This copy is for your personal, non-commercial use only. Distribution and use of this material are governed by our Subscriber Agreement and by copyright law. For non-personal use or to order multiple copies, please contact The Epoch Times Reprints.

June jobs printed at 372,000 new jobs, well above the consensus estimate of 268,000. The unemployment rate was 3.6 percent, unchanged from last month, but down from last June’s 5.9 percent. The labor force participation rate was 62.2 percent, up from the 61.6 percent that printed in June 2021, but down 10 basis points (bps, defined as 1/100th of a percentage point) from last month.

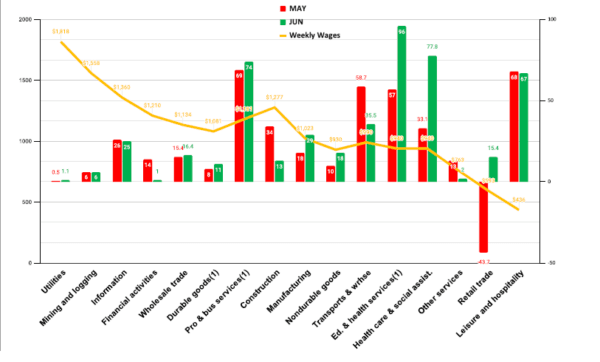

The most jobs were gained in Education and Health Services at 96,000 (which includes Health Care and Social Assistance job of 77,800), which tend to be government supported, followed by professional and business services. See the chart below.

June Jobs by Average Weekly Wages from June 2022 BLS Data. Copyright 2022, The Stuyvesant Square Consultancy

April and May jobs were revised downward by 74,000 net jobs. The U-6 Unemployment Rate, which measures total unemployed, plus all persons marginally attached to the labor force, plus total employed part-time for economic reasons, ticked down to 6.7 percent from 7.1 percent last month, and down from 9.8 percent last year.

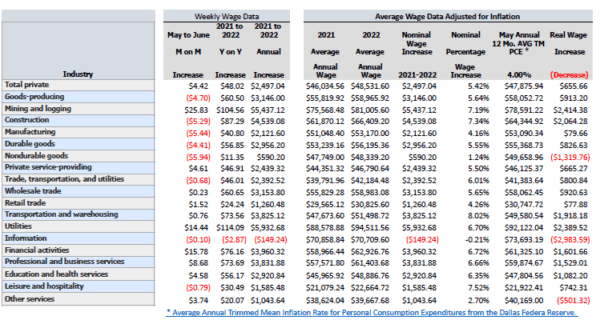

Real wages, which we define as annualized average weekly wages minus the 12-month average trimmed mean inflation rate for personal consumption expenditures, for May (the latest available data), currently 4.0 percent, were mixed. The mining and logging sectors showed the biggest annualized real wage gains, while workers in the information sector again showed the greatest annualized real wage losses, as they did last month. See the real wage data below. We report this data at the end of each quarter.

Real Wage Data by Major Categories of Employment. The Stuyvesant Square Consultancy

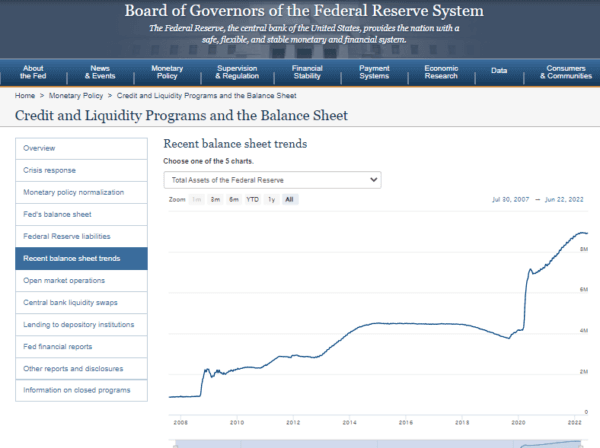

Federal Reserve Balance Sheet

We’ve said since the specter of inflation first appeared that the biggest issue is too much money in the economy. We have urged for quite some time that the Federal Reserve, or “Fed,” reduce its balance sheet. That has started, but just two weeks ago (June 15), and only slightly, by allowing maturing instruments to “burn off.” The reduction can be seen from the very slight downward curve at the top rightmost portion of this chart:

Federal Reserve Balance Sheet.

Selling the Treasurys and Mortgage-Backed Securities the Fed acquired in the pandemic to stimulate the economy would “soak up” the excess cash in the economy and raise long-term rates and slow the economy. The Fed has not done that and, consequently, we’re seeing the yield curve invert.

Yields on Treasurys change daily. The graph of their yield over time is called the yield curve. Most of the time, there is a spread in rates between the shorter-term rates and the longer-term rates. The Fed’s traditional tools—the ones that make the most headlines—generally affect only short-term interest rates. Longer-term rates are harder to control and doing so requires the Fed to engage in more extraordinary, rarely used, measures from its toolbox. One of those tools is called “Yield Curve Control”—controlling long-term rates by buying and selling Treasurys. The Fed has not used that tool and now market forces have caused the 2-year rate to exceed the 10-year interest rate twice; first in April and again this week.

