This copy is for your personal, non-commercial use only. Distribution and use of this material are governed by our Subscriber Agreement and by copyright law. For non-personal use or to order multiple copies, please contact The Epoch Times Reprints.

Federal Reserve Board Chairman Jerome Powell speaks during an interview by David Rubenstein, chairman of the Economic Club of Washington, D.C., on Feb. 7, 2023. Julia Nikhinson/Getty Images

As the Federal Reserve comes to a crossroads in its campaign to extinguish historically high inflation rates, Jerome Powell, its chairman, said that America’s central bank was “steering by the stars on a cloudy night.”

According to some economists, one obstacle obscuring the Fed’s view is the federal government itself. As the state extends its authority ever deeper into private markets, it is not only drowning out the information the Fed needs to set policies, it also is acting as a material drag on America’s ability to produce, regardless of how many trillions of dollars the Fed pumps into the economy.

“The dramatic expansion in government reflects the secular decline of the dollar and the U.S. economy,” Arthur Laffer, former economic advisor to presidents Ronald Reagan and Donald Trump, told The Epoch Times. “If the Fed saw the decline for what it is, it would be the first step to recovery.”

To see examples of this, the Fed need look no farther than its own home turf: the market for short-term interest rates.

Short-term interest rates, absent government intervention, should reflect an economy’s supply and demand for loans and credit at any given time. Economists denote this hypothetical rate as R* (“R star”), or the “neutral rate.”

“We don’t observe the neutral rate in the real world because the Fed is interfering with the market,” Thomas Hogan, senior research faculty at American Institute for Economic Research and former chief economist for the U.S. Senate Banking Committee, told The Epoch Times. “Powell is making a pun here, that because we don’t observe the neutral rate in the real world, we can’t see ‘R-star.’

“The Fed is now so involved with financial markets that they are distorting the market and making it difficult for the market to operate, but also difficult for them to get good signals from financial markets about the effects of their own policies,” Mr. Hogan said. “The Fed is playing such a large role in those markets that it’s difficult to tell what the market rate would be if the Fed weren’t interfering.”

Crowding Out the Private Sector

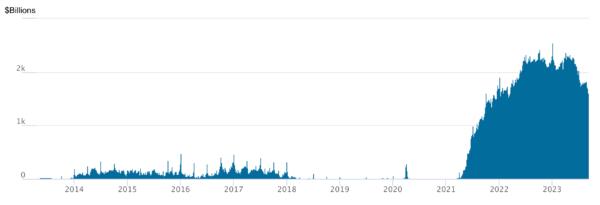

One of the markets for short-term investments is the reverse-repo market. The Fed was a minor player in this market until 2021 when its participation spiked from a few billion dollars, to more than $2 trillion.

Source: Federal Reserve / Fed's participation in the reverse-repo market, a short-term credit market

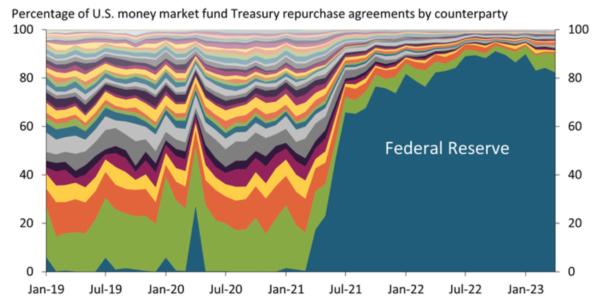

Prices and rates in this market had previously been set via arm’s-length trading by numerous counterparties. Over the past two years, however, the Fed grew from being a minor player to dominating more than 80 percent of the market.

Source: U.S. Securities and Exchange Commission; data assembled by Stefan A. Jacewitz, Federal Reserve / Crowding out the competition: the share of the Treasury repo market held by the Fed has increased dramatically since 2021

A January report by the Atlantic Council stated that “the persistently huge footprint of the Fed in private short-term financial transactions … reflects the preference of financial institutions and other companies to deal with the Fed rather than conducting businesses among themselves. This is an unhealthy development with largely negative implications for the U.S. financial system and economy going forward.

“If these trends continue, they will marginalize the role of private markets for short-term funds, weakening the usefulness of market price signals arising through the autonomous supply and demand for funds,” the report stated.

