China released a series of May economic data; all are better than expected and some show improvement from the previous month. But a month’s change right after massive lockdown is certainly not confirming a change of downtrend (to flat or up). Whether there will be a structural change is hard to judge simply from the latest trend. After all, economic data are not market data where technical analysis applies. Although a worsening economy will “ultimately” mean reverting and bottoming out, it is not easy to tell in advance from individual data series.

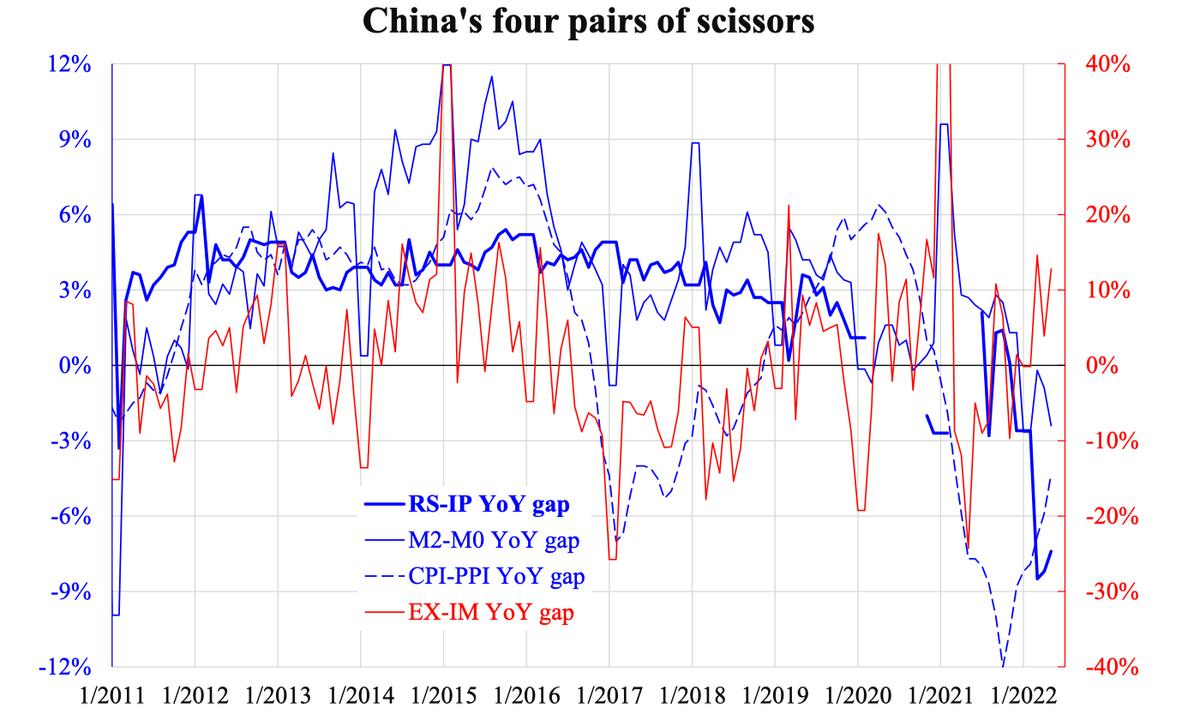

However, there could be some hints when related times series are viewed in combinations. From the released headline data for example, the gap between retail sales (RS) and industrial production (IP) growth rates gives the excess demand (with respect to supply). The difference in broad and narrow money (M2, M0) growth rates measure the multiplying effect of repeated deposit creations. The gap between consumer price index (CPI) and producer price index (PPI) growth rates captures firms’ profits, while that between exports (EX) and imports (IM) reflects the nation’s profits from the rest of the world.

For each of these pairs, whenever sign switching happens the Mainlanders term it as “scissors” where one cuts across the other. It is intuitive that economic outlook is good when these pairs of difference are positive. From the post financial tsunami period shown in the accompanying chart, the first challenge where some of these pairs dipped below the zero line was in 2016. That was an emerging market crisis rehearsal where eye of storm was in Middle East. Although China was mildly affected, some cities had housing crisis and some firms defaulted.

The true downturn happened last year when all these pairs fell into the negative zone. That says, both domestic demand (RS-IP) and external demand (EX-MI) were weak, credit was stuck despite money had been strong (M2-M0), thereby firms were unable to pass through costs to buyers (CPI-PPI). These are not easy to turnaround because for each of these pairs only one variable is under control: retail sales (RS) and M2 are market determined which are not easy to boost, while imports (IM) and PPI are externally driven which are even harder to manipulate.

The only better-looking pair from the chart is exports-imports growth gap. Nevertheless, this is not because of strong external demand but weak domestic demand (from overseas): both eased yet imports slowed down much faster to zero than exports. With lockdown measures partly removed, imports growth might pick up which means the gap will dip below zero again. By then, all pairs will reappear in the contraction zone. Regardless of the high growth rate of each individual series compared to other countries, the scissors are telling the ugly truth.

Deleveraging is painful in nature. The worst is when this happens when most countries are monetary tightening at a speed not seen for decades. If easing against the wind, Japan has demonstrated with their currency value depreciating by a quarter. If not, deleveraging will bound to be highly painful.