I’m writing this while traveling from Arequipa, Peru to Cusco, Peru. For me, one of the best parts of traveling is the serendipitous interactions I have with fellow travelers. Earlier this week, I was fortunate enough to have dinner with a doctor from Buenos Aires, Argentina. Iván Paz is working in Arequipa right now, and when I asked him how long he planned on staying, he told me that he was never going to live in Buenos Aires or his native Argentina again.

I visited Buenos Aires years ago, and like many, found it completely charming. It has the beautiful architecture, cosmopolitan services, and fantastic restaurants found in many European capitals. It also has the warmth and charm of a South American country. Men I just met hugged me. Women I just met kissed me. It’s hard not to love a visit to Buenos Aires.

Naturally, I asked my dining companion why he was so adamant about never returning. What follows is his story. I don’t understand Argentinian politics well enough to have an opinion about his views, but I can confirm that his economic analysis is sound.

When he told me that the annual inflation rate in Argentina was 40 percent, I asked him how mortgages were structured when someone wanted to buy a house. He laughed and replied that buying a house wasn’t possible. When I pressed for more information, Iván told me that almost a decade ago he bought a house. The bank financed 50 percent of the purchase price at a 14 percent rate; conditions that would cause domestic unrest here in the United States.

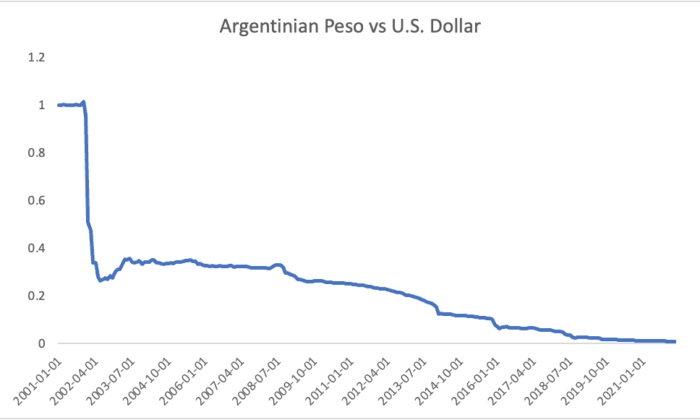

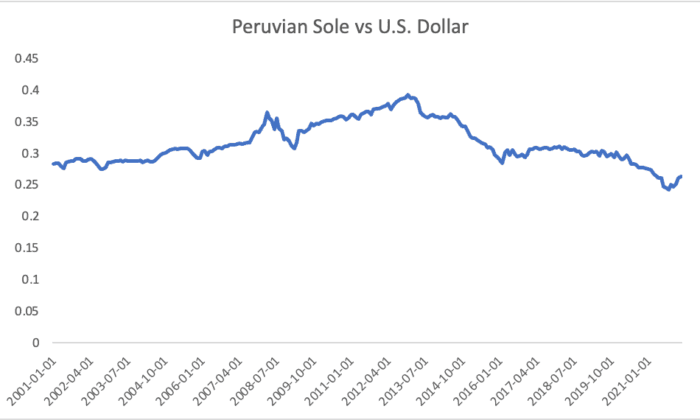

As proof that government policy regarding money supply and excessive spending matters, we show what’s happened to the currency of nearby Peru. Please note the relative stability of the Peruvian Sole versus the constantly plummeting value of the Argentinian Peso.

Despite mortgage conditions that Americans might consider awful, I realized that getting 14 percent financing when the value of the currency used to pay the mortgage payment was depreciating at 40 percent was actually a great deal. I asked my friend how the banks didn’t go out of business effectively lending at negative 26 percent, and he replied that the banks were fine because the government had guaranteed the bad loans. Astute readers will remember that the U.S. government supplying guarantees for bad mortgage loans was a key element of the 2008 great financial crisis. The story I was hearing was getting to be uncomfortably familiar.

I asked Iván what happened to these loan programs, and he said that a year after he bought his house, the loan programs were all closed. In fairness to the banks, there’s no reasonable way to make multi-decade loans when inflation is running at 40 percent. Iván said that now, if someone in a highly-educated profession (like a doctor) wants to buy a home, it takes about three years to save enough for the down payment on the land. That’s before buying a single brick, roof shingle, flooring, or plumbing supplies. He’s correct that under these conditions, it’s not possible to buy a house.

The U.S. Federal Reserve needs to respond to the current situation. Inflation is at a 40-year high, real interest rates are at record negative levels, and as of this writing, they’re still engaging in Quantitative Easing (increasing the money supply). Even the most hawkish (aggressive) members of the Fed think they’ll be able to get away with a 2 percent increase in interest rates. We don’t think the United States is heading in the direction of Argentina right now, but there are many parallels between Iván’s story and U.S. economic policy. Argentina represents a warning on how bad things can get if our institutions don’t take the current situation seriously.