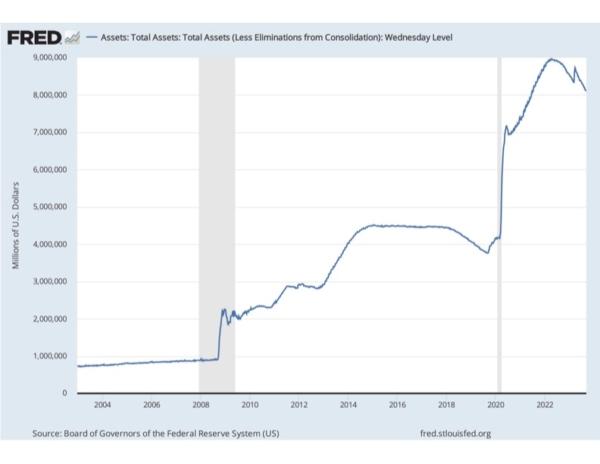

The Fed was created to be a lender of last resort to America’s banks and to set monetary policy; its mission is to keep inflation and unemployment within an acceptable range. Starting in 2008, however, the Fed took on the new role of implementing an experimental policy called “quantitative easing” (QE).

The Fed embarked on this policy at a time when they had driven interest rates to zero, but the economy remained sluggish. Under QE, the Fed created trillions of dollars, which it used to buy Treasury bonds, mortgage-backed bonds, and other securities from banks, on the theory that flooding the economy with dollars would compel new spending, lending and investment, despite the risk of inflation.

Source: Federal Reserve / The Fed's balance sheet, as its investments expanded from $800 billion before 2008 to $9 trillion in 2021 under quantitative easing; shaded gray areas indicate recession

Under QE, the Fed transformed itself from lender of last resort into one of the world’s largest investment funds. In 2020, it launched a second major asset purchase program in response to government pandemic lockdowns, and its holdings ballooned to $9 trillion.

Though America’s central bank has thus far been limited, for the most part, to buying government-issued bonds, it nonetheless moved closer to other countries’ central banks like the Bank of Japan, which is currently the largest single owner of shares in Japanese companies.In Europe, central banks were even permitted to invest for political causes, financing companies that produced wind and solar technology.

Printing Money

Central banks are unique among financial institutions, in that they can create money virtually without limit whenever they want to go on a buying spree. And although the Fed’s expansion was justified as a way to rescue the U.S. economy from recession, its balance sheet never returned to previous levels when the recessions passed.

For all the government spending, living standards fell for the middle class and the poor. And growth rates fell, as well.

The U.S. economy averaged GDP growth rates of 3.1 percent, net of inflation, since World War II. However, during the 15 years since QE was put into effect, growth rates net of inflation have been cut in half, averaging a mere 1.6 percent.

“The Fed is mostly concentrated on short-term growth, but in the long term, creating more money can only create more inflation,” Mr. Hogan said. “The longer-term problems have been getting worse, in terms of regulation, in terms of government spending, in terms of interference in the economy, and the Fed is actually doing a lot of things to make those problems worse.”

In addition to the drag on growth and inflation, quantitative easing risked other unintended consequences. One of these is what is called the “allocative effect.”

This is the incentive or compulsion, during low-interest periods, for investors to allocate funds toward riskier ventures that would pay a higher return, versus safer assets that were once the norm but now yielded almost nothing. Savers could not afford to sit in cash, munis or treasuries because they would just lose money to inflation.

The allocative effect led to a series of asset bubbles—in housing, stocks, cryptocurrencies, etc.—as investors chased yield. In addition to price inflation, asset inflation has become a chronic feature of America’s economy.

Another side-effect was something called the Cantillon effect, which in short means the first ones to get the money get rich. In this case, money-center banks were first in line, and they reaped the benefits before inflation set in. This created enormous wealth disparities in which those holding assets enjoyed huge profits as prices escalated, but those relying on wages or living on fixed incomes suffered from the dollar’s fall.

Government intervention in America’s private economy goes well beyond the Fed, to include government spending and debt, and subsidies and regulations to compel the economy to shift to production of wind and solar energy and electric vehicles (EVs) and away from oil, gas and coal.

“The era of big government is back in the United States,” Steve Hanke, professor of economics at Johns Hopkins University and former member of the Council of Economic Advisors under President Reagan, told The Epoch Times. “It will not only hinder prospects for a healthy recovery; indeed, the heavy hand of government will put a damper on the potential growth rate in the U.S. going forward.”

In many ways, the administration is working against the Fed by spending trillions of dollars it doesn’t have and implementing policies that will likely constrain supply, particularly in industries like energy and transportation. This complicates efforts to fight inflation, which is caused by too much money chasing too few goods.

“If the federal government increases spending, taxes and regulation, there will be less production,” Mr. Laffer said. “Less production courts inflation; more production courts disinflation.”

“The Fed’s inflation-fighting efforts will come to naught if the government interposes obstacles to production,” he said. “Good money, low taxes, free trade, spare regulation, and spending restraint will produce the best results.”