While the U.S. year-on-year inflation is declining, inflation in the Eurozone is still not under control. Why is that so?

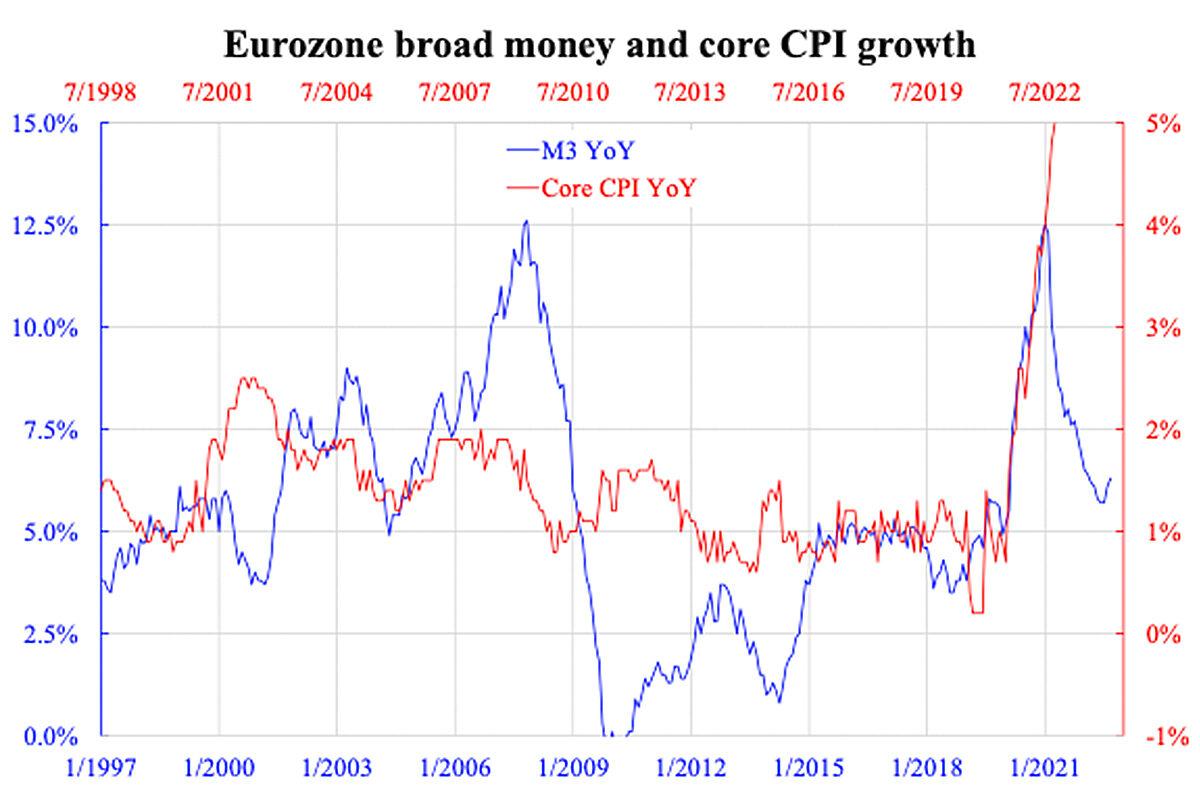

However, if the same exercise is repeated in Eurozone, another major economic system, something different is observed. Even assuming a longer time lag of six quarters, the money growth that peaked in early 2021 did not lead to a fall in inflation; this was also true for core inflation. As the accompanying chart shows, core inflation surged to five percent instead of following the phase-lead money growth decline. This suggests there are factors other than monetary in play. Monetary factors generally govern the demand side; is the supply side still tight?

The supply side being tight is logically possible, but other aspects of data seem not to confirm this. For example, the Baltic dry index, which reflects the tightness of shipment, is now near the lowest level since the pandemic outburst. The Dutch natural gas price also vapourised all upside from June to August and is now back near the pre-war level. Also, the price of most resources peaked soon after the Russia-Ukraine war broke out, so the supply-side argument did not apply over the past few months. How, then, can we explain such a core inflation surge with neither demand nor supply factors?

Examining the components of inflation, energy is no doubt the main driver giving almost 42 percent of inflation. But the non-energy industrial goods inflation also stood at six percent, while services accounted for 4.4 percent. The latter two are presumably mostly unrelated to the supply side, yet both are very high. This suggests inflation is evenly spread to most sectors. Further examining the member countries of the Euro area, all have the latest core inflation readings of 4.x percent to double-digit, suggesting inflation is also evenly spread across countries, a higher-level spatial dimension than domestic sectors.

Clearly, non-core inflation (mainly tobacco, food, and energy) has generated the so-called “second-round effect” of core inflation. The latest measure of inflation expectations for these items does not reflect this but shows low numbers, yet, overall inflation is chasing the current inflation reading. If inflation expectations are still well anchored at the same level, then the only remaining reason for inflation rise is the central bank not doing enough. While the U.S. is having lower core inflation than the Euro area now, the policy rate doubled (the U.S. is near 4 percent, Euro area is at 2 percent). The two central banks did a natural experiment.

Despite the latest Euro area unemployment rate being 6.6 percent, it is already a record low since data began in 1998. Wage growth edged up from the pre-COVID-19 trend level of 1.6 percent to now 4.1 percent. All this points to an overheated economy without appropriate tightening—a true reason inflation is still surging.