This copy is for your personal, non-commercial use only. Distribution and use of this material are governed by our Subscriber Agreement and by copyright law. For non-personal use or to order multiple copies, please contact The Epoch Times Reprints.

NEW YORK—GDP printed at -0.9 percent this morning, 1.4 percentage points worse than market expectations of +0.5 percent. We had estimated the GDP to print up between nil to 0.5 percent up in our June Jobs Report. We attribute the “miss” to a continuing anomaly from the ports being cleared, discussed more below.

The Bureau of Economic Analysis (BEA) print met the generally accepted definition of a technical recession, which most analysts accept as two consecutive quarters of negative growth. (The Biden White House had tried to spin the definition last week in a frankly embarrassing—and gravely misguided—preemptive attempt to redefine recession. Two consecutive quarters of negative growth have been treated as “recession” since at least 1947.) The combination of recession and inflation causes us to be back to “stagflation,” a portmanteau of “stagnation” and “inflation.” We have not seen “stagflation” since it was ushered in by the Carter Administration back in the late 1970s.

The Data Charts

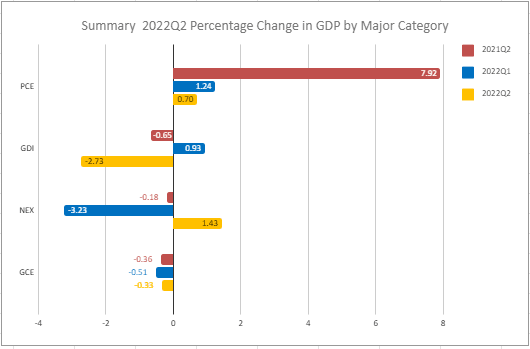

Summary GDP Percentage Point Change by Major Category (2021Q2, 2022Q1, and 2022Q2) The Stuyvesant Square Consultancy from BEA Data

Personal Consumption Expenditures (PCE) printed mildly up at 0.70 percent, as did Net Exports (NEX). Government Consumption Expenditures (GCE) printed slightly down.

But the biggest element of today’s disappointing GDP result was the negative print in Gross Domestic Investment (GDI), which printed down 2.73 percent. That decline was overwhelmingly comprised of a decline of 2.01 percentage points in Changes in Private Inventories (CPI) and a decline of 0.72 percent in Fixed Domestic Investment (FDI).

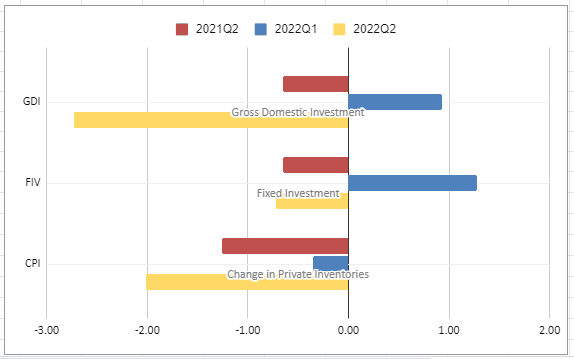

Gross Domestic Investment Percentage Point Change (2021Q2, 2022Q1, and 2022Q2) The Stuyvesant Square Consultancy from BEA Data

The first quarter of 2022, or 2022Q1, GDP printed down 1.6 percent, which we attributed to imports clearing the ports that had been backlogged, as discussed in our 2022Q1 GDP report. It stands to reason, then, and it is our operating thesis, that non-farm private inventories declined 1.96 percentage points largely because those inventories that had been back ordered filled store shelves after clearing U.S. ports in 2022Q1. Thus, further investments were not required in 2022Q2 and declined substantially. (Farm inventories dropped 0.5 percentage points, so that the total decline is the 2.01 percent shown in the chart.)

We will know more about this operating thesis about imports and inventories when 2022Q3 prints on October 27th. It is largely why our GDP estimate was off, at its worst, by the same amount as the consensus estimate. Assuming our thesis holds true, and that the net exports decline in 2022Q1 offsets our inventory decline in 2022Q2, we would hope this anomaly would normalize in 2022Q3.

