This copy is for your personal, non-commercial use only. Distribution and use of this material are governed by our Subscriber Agreement and by copyright law. For non-personal use or to order multiple copies, please contact The Epoch Times Reprints.

As Baby Boomers head into their “golden years,” financial analysts are asking what will become of the enormous wealth that this generation, the richest in American history, has amassed.

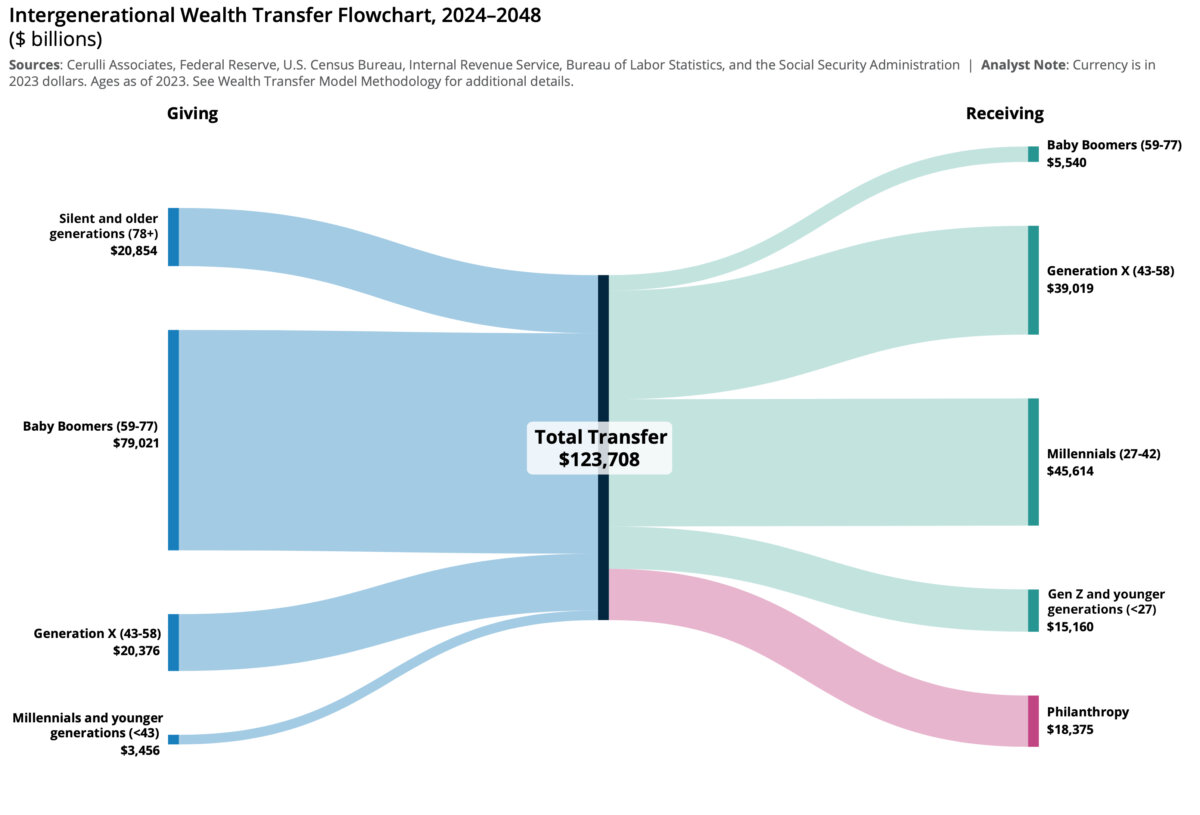

A 2024 report by Cerulli Associates Senior Analyst Chayce Horton deems it the Great Wealth Transfer and predicts that over the next two decades, approximately $124 trillion in assets could be passed down from Americans born before 1965. Of this, Horton projects that $105 trillion will go to heirs and $18 trillion will go to charity.

Bank of America Private Bank President Katy Knox likewise calls it “the greatest generational transfer of wealth in history” in a 2024 report, and the bank states that Boomers’ assets “are increasingly under new management.”

