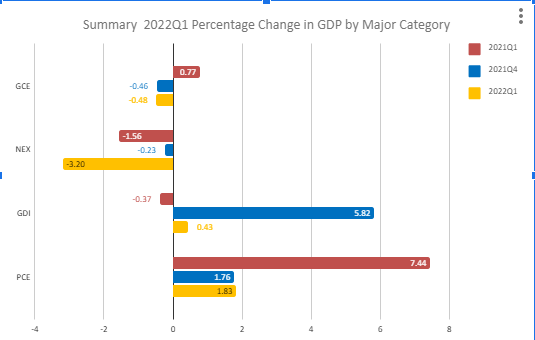

- Topline GDP printed down 1.4 percent versus a consensus estimate of 1.1 percent up.

- Personal consumption expenditures (PCE) were sharply lower, year-on-year, as the economy normalizes

- The backlog of container ships that stood offshore at the end of last year has largely been cleared, and the U.S. has imported more oil and gas at higher prices, having a negative effect on the net exports (NEX) component of GDP and pushing the entire GDP print negative.

- Given that anomaly, the Federal Reserve is still likely to push rates higher when it meets May 4-6.

- Gross domestic investment (GDI) dropped as rates increased and concerns about business conditions increase.

DATA SUMMARY

This morning’s print of 2022 first quarter GDP (2022Q1) largely disappointed observers, including us, who had anticipated a higher print. (We had anticipated a print of 1 to 1.5 percent in our jobs report at the beginning of the month.)PCE, the traditional driver of GDP, dropped considerably from the comparable quarter last year, but was up slightly from last quarter.

SOURCE: The Stuyvesant Square Consultancy © from Bureau of Economic Analysis Data