Recently the market has been struggling between recession or no recession, and whether there will be a recession, sooner or later. By definition, recession refers to the period when economic activity runs from peak to trough, about its trend level. Although it takes quite some skills to separate the trend and cyclical components from a time series, laymen would be able to tell if economic activity is near its peak or if it has peaked.

Intuitively, from leading indicators like stock indexes refusing to advance to lagging indicators like the unemployment rate refusing to further improve, we know the peak is imminent.

Based on theory, the recession is a process that runs from excess demand to excess supply. The “excess” happens because it takes time to produce whereas demand can change instantly; this is the concept of “time to build.” The duration of such a process depends on the nature of production. If for general goods with short production periods, business cycles are generally shorter: recession happens usually once or twice every decade. But for durables like housing which take much longer to build, cycles are much longer which can be up to 15 to 25 years.

A normal business cycle recession may not involve a housing recession, but the converse is not true where housing recession generally leads to a business cycle recession, which is deeper and longer. Academic studies conclude for most countries, housing takes up some one-fifth to one-third of the overall economic activity. Moreover, according to Granger, the housing cycle causes the business cycle but not necessarily the other way round. Thus, if there is a housing recession ahead, we can almost surely tell that recession will not be anything mild or simple, but tough instead.

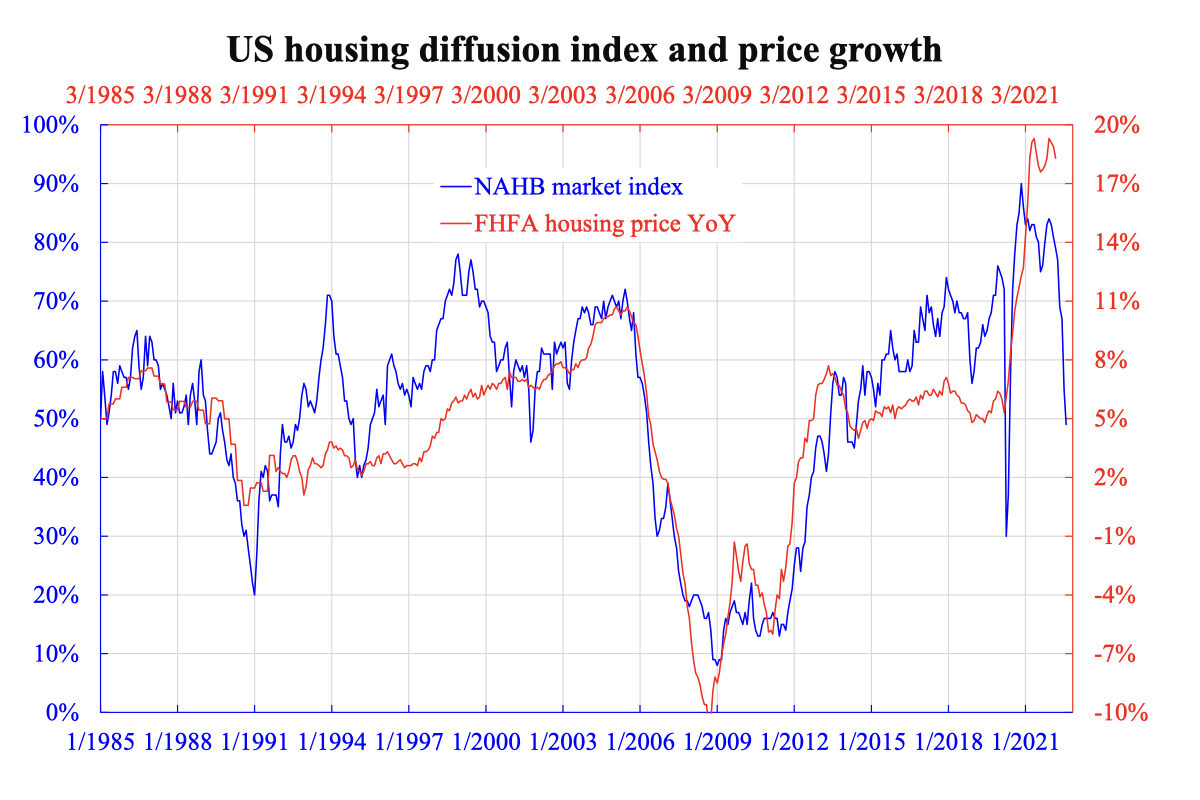

There are plenty of housing cycle indicators including the building and construction ones like housing starts or building permits, as well as the sales ones like new or existing home sales. All these figures have shown very bad trends in recent months. Another kind of indicator is a survey. The National Association of Home Builders (NAHB) has a market index surveying the ratio of bullish to bearish. From the accompanying chart, one can see that this index is very effective in foreseeing the housing price year-over-year (YoY) growth about two months ahead.

It is projected that the housing price YoY growth will fall from the top of 20 percent to a mid to low single digit. This is not the end of the story, however, because the rate hike is probably only half to two-thirds done. There will be another one percent to two percent more hike to go. More importantly, the rate hike will have a delayed effect which extends to cover the whole of 2023 and probably 2024. Added that housing price has high momentum (i.e., a very long autoregressive (AR) process), the snowball effect of housing price decline is not easy to stop once it has been kicked off.

All the above will be irrelevant if a recession is not going to happen, but this seems unlikely as the yield curve gets inverted. Most analysts still have underestimated the upcoming recession.