NEW YORK—The U.S. Treasuries market took investors on a bumpy ride in 2020, with yields plunging to historic lows in the early part of the year before a partial grind back in the second half.

Investors are looking for yields to edge up further as the calendar flips to 2021.

Expectations that a vaccine against COVID-19 will spur an economic rebound in 2021 have pushed some investors out of Treasuries and other safe-haven assets in recent months and helped lift yields, which move inversely to bond prices, near their post-pandemic highs just under 1 percent. Still, they are well off the levels seen at the beginning of the year, when benchmark 10-year Treasuries yielded closer to 2 percent.

The post-pandemic drop in Treasury yields, spurred by unprecedented U.S. Federal Reserve support, had wide-ranging repercussions, forcing investors to rethink the role of bonds as a hedge against stock gyrations and spurring a scramble for yield across markets. Prices for gold, which often struggles to compete with yield-bearing investments, are up about 24 percent year-to-date, its best year in a decade.

“The renewed hunt for yield means investors need to take a look at the role of ... bonds in portfolios,” analysts at UBS wrote in a report.

Few investors believe Treasury yields are going back to their pre-COVID-19 levels anytime soon. The median forecast by strategists in the latest Reuters poll on where Treasury yields will stand in 12 months was 1.2 percent.

Among the factors that could influence yields are how quickly vaccines can be rolled out across the United States and the results of the Jan. 5 Georgia Senate run-off, which could tip control of the chamber to Democrats.

If history’s any guide, though, yields could end up considerably below current forecasts: analysts’ projections have tended to overestimate where yields will be in a year’s time.

One catalyst for a rally in longer-dated bond yields could be a potential rise in U.S. inflation—a factor that could cause investors to sell longer-dated bonds, as inflation erodes their value over time.

Although inflation has in the last decade consistently averaged below the 2 percent target set by the Federal Reserve, trillions of dollars in government spending and the central bank’s pledge to allow periods of higher consumer prices have revived discussions of its return.

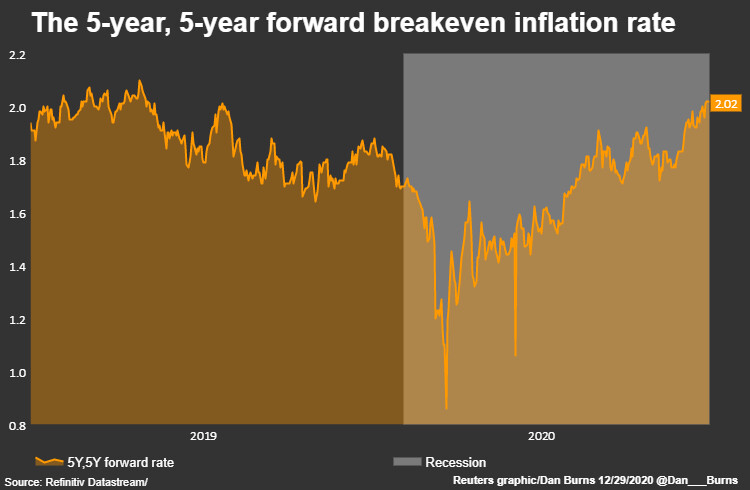

One measure of inflation, which tracks the expected average inflation rate over the five-year period starting five years from now, is at 2.02 percent, the highest since May 2019. The latest survey by BofA Global Research, meanwhile, showed fund managers see a rise in inflation as the market’s second-biggest “tail risk.”

Demand for inflation-protected bonds has risen, with the yield on 10-year TIPS around negative 1 percent.

Analysts at Deutsche Bank said in a note earlier in December that there should be healthy appetite for more Treasuries next year, if the Fed stays supportive. Deutsche expects net coupon issuance for 2021 at $2.7 trillion, and with the Fed continuing purchases at its current rate that means the private sector needs to absorb $1.7 trillion.

Still, Treasury supply/demand could become “more imbalanced” in 2021, said Bank of America in a Dec. 11 note, with supply expected to reach record highs.

Investors are also keeping a close eye on whether the Fed will reconfigure its bond purchases to cap a potential rise in long-term yields.

Expectations of rising long-end yields have been reflected in the spread between two and 10-year Treasury yields, the most common measure of the yield curve, which has widened by nearly 12 basis points in December alone. Speculators have a sizeable bearish position in longer-dated Treasuries in the futures market.

For its part, the Fed has given little indication it is ready to adjust its mix of bond buying, with Chairman Jerome Powell saying earlier this month that for the time being, buying more long-dated debt was not “high on our list of possibilities.”