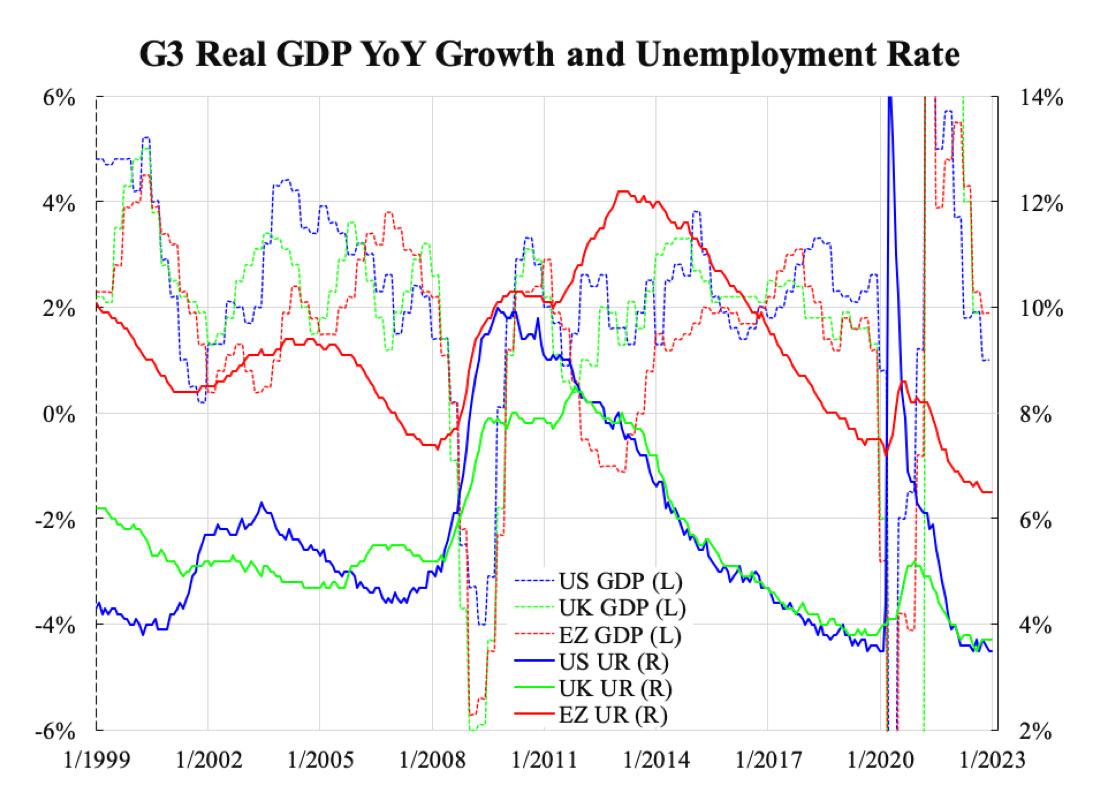

There has been a rooted impression that the economic performance in Europe is always worse than that in the United States. This is not true. The measuring period for GDP released by the U.S. is quarter-over-quarter (QoQ), while those in other places are usually year-over-year (YoY). If both are reported in YoY for comparison, the numbers for 2022 Q1 to Q4 in the U.S. were 3.7 percent, 1.8 percent, 1.9 percent, and 1.1 percent, respectively, while those in the Eurozone were 5.5 percent, 4.3 percent, 2.3 percent, and 1.9 percent. The Eurozone numbers are higher than those of the U.S. in every quarter. Even if the Eurozone is replaced by the UK, the UK is no worse than the U.S.

If comparing the average GDP growth rates among these places since the birth of the Euro in 1999 to the latest, Eurozone is the worst at 1.4 percent, which is lower than UK’s 1.7 percent and 2.2 percent in the United States. But if exceptional quarters like the financial tsunami in 2008/09, the European debt crisis in 2012/13, and COVID in 2020/21 are excluded, then in normal times, the Eurozone, UK, and the U.S. averaged a much narrower range at 2.1 percent, 2.4 percent, and 2.6 percent respectively. Note that GDP growth has an intrinsic error of about 1 percent, such a 0.5 percent difference may not matter meaningfully (statistically insignificant).

By further counting, two-thirds of the time, the United States grew faster than the Eurozone, and the portion of time that the U.S. grew faster than the UK or the UK grew faster than the Eurozone is both about 60 percent. Neither of these three fractions is overwhelming, meaning that the three places may not perform very differently. Even if the cyclical ups and downs are observed, the timings of recession and recovery do not exhibit much difference—cycles are pretty synchronous. GDP growth is never a good indicator of cross-country differences, especially on cycles.

The fundamental difference is easier to see not from flow variables but from the stock ones. The latter kind includes those fractions like whatever-to-GDP ratios, or one common measure is the unemployment rate divided by the labor force. Eurozone has shown a consistently higher unemployment rate than the United States or UK, on average by 3-4 percent.

Fair to say that the Eurozone is comprised of extreme members. If only Germany and France—which together take up half of the Eurozone GDP—are concerned, then their average unemployment rates (both 7.8 percent) are just around 2 percent higher than the United States (5.8 percent) or UK ones (5.6 percent). Such differences might be attributed to the institution where capitalism is in the United States and UK while socialism is in Germany and France. A glance at the ups and downs demonstrates again that there is no difference in cyclical direction except for a slight phase lead/lag observed.

What data conclude is the difference lies more in the longer-run macro, which is the growth and development aspect, than shorter-run macro, which is concerned more with business cycles. International institutions or major banks highlighting any cross-country cycle differences may not be consistent with past data. This information is helpful in forecasting because one can always cross-check the consistency of outlook views among these countries.