The Consumer Price Index (CPI) is an attempt to measure an overall increase in prices across time. The calculation runs into a variety of problems including issues with product substitution, rural vs urban consumption, and innovation. The last item shows how difficult it is to calculate an inflation number when prices for items like cars, televisions, and computers might be similar to what they were many years ago, but the newer models have better performance and improved features. If you pay the same amount for a better product, the CPI doesn’t reflect that.

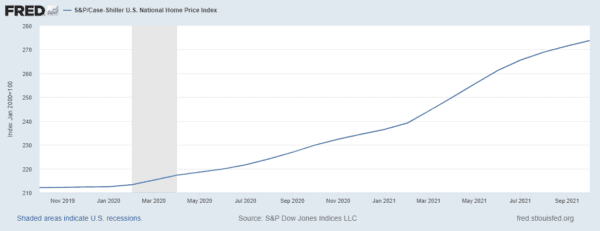

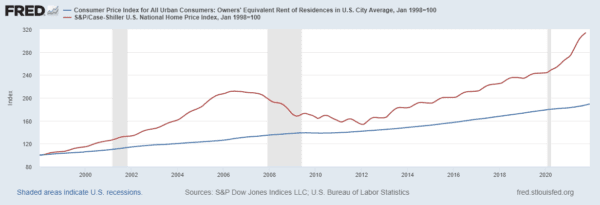

So, housing costs went up 19 percent and the official CPI says 4 percent. That shouldn’t be possible. What’s happening is due to a sneaky change made to the CPI in 1998 when the shelter cost for homeowners was changed to “owners’ equivalent rent.” That means that homeowners were asked to estimate what someone would pay to rent their homes. Largely because homeowners rarely buy houses and even more rarely rent them, people tend to underestimate what it would cost to rent in their neighborhood. Since the change in methodology was put in place 24 years ago, owners’ equivalent rent has trailed actual housing prices by 67 percent.

Last week, we covered how quantitative easing and low interest rates are the root cause of the inflation we’re experiencing now. Last month, Federal Reserve Chairman Jerome Powell said he was going to wind down quantitative easing over the next few months and start to raise interest rates in 2022. With the Federal Funds rate currently at 0 percent and the official CPI at 7.1 percent, that means that real interest rates are currently negative 7.1 percent. We have a huge negative real interest rate, inflation at a multi-decade high, and systematic underreporting of inflation, and as of right now, the Federal Reserve is still increasing the liquidity in the system. Said plainly, they’re still doing more of the thing that’s causing the problem. The market is acting like Powell just insisted that everyone eat their broccoli, while he’s actually still handing out candy like it’s Halloween.

Even though the Fed has stopped using the word transitory to describe inflation, it’s clear they expect it to moderate later in 2022. Powell is in a tough spot. Inflation is crushing the savings of the people who have managed their finances carefully, and it is a danger to the standard of living of anyone on a fixed income or who isn’t affluent. In order to mitigate that problem, Powell is going to need to raise interest rates aggressively. If he does so, the stock market will likely take a hit. He’s trying to balance the stereotypical conflict between Wall Street and Main Street, but someone is going to get the worse end of this. As of now, he’s letting inflation rise quickly and protecting the stock market.

A lot of Americans are anxious right now about the state of their finances, the ability to maintain their standard of living, and about their savings and investment portfolios. Next week, we’ll address a list of things that people at every level of income and wealth can do to better protect themselves and their investments from both higher inflation, and the coming higher interest rates.