The sudden bull of the Japanese stock market in May called for a thorough review of Japan. Japan used to be excluded from Asia in the past decades, but concentrating on industrialization, its stock market expanded exponentially in the latter half of the 1980s. The recent Japanese stock index (whether Nikkei or Topix) is still below the 1990-year peak. Fair to say, it is not anything outstanding given after the depression, the U.S. stock index took only a quarter century to recover to its 1929 peak. Moreover, Japan’s latest quarterly real GDP YoY growth rate could barely evade consecutive quarters of negligible growth and contraction.

The overtaking of Hong Kong (stock market) and Taiwan (chips production) by Japan are driven mainly by external forces of U.S. and NATO. However, internal drivers of Japan’s sustainable growth are still lacking. While the external drivers prepare the investment channel, the consumption one still relies on domestic variables, particularly population. Japan’s declining population has been a problem for a long time, and there is not any way out. The population pyramid is still shifting towards the aging side, where the young age proportion is still shrinking.

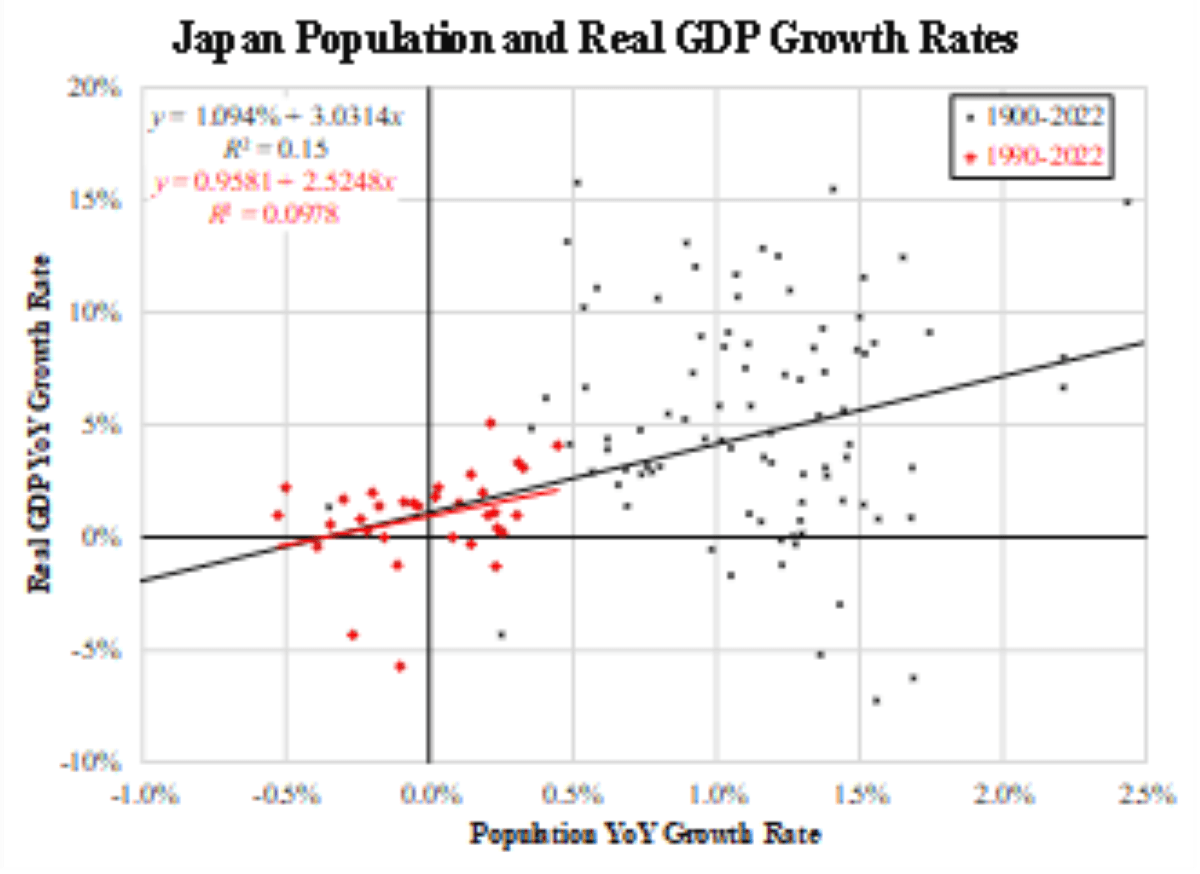

The accompanying chart shows the relationship between population and real GDP growth, both in year-on-year terms. Data from 1900 to now or those from the 1990 bubble burst to now suggest a positive relationship between the two, where the coefficients are both 3 after rounding. That says, a one percent decline in population growth contributes to a three percent decline in real GDP growth. In either case, as the population declines over 0.3 percent (which is already the case now), the real GDP trend would switch from expansion to contraction, a scenario worse than stagnation.

The sufficient factors might be more complex and subtle. It seems adding a big nation with positive population growth works. Between 2000 and 2007, mainland China plus Hong Kong together gave this mix. This has become a past tense now that Japan cannot mimic.

While you are bullish on Japan, bear all these in mind.