When the rate for the short-term Treasurys exceeds the longer-term rates, the yield curve is said to “invert.” And an inverted yield curve almost always signals a recession or depression within two years. The reason a recession follows is that businesses put their money into Treasurys, thereby reducing the overall yield, instead of investing in businesses.

This chart below shows the spread between the rates on the 2 Year and 10 Year Treasurys. As you can see, the difference is now zero to negative, as it was in April. (At this writing at 9:00 a.m. on July 8th, the 2-year yield is 3.1191 percent, the 10-year 3.078 percent.)

Difference in Interest Rates between the 2 Year and 10 Year Treasurys over time. Federal Reserve Bank of St. Louis

Other Data

The Institute for Supply Management’s print of the Manufacturers Purchasing Managers’ Index, the Manufacturing PMI,® registered growth in June at 53.0, down 3.1 from May. A reading above 50 signals growth, with a notable contraction in new orders, which had been growing in May.

The Job Openings and Labor Turnover Survey (JOLTS) fell slightly in May, the latest available data, with job openings falling by 427,000. Most troublesome was the 2022 Q1 labor productivity (pdf), which dropped to the lowest level since 1947. As a consequence, unit labor costs increased 12.6 percent.

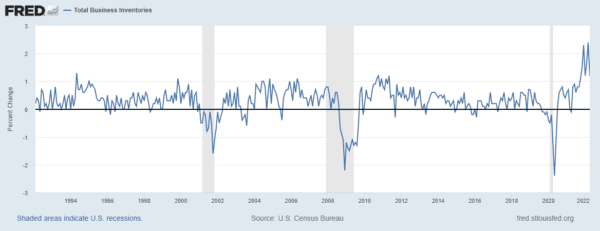

Another signal of the coming—and severe—recession is the percentage change in business inventories, now at their highest since records were kept. Inventories are simply not moving, presumably because consumers are hoarding cash on the expectation of a recession and also for fear of the cost of fuels.

Total business inventories. Federal Reserve Bank of St. Louis

Inflation appears to be affecting household debt levels, as we are seeing household debt service payments as a percent of disposable personal income increase by over 110 basis points (1.1 percent) since the beginning of the year.

Housing starts (pdf) slowed by 14.4 percent in May, the latest available data, on rising interest rates.

Real personal income declined by 0.1 percent as did personal consumption expenditures, by 0.4 percent.

The Atlanta Fed estimate of GDP Now shows a decline in 2022Q2 GDP of around 2 percent. If that plays out when the figures are released July 28th, the United States will fall within the technical definition of a recession; that is, two consecutive quarters of negative GDP.

We’re agnostic as to a recession because we believe that the second quarter will print low, but not negative, at least in the first estimate. It is best described as a “jump ball” as to whether we will be in a technical recession. Nevertheless, we believe the first half of 2022 will print negative, taken on the average of the first two quarters.

Inflation is currently printing at 8.6 percent, unadjusted, for the year. Depending on the inflation release we will see July 13th, we expect the Fed may target rates up a full percentage point in their July 26th/27th meeting. (This seems unlikely, though, because the Fed members economic projections won’t be released again until September.) We anticipate inflati0n—particularly in food and energy—to continue at high single or double digits because of the fertilizer shortages we wrote about here. We also are seeing food shortages from the Ukraine War and agricultural strikes in The Netherlands and other countries in Europe.

We’re expecting a mild recession to be declared with the fourth quarter and for 2022Q2 to print between nil and 0.5 percent growth. We look for a deeper recession in the first half of 2023.

We see very few investment opportunities and suggest mostly the best choice is cash or TIPS, Treasury Inflation Protected Securities. Holders of Fortune 100 securities should hold them, but place stop loss orders, especially if you are approaching or in retirement and need to protect your portfolio from big losses.

_____________________________________________________

DISCLOSURE: The views expressed, including the outcome of future events, are the opinions of the firm and its management only as of July 8, 2022, and will not be revised for events after this document is submitted to The Epoch Times editors for publication. Statements herein do not represent, and should not be considered to be, investment advice. You should not use this article for that purpose. This article includes forward looking statements as to future events that may or may not develop as the writer opines. Before making any investment decision you should consult your own investment, business, legal, tax, and financial advisers. We associate with principals of TechnoMetrica on survey work in some elements of our business.

Note: Our commentaries most often tend to be event-driven. They are mostly written from a public policy, economic, or political/geopolitical perspective. Some are written from a management consulting perspective for companies that we believe to be under-performing and include strategies that we would recommend were the companies our clients.

J.G. Collins is managing director of the Stuyvesant Square Consultancy, a strategic advisory, market survey, and consulting firm in New York. His writings on economics, trade, politics, and public policy have appeared in Forbes, the New York Post, Crain’s New York Business, The Hill, The American Conservative, and other publications.