Americans’ net wealth hit a historic high in 2021 of 6.1 times U.S. GDP, according to Federal Reserve data, though this followed two years in which the government paid out more than $930 billion in COVID relief payments. Since then, it has fallen back to 5.6 times GDP, but remains significantly higher than levels between 3 and 4 times GDP between 1950 and 2000.

On the whole, Americans have become richer than ever, and nearly two-thirds of that wealth is currently in the hands of people over 60.

As of 2024, 52 percent of the total wealth in America was owned by Baby Boomers (born between 1945 and 1964), and an additional 13 percent was owned by the “Silent Generation” (born 1928 to 1945), according to Statista, a data analytics firm. Bank of America’s survey put that share even higher, with 72 percent of wealth being held by those two generations.

Many eyes are now turning to the spending and investment habits of Gen X, Millennials, and Gen Z, which Bank of America predicts will become “the largest and richest generation by 2035.”

What happens with these huge sums has sparked much speculation from financial analysts looking to predict where markets may be headed.

“Despite well-publicized fears that aging Boomers would move money out of stocks en masse as they reached retirement age, dragging down markets and investor returns, the fact is that the stock market has gone gangbusters in the past 15 years since Boomers began turning age 65,” Bankrate financial analyst Greg McBride told The Epoch Times. “The amount of money flowing in and out of capital markets on a daily or yearly basis swamps the amount of intergenerational wealth transfer in that same given timeframe.”

But now that Boomers are heading into their 70s and 80s, attention has turned to what their children and grandchildren will do with all the wealth that could be coming their way. Will the young invest in stocks, houses, bitcoin, or simply spend it?

Youth Prefer Higher Risk, Higher Return

“Our data does support this idea that younger investors, due to their longer time horizons and bias towards higher returns and equities—because of their formative experiences being in the last 15-plus years—are generally more interested in stocks, alternative investments, and cryptocurrencies,” Horton, author of the Cerulli study, told The Epoch Times. “As younger investors gain a greater share of wealth in the United States, there will continue to be growing demand for these aforementioned investment styles among young investors.”

The Bank of America survey found that younger investors had a particular interest in crypto, private equity, and real estate, and were more skeptical that a stock-and-bond portfolio alone would generate an adequate return.

“The past two years have seen more inflation than in decades, sharply rising interest rates, a bear-market year for stocks in 2022, a headline fraud case in the burgeoning crypto industry, two major geopolitical conflicts, and the meteoric rise of AI tools in everyday life,” the report states. Recent experiences with equity markets also include the bear market between 2000 and 2002 and a 50 percent fall in stock prices between 2008 and 2009.

This could spur younger investors to look beyond the more traditional portfolios of their elders, and to consider riskier or alternative investments to generate higher returns. If indeed younger investors have a higher propensity for risk-taking, that could spur growth and innovation, but also bring more volatility.

“Risk tolerance is essential to entrepreneurship and long-term wealth creation, and a younger generation embracing risk may drive future waves of invention and economic growth,” Peter Earle, an economist at the American Institute of Economic Research, told The Epoch Times.

“On one hand, money flowing out of conservative investments like value funds and investment grade bonds and into more speculative assets may spur innovation and fuel for high-growth enterprises,” he said. “The flip side, of course, is that this shift contemplates a higher likelihood of speculative excess and market correction, especially in assets like meme stocks or cryptocurrencies.”

Meme stocks are equities whose pricing is driven by the buzz they create on social media.

Others predict that the reputedly higher risk tolerance among the young will dissipate as they age.

“I think what you’re going to see is that these generations, just like all others, will migrate from being very aggressive in their investment and job opportunities, to being more and more conservative,” Ken Johnson, finance professor at the University of Mississippi, told The Epoch Times.

Predictions for Home Prices

However, real estate is one market where we could see a significant impact over time, Johnson said.

“Housing is, and will continue to be, less important in the portfolio of savers,” he said. Gen Z and Millennials will have access to many more investment options than any prior generation, which he calls the “democratization of investing.”