Federal Reserve Meeting

Today’s GDP print comes the day after the Federal Reserve (“the Fed”) raised rates three-quarters of a percentage point, or 75 basis points (bps), thus making the rate on federal funds 2.5 to 2.75 percent. The market rallied yesterday on the Fed rate increase, with the Dow Jones closing up 1.37 percent to 32,197.59. The broader index was up even more, 2.62 percent, and the NASDAQ up 4.06 percent. (Markets were largely flat, in percentage terms, after the GDP print this morning.)

The markets seem to be sensing that the Fed will pivot, first to lower increases 50 or 25 bps and then, eventually, lower rates again. Our view is such a sentiment is hope over experience. Barring political considerations (which can never be discounted in the purportedly “independent” Fed) we believe the central bank will continue hikes until we return to a normalizing economy and a return to r* (r-star), the natural rate of interest, plus at least 100 basis points. We believe the “burn-off” of the Fed balance sheet that commenced in June and that will accelerate to $95 billion in September, barring unforeseen circumstances, will tighten markets and put the financial markets and the economy into further decline. Especially hard hit will be multinational companies with extensive foreign markets and translation risks. (We saw that already with some of the reporting earlier this month.)

We think there is a 7 in 10 chance of the recession continuing into 2022Q3 and Q4. The odds that it will be deep and long are, for now, 4 in 10. We are, however, troubled by the prospect of so-called “zombie” loans arising from the Fed’s low-interest rates since 2008. Most of those concerns are around commercial real estate construction and purchase loans. We project that office buildings in a newly evolved remote work economy will be difficult to fill and that many of the construction and purchase mortgages used to build or acquire such properties will default. That, in turn, will result in an additional and more severe slowdown, particularly in the regional banking sector.

An interesting aspect of the GDP report that is little noticed and rarely reported is the print of Gross Domestic Income, which the Fed describes as: “an alternative way of measuring the nation’s economy, by counting the incomes earned and costs incurred in production. In theory, GDI should equal gross domestic product, but the different source data yield different results.”

GDI printed up 2.5 percent in 2022Q1 versus a GDP decline of 1.6 percent. We think that the import/inventory anomaly may be the distinguishing factor, which makes us a bit more optimistic than most.

Looking Forward

We think 2022Q3 GDP will print in the range of -0.5 to +0.5 percent, based on the aforementioned thesis. We revise our forecast in our monthly jobs reports and, when necessary, our @stuysquare Twitter feed if and as exigent circumstances warrant.

There are numerous grey or black swans on the horizon that should concern investors. The most obvious is the Ukraine War spinning further out of control. China is at risk of widespread public rebellion in its westernmost provinces as would-be homeowners see their deposits lost by over-leveraged Chinese developers. The CCP has also made belligerent statements about House Speaker Nancy Pelosi’s planned visit to Taiwan and could use it as a pretext for imposing the Taiwan Strait blockade which has concerned us for some time. North Korea’s Kim Jung Un is making belligerent statements as well.

Any one of these off-white “swans” could markedly alter the outlook for the economy, as could a new virulent variant of the CCP virus, commonly referenced as “COVID 19.”

DISCLOSURE: The views expressed, including the outcome of future events, are the opinions of the firm and its management only as of July 28, 2022, and will not be revised for events after this document is submitted to The Epoch Times editors for publication. Statements herein do not represent, and should not be considered to be, investment advice. You should not use this article for that purpose. This article includes forward looking statements as to future events that may or may not develop as the writer opines. Before making any investment decision you should consult your own investment, business, legal, tax, and financial advisers. We associate with principals of TechnoMetrica on survey work in some elements of our business.

Note: Our commentaries most often tend to be event-driven. They are mostly written from a public policy, economic, or political/geopolitical perspective. Some are written from a management consulting perspective for companies that we believe to be under-performing and include strategies that we would recommend were the companies our clients.

J.G. Collins is managing director of the Stuyvesant Square Consultancy, a strategic advisory, market survey, and consulting firm in New York. His writings on economics, trade, politics, and public policy have appeared in Forbes, the New York Post, Crain’s New York Business, The Hill, The American Conservative, and other publications.