The U.S. economy is currently experiencing the hottest real estate market on record, the latest Realtor.com housing data show.

The most recent S&P/Case-Shiller U.S. National Home Price Index data show a sizzling real estate market, too.

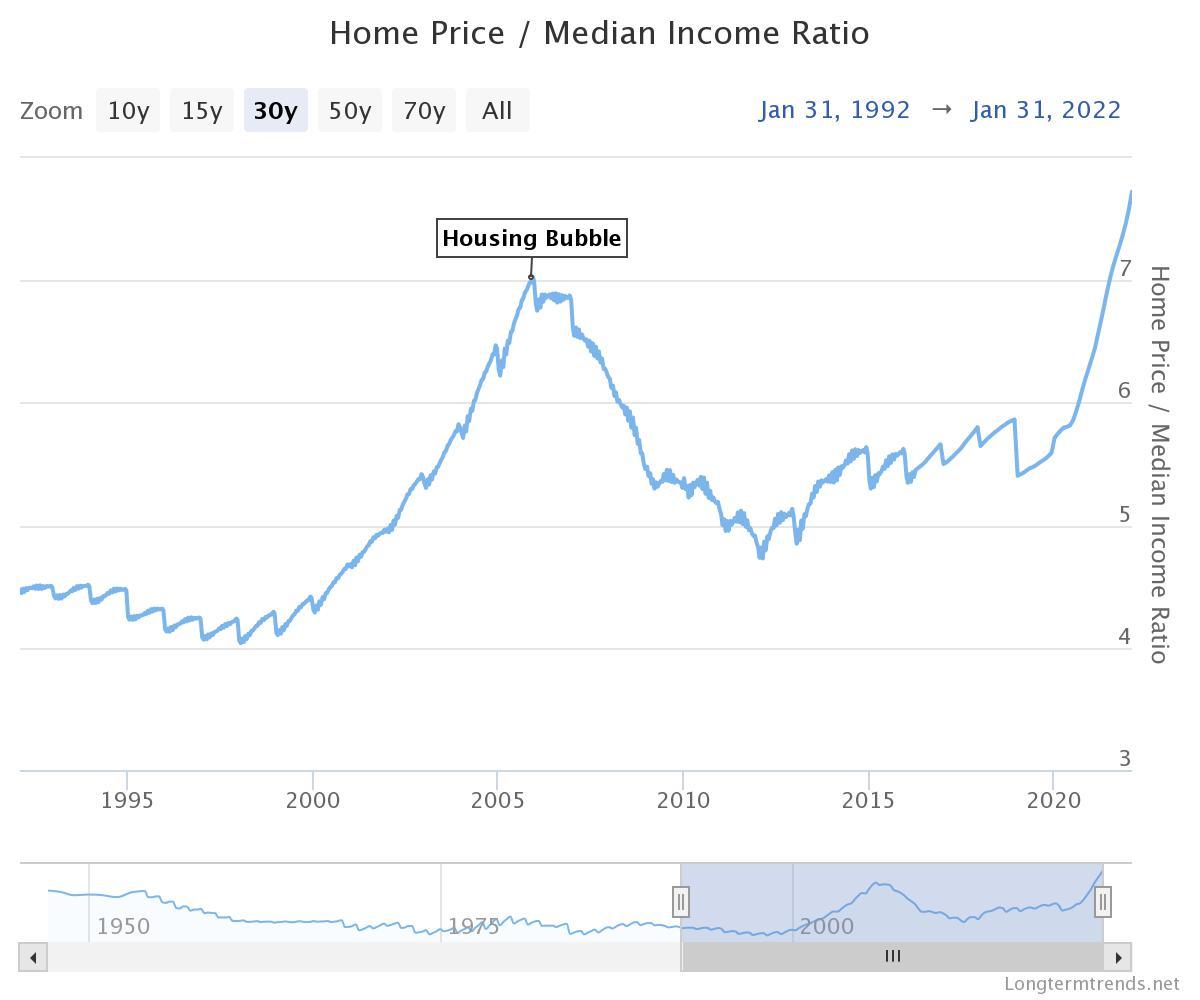

A Market Bubble or Long-Term Trend?

Over the last decade, the median household income increased around 11 percent and median home prices soared 30 percent, according to CNBC. Since 1965, average home values have skyrocketed 118 percent, while the median household income has gone up only 15 percent.Rising mortgage rates could also start playing a significant role in the housing market.

This upward trend in mortgage rates is pricing many prospective homeowners out of the market, says Nik Shah, the CEO of Home LLC, a down payment assistance provider for homebuyers.

“In late 2020, the typical U.S. resident could afford to buy a home worth 48 percent more than the median-priced home in the country,” Shah told The Epoch Times. “In 2022, thanks to rising mortgage rates and home prices, that’s reduced to only 5 percent.”

Despite concerns about higher mortgage rates impacting the pandemic-era housing boom, rising rates will only affect new entrants in the real estate market, says Morgan Stanley.

“The mortgage market is mostly fixed-rate, so raising rates won’t raise the monthly payment on current owners, but instead will disproportionately impact first-time homebuyers,” bank researchers said in a recent research note. “Robust mortgage underwriting should keep foreclosures limited, preventing the forced selling that would weigh on home prices.”

But if more people are being priced out of the real estate market, will sales volumes and prices start to respond by falling?

According to Kunal Sawhney, the CEO of Kalkine Group, an independent equities research firm, thinks “a substantial shift might be just around the corner.”

“But this shift may not be as detrimental to housing assets’ prices as some pundits have been forecasting for over the past many months,” Sawhney told The Epoch Times. “Neither a large-scale correction nor a major crash can be expected in the market in the near-to-medium term.”

However, the research analysts at the regional central bank do not believe a correction would be similar to the last housing bubble from more than a decade ago, citing better household finances and modest borrowing levels to purchase homes.

Looking ahead, home price appreciation should “decelerate,” the Morgan Stanley analysts added.

Shah agrees, adding that “there’s little to no chance of them going down” because of record low housing inventory and “pent-up millennial demand waiting to snap up homes at the first possible opportunity.”