For older generations, buying a house was often the best way to build wealth because mortgages allowed them to leverage their income and imposed financial discipline in order to make the monthly payments. For younger generations, however, houses may be seen simply as a place to live rather than what has been for most Americans their largest single asset, according to Fed data.

“As the democratization of access to securitized equities and bonds increases, the importance of housing in wealth creation will decline,” Johnson said.

He predicts a shift in the coming decades toward smaller homes but with more amenities and high-tech features, including entertainment centers and home offices. A higher demand for lower-maintenance apartments over suburban homes is also likely, he says.

A large inheritance could help younger Americans afford a downpayment on a home, driving up demand and house prices, a report by Rohan Girvin published in the University of Michigan’s Journal of Economics states. But if the young have smaller families or are more inclined to live in cities, it could reduce the demand for large suburban homes and create a glut as they look to sell inherited properties.

Many analysts, however, caution against overstating the impact of this projected windfall.

“The great wealth transfer is something we expect to be ongoing for the next two decades and will not be happening all at once, so we think that changes in technology and attitudes towards allocations, product use, and alternative assets will be driven by factors outside of wealth transfer to a much greater degree than wealth transfer will drive those trends,” Horton said. “Additionally, because most inheritances are received at the time of death of a parent, those inheritances are often received by people in their 50s or 60s—and because of this, we see Gen X being the largest recipient of wealth transfer over the next 15 years.”

Inheritance Lost

Receiving a large inheritance is one thing, however. Holding on to it is another.

“A well-publicized study by a wealth consultancy noted that 70 percent of wealthy families lose their wealth by the second generation and 90 percent do so by the third generation,” McBride said. “While there is debate about those figures, regardless, it highlights a very real risk that families and financial firms need to actively plan for, beginning years in advance.”

This frequently cited study was conducted by Victor Preisser and Roy Williams, based on research into the legacies of 3,250 wealthy families, and published in the 2004 book, “Preparing Heirs: Five Steps to a Successful Transition of Family Wealth and Values.”

“Empirical evidence suggests that earned wealth is more often retained and grown, while inherited wealth is often spent or misallocated by second and third generations,” Earle said. “Inherited capital entering the hands of those with little investment experience may be consumed quickly on unwise or wasteful consumption, accelerating its dissipation.”

“Market economies reward competence and foresight, not entitlement,” he said. “So while transfers initially elevate passive recipients, those results are overwhelmingly temporary, with the long-term outcome depending on their ability to act as effective capital allocators.”

Boomers May Spend It

Many analysts question whether the Great Wealth Transfer will happen at all. Boomers may end up spending more of their money than they give away, according to Laurence Kotlikoff, professor of economics at Boston University.

“We don’t have any real evidence of altruism,” Kotlikoff told The Epoch Times.

“If you look at the average consumption by age, we see it going up for the elderly—compared to younger people—dramatically,” he said. “What the data show is that once the kids are adults, their parents consume as if they don’t have any kids.”

The average 70-year-old American is consuming about 60 percent more than the average 40-year-old today, he said, whereas in 1960, the average 70-year-old consumed about 40 percent less. In line with this data, a 2023 report in the Wall Street Journal found that Americans over 65, who comprised less than 18 percent of the population, accounted for 22 percent of the nation’s consumer spending that year, up from 15 percent in 2010.

In addition to leisure spending, Boomers are also facing much higher medical expenses, which could be the major factor consuming their savings.

“If you are like most Americans, health care is expected to be one of your largest expenses in retirement, after housing and transportation costs,” a 2024 investor report by Fidelity stated. “But unlike your parents’ generation, you won’t likely have access to employer- or union-sponsored retiree health benefits.”

Fidelity predicted that the average 65-year-old will likely need $165,000 in after-tax savings to cover health care expenses, up 5 percent from 2023.

“Boomers are living longer, and advanced age brings escalating healthcare costs, assisted living charges, and long-term care expenses,” Earle said. “Many Boomers, in the final years of their lives, may consume much of their accumulated wealth, leaving less or none to pass on.”