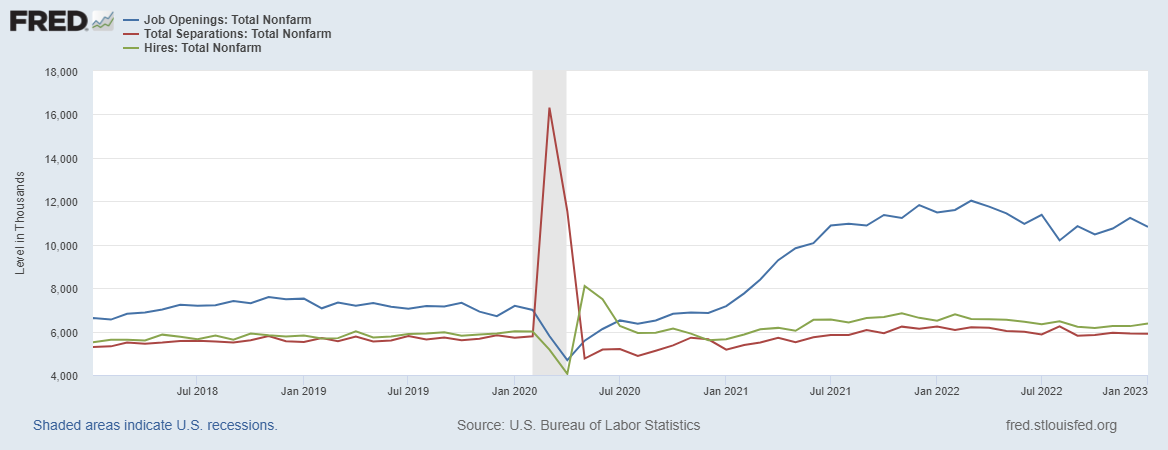

The other driver of inflation is an “America sitting on the couch.” As illustrated below, job openings far exceed hires, so that employers have to pay higher wages to coax workers back into the workplace. Pandemic food relief ended in February and other benefits ended some time ago. That may help force more workers back into the workforce; however, many of those seeking employment lack the skills of retiring baby boomers and the fact that some younger workers eschew manufacturing jobs as somehow beneath them. (This is one of the leading drivers of Washington lobbyists’ arguments for more work visas for foreign workers and immigration reform.)

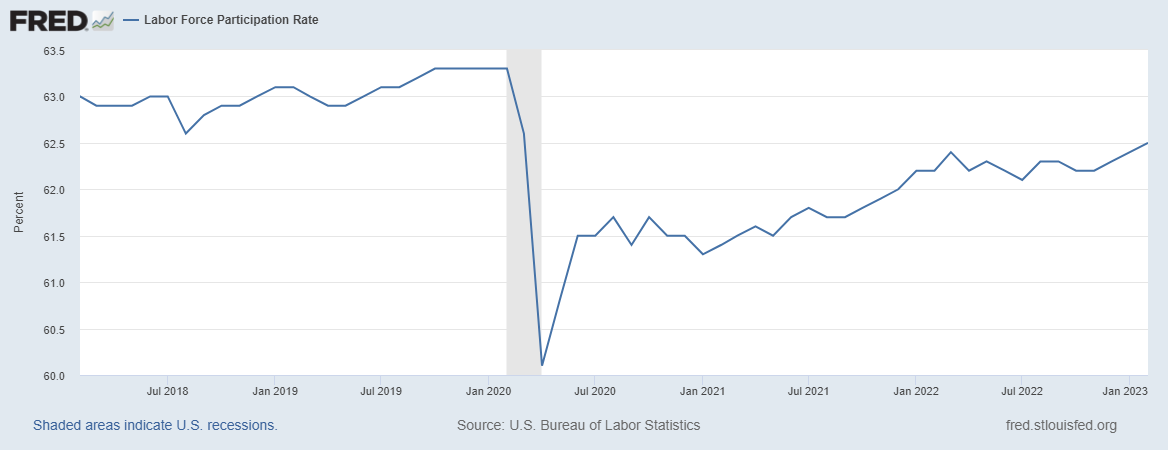

Nevertheless, the labor participation rate—that is, the number of people working or looking for work—is improving, it remains well-below pre-pandemic thresholds. Those people need to come back to the workforce to lower wage inflation and inflation overall.

Republican budget proposals to impose a work requirement on recipients of food stamps and Medicaid are likely to further improve the participation rate. Under President Bill Clinton, for example, who promised to “end welfare as we have come to know it“ as part of his campaign, a work requirement imposed by the Republicans in 1996 trimmed the welfare rolls, because recipients were required to show up for work. It turned out that several million recipients of welfare had been working ”off the books,” so that requiring them to show up for a welfare-benefits job forced them to choose to either remain on welfare or continue their off-the-books job. Most chose their off-the-books job, so that welfare, in the form of aid to families of dependent children and temporary assistance to needy families, dropped from 14 million to just 4 million.

Other Data

Labor productivity continues to disappoint, coming in below expectations while raising labor costs.

The Biden budget posits a 5.2 percent wage increase for federal workers, the largest federal wage boost in 42 years. This comes on the heels of statutory Social Security cost-of-living increase of 8.7 percent, the highest since 1981. Both will tend to exacerbate inflaionary pressures.

The TIPP Index showed respondents still have a negative, but improving, view of the economy.

Perspective and Prognostication

We reiterate our view that there will be a recession in the third quarter, and we think the Fed will move rates higher—most likely a 50 basis-point increase later this month—and continue to do so before pausing at the third quarter recession. There will be no “soft landing.”

We estimate first quarter GDP will print between 0.5 and 1.5 percent. That is, of course, conditioned on the Fed sticking to its 2 percent inflation target and not caving in to pressure from both the left and the right for a higher rate that we discussed before. We believe that departing from the 2 percent target would be a mistake and a significant risk to U.S. financial stability, and would result in the kind of stagflation—a portmanteau of stagnation and inflation—that existed during the presidency of Jimmy Carter in the late 1970s.

______________________________________________

NOTE:Our commentaries most often tend to be event-driven. They are mostly written from a public policy, economic, or political/geopolitical perspective. Some are written from a management consulting perspective for companies that we believe to be underperforming and include strategies that we would recommend were the companies our clients. Others discuss new management strategies we believe will fail. This approach lends special value to contrarian investors to uncover potential opportunities in companies that are otherwise in a downturn. (Opinions with respect to such companies here, however, assume the company will not change).

The views expressed, including the outcome of future events, are the opinions of the firm and its management only as of March 10, 2023, and will not be revised for events after this document was submitted to The Epoch Times editors for publication. Statements herein do not represent, and should not be considered to be, investment advice. You should not use this article for that purpose. This article includes forward-looking statements as to future events that may or may not develop as the writer opines. Before making any investment decision you should consult your own investment, business, legal, tax, and financial advisers. We associate with principals of TechnoMetrica, publishers of the TIPP Index on survey work in some elements of our business unrelated to that index.

J.G. Collins is managing director of the Stuyvesant Square Consultancy, a strategic advisory, market survey, and consulting firm in New York. His writings on economics, trade, politics, and public policy have appeared in Forbes, the New York Post, Crain’s New York Business, The Hill, The American Conservative, and other publications.

k

k