Companies buying back their own shares is now one of the biggest sources of demand for stocks, helping propel the S&P 500 to new record highs.

Share buybacks are the low-hanging fruit for management, although signs point to a decreasing bang for the buck.

“In a way it’s catnip for management teams,” said RBC Wealth Management’s Alan Robinson in an interview. “They see the direct relationship. It’s a quick way of supporting the share price by reducing the float [amount of shares outstanding].”

Robinson adds that as long as the stock’s performance is a factor in management’s compensation, then buybacks will be a major component in a company’s capital allocation.

It is also easier to see the benefits of share buybacks as opposed to long-term capital spending. While companies have also increased capex—or brought forward business investment intentions given the tax breaks—the benefits tend not to show up for years, potentially. A widely held criticism of the management of companies and their incentive structure is the de facto short-term focus.

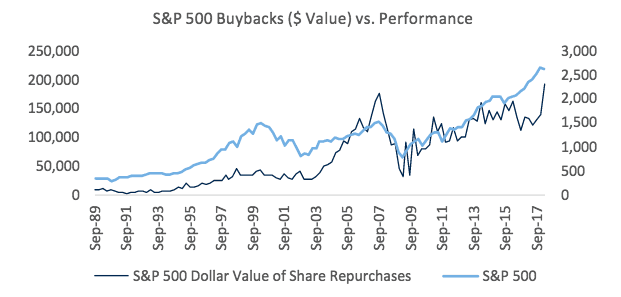

As companies buy back their stock at record-high prices, the marginal impact on the share price decreases. Even with a record dollar volume of share buybacks, the buyback yield (total repurchases relative to total stock outstanding) has been more subdued.

“In a way, share buybacks have been a victim of their own success,” Robinson said.

A reason for the slowdown in share buybacks relative to market capitalization is that management is becoming more cautious in its expectations of earnings, cash flow growth, and ease of obtaining funding, according to Robinson.

More Fuel

In principle, share repurchases send the same signal to shareholders as does a cash dividend: The company does not have sufficient reinvestment opportunities for the amount of cash flow generated. It could also indicate that management thinks its shares are undervalued and wants to send a message to the market, which some companies did after the October 1987 crash.Share buybacks are also more flexible than cash dividends as they are not a long-term commitment. A company does not want to reduce its cash dividend once it has made a commitment, as it tends to signal the company faces difficulties.

The tech sector accounts for 40 percent of buybacks—Apple became the world’s first $1 trillion company, aided by buybacks of $21 billion, which have boosted earnings per share by 40 percent, according to Goldman. Tech has also been one of the best-performing sectors of the S&P 500.

Invesco believes $1.5 trillion will return to the United States, as the tax rate has been cut from 35 percent to 15.5 percent for a one-time repatriation of offshore cash.

“We believe the repatriation tax will incentivize companies to use their own overseas cash to fund buybacks and M&A in place of debt issuance,” according to Invesco.

And while mergers and acquisitions are getting done, they are a lot more difficult for management to pull off successfully than buying back their shares. Paying a premium to acquire an already fully valued company needs strong justification and may even require regulatory approval.

Significant potential demand remains for stocks as firms complete their existing buyback programs, according to Goldman.

As a portfolio manager, Robinson is focused on what happens once M&A cools down. The question then becomes: Does that money get put to work in stock buybacks?

“That might be the next leg ahead in terms of share repurchases,” he said. “For that to happen near the end of the [bull market] cycle will be the last hurrah, but we’re not there just